Happy anniversary to my friends Charlie and Ginny, who were fired by their lame financial advisor this time last year.

Why? And, more importantly, how are they doing one year later? Let’s discuss.

Our friends have the same goal as retirees like us: to put the pile of money we saved our entire lives to work for us in retirement. Then, use said pile to provide income, so we don’t have to worry about the pile, the market, the news, and the headlines.

That is where the couple “went wrong,” according to the person they paid to give them “advice!”

Their transgression? Asking too many questions about dividend stocks. They started reading Contrarian Outlook and, of course, began to learn too much.

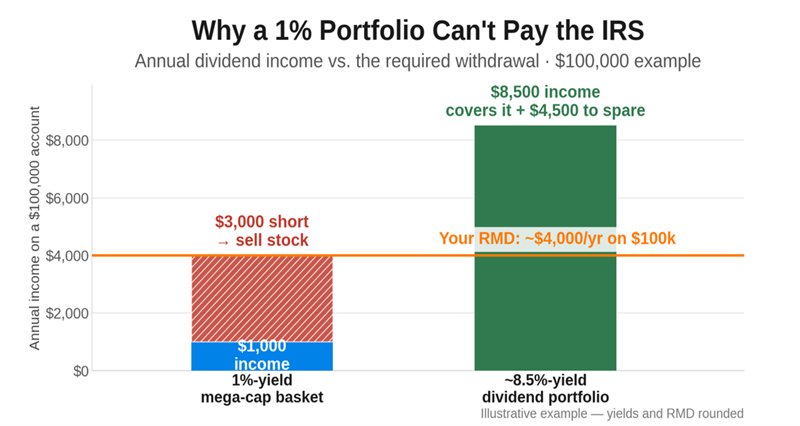

Now, their hired suit had a strategy—the only one that lazy Wall Street ever seems to employ for retirement: Take out 4% a year, and sell stocks to do it.

So, their vanilla bean had them in sub-1% dividends. But Charlie and Ginny specifically needed 4% to cover their annual RMD—their required minimum distribution. (As you know, RMDs kick in at age 73, and they often start around 4% and climb from there. Meaning your portfolio has to earn 4% or more, or you’re eating into it.)

But how is a portfolio yielding only 1% supposed to turn into 4%? By selling shares, of course. And that’s exactly what their suit did, every month, on their behalf. Understandably, it drove Charlie nuts. “I hated that stock was being sold each month to fulfill this requirement.”

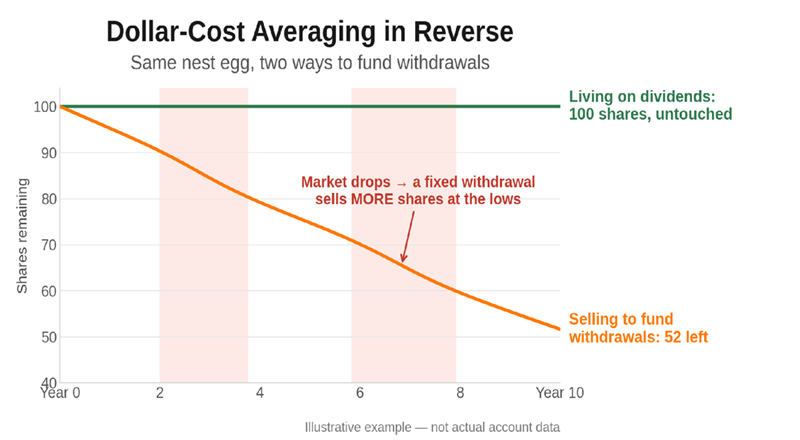

Selling mechanically every month is bad. It is the opposite of dollar-cost averaging (DCA), the strategy you probably used to build your retirement portfolio. When you DCA, you put money to work every month. This is good, not only because you are being a disciplined saver, but also because you are naturally buying more shares when the market is low (and fewer when the market is high).

A monthly investment is a set dollar amount. The stock market is what swings wildly. In building a portfolio, this volatility works in the saver’s favor.

But when harvesting a portfolio—taking money to meet an RMD, or living expenses—it works against the investor! Instead of buying more stock low and less high, you sell more shares when the market is low and fewer when the market is high. (Wait, what?) Charlie and Ginny were understandably perturbed.

They began asking, “Hey, where are the dividends to help us sleep at night?”

His reply? “The S&P 500 did better ‘overall’ than dividend stocks.” So he didn’t suggest changing their approach. This “DCA in reverse,” in other words, was just fine with him!

Isn’t that crazy? Their advisor wanted them to own the usual “buy and hope” stocks—40 near-zero-yield mega caps such as Google, Microsoft and Meta. And he became defensive when they questioned it! (Even financial advisors, who are salespeople in essence, should know that attitude doesn’t sell!)

The couple knew there was a better way. Their initial ask inspired a lame compromise. Their advisor proposed that they buy dividend stocks—“but mostly stocks that paid less than 3% dividends.”

Our friends knew that sub-3% still wouldn’t cover 4%, so they pushed back. And got themselves fired!

Lucky then, because they’re in better shape today. They don’t sweat the gyrations of the market. About half their account now sits in dividend payers, and that half alone covers their RMD thanks to the generous yields we talk about here.

“We sleep better at night,” they told me. It doesn’t matter what the market is doing when they wake up. They don’t even have to watch the market. These generous dividends hit their account like clockwork. Their RMD is covered. They never again have to sell into a drop or pullback. So why would you not sleep better at night?

A big shout-out and thanks to Charlie and Ginny for sharing their story. Now, let’s talk about you. If you’re funding your living expenses or your RMDs by selling shares, you’re running dollar-cost averaging in reverse—just like Charlie and Ginny’s former cheap suit. Change that flawed strategy!

We don’t want you to sell more shares when stock prices are low. What we want is to keep that principal intact—and to own a portfolio churning out smooth monthly dividends, so that you don’t have to sell shares ever.

And here’s a compromise for the vanilla beans who say the S&P 500 does better on average. Consider the JPMorgan Equity Premium Income ETF (JEPI), which buys the underlying S&P 500 index and then sells (“writes”) covered calls to generate additional income.

The steady income cushions JEPI on pullbacks. It’s a sleep-at-night version of the S&P 500. JEPI pays a monthly dividend plus it can still appreciate when the market rises. The fund yields 8.3%, plenty to meet a 4% living expense or RMD obligation and capture market gains!

Now, if you’re interested in building a dividend machine—a portfolio that covers your living expenses and your RMDs—you’ll want to check out our Contrarian Income Report portfolio. We have over 20 stocks and funds averaging an elite 8.5% yield today. That’s right, 8.5%—which is how you cover withdrawals and cash needs without selling a single share.