Once again, the mainstream crowd is wrong—this time on real estate. And they’re wrong for the same reason they always are: They’re looking at the wrong numbers.

We’re fine with that. We saw it coming.

And we’re ready to profit through an overlooked dividend grower that throws off $14 billion in yearly cash flow. It hands much of that to us as share buybacks and a dividend that’s jumped 11% annualized in the last five years.

We haven’t seen an opportunity like this since 2021. Back then, pandemic restrictions kicked off a home-renovation bonanza. Another one is getting started now.

Welcome to “Home Reno Boom 2.0”

Today, six years after COVID forced me to turn my patio into Puerto Backyarda (complete with a “misting fan” from Home Depot—hint!), homeowners are pouring another wave of cash into their abodes.

Thankfully, it’s for a different reason: Mortgage rates are high, and those who did buy homes in the rock-bottom-rate days of 2020 and 2021 are loath to move—and lose their bargain-basement 30-year mortgage rates.

The answer? Stay put—and reno your current place.

Many of those folks have also built up a lot of equity since 2021, and they’re tapping it to remodel that kitchen or bathroom they’re tired of looking at.

Last year, for example, they were busy setting up home-equity lines of credit (HELOCs), the number of which jumped 14.3% in the fourth quarter. This year, the total spend on remodeling is projected to jump to $518 billion.

So the money is there. The motivation is there. Now here’s the real trigger for Reno Boom 2.0: The typical American home is now 44 years old.

These houses need new roofs. They need new pipes. The HVAC is about to wheeze its last breath. None of these problems care about interest rates, Middle East conflicts or AI. They need to be fixed—stat.

That’s where Home Depot (HD), the world’s largest home-improvement retailer (and a pick of my Hidden Yields service), comes in.

As I write, little to none of this reno demand is priced into the stock, which has fallen as the crowd assumes HD is going nowhere until home sales pick up. The reno story? They missed the memo.

That’s okay—we’re happy to fill them in!

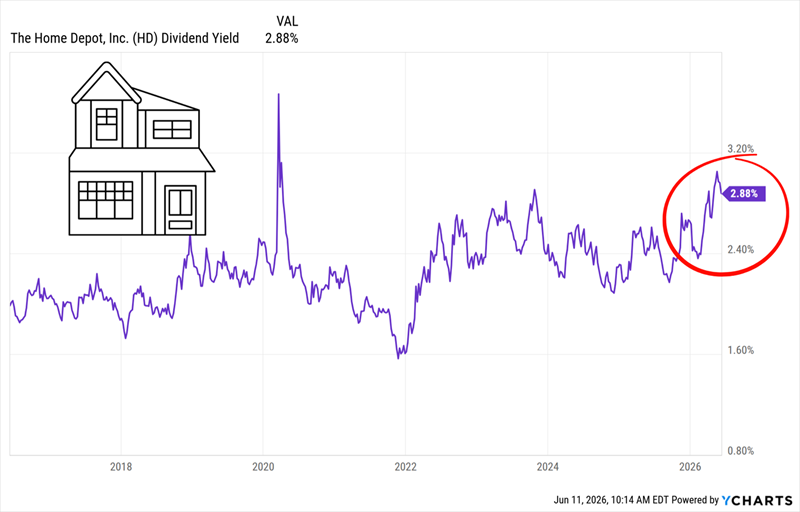

Another reason why HD is a buy now is that the stock’s decline has sent its dividend yield higher (as yields and prices move in opposite directions). As I write, it’s just below 3% and near a peak we haven’t seen since, yes, the 2020 COVID crash:

HD’s Yield Adds a Second Story

A buy now locks in that yield, which is nearly triple what the typical S&P 500 stock pays. Doing so also gives us a nice yield on cost to build from, with HD’s payout hikes averaging 11% annualized over the past five years.

And no, I don’t expect that yield to stick around, for another reason: AI. As it marches through the economy, it’s weighing on hiring and capping wage growth. That’s already happening, with wages gaining 3.6% in April, well behind the May CPI print of 4.2%.

In other words, AI is a deflation machine. As it spreads, CPI—and rates—will likely fall.

Renos Now, a New Address Later

Homeowners, by the way, are somewhat insulated here, as they tend to have higher incomes than the public-at-large.

As lower rates arrive, they’ll tempt more homeowners to move, as the “rate penalty” for ditching their current mortgage eases. That sets up a tidy “2-step” catalyst for HD: a reno boom now, followed by a “handoff” to a fresh round of homebuying as rates fall.

And, again, none of this is priced into the stock.

As I write this, HD is more than 25% off the all-time high it hit in late 2024. That’s absurd for a company generating $14 billion in yearly free cash flow—a total that’s been growing strongly in the last decade:

HD’s Cash-Flow: “Moving on Up”

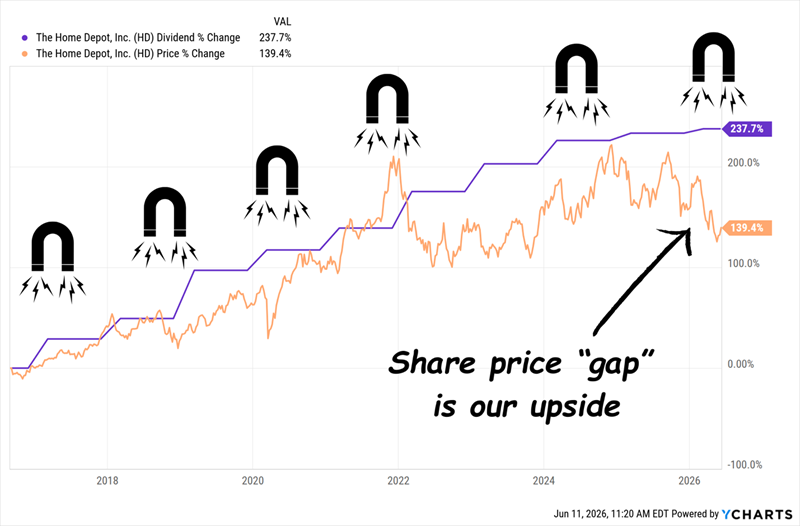

Management, meanwhile, is returning as much of that cash as possible: In the last decade, HD has bought back 17% of its outstanding shares and hiked the dividend a rich 238%. Thanks to that growth, an investor would be yielding 7.3% on a buy made then.

That sturdy payout growth has fueled HD’s “Dividend Magnet”—or the tendency of a rising dividend to pull the share price higher. You can see that in the chart below.

HD’s “Dividend Magnet” Is Due

You can also see that the orange line (the share price) has split from the purple staircase since about last fall. That’s our upside: When that gap closes, we collect the difference.

Meantime, HD is catching a lot more of what contractors spend on projects through its Pro Desk, which, thanks to a couple of recent acquisitions, makes the company a top-to-bottom supplier for contractors.

That’s a big deal: Five years back, a contractor who’d just, say, landed a big kitchen job would have had to call three or four different suppliers to get what they needed. Now they can wander into the local Home Depot’s Pro Desk (or better yet order through the online platform) and everything arrives from one source, on one truck.

Contractors need these materials whether the housing market is booming or busting, especially as American homes age. That alone makes Home Depot’s revenue base stickier—and more recession-resistant—than Wall Street gives it credit for.

AI-Powered Tools Make Contractors Faster (and Home Depot Busier)

Let’s wrap with another way AI is speeding up HD’s business: The company recently rolled out AI-powered tools that convert construction blueprints into material lists in days rather than weeks.

Voice prompts, uploaded documents, text descriptions—throw anything at it and the system spits out a shopping list ready for checkout and delivery. This means AI isn’t replacing contractors—it’s making them faster. And the faster they work, the more projects they take on, and the more materials they order from … you guessed it.

Add it up and you get a company that’s building resilience and growth at the same time. That sets us up for faster payout hikes and Dividend Magnet–powered price gains. And thanks to the lack of love from Wall Street, we’re getting in at a bargain, to boot.

The Dividend Magnet Has Returned 61%, 112% and 148%. Here Are Its Next 5 Winners

The Dividend Magnet is more than just a pattern. It’s a proven way to build wealth.

But to really make it work, you need to know the quality of the cash flow backing up those payouts. Because here’s the danger: The Magnet also works in reverse, pulling down a company’s stock as dividends fall (or flatline).

That’s where Hidden Yields comes in: There, I zero in on the companies with the strongest cash flows and the most overlooked prospects (like HD’s “quiet” reno boom).

When those overlooked tailwinds finally click in with the masses, we get an extra boost as share prices jump—and reel in these stocks’ growing dividends.

The Dividend Magnet has delivered returns like 61%, 112% and 148% for us at Hidden Yields, and I’ve got my next 5 winners ready for you now.