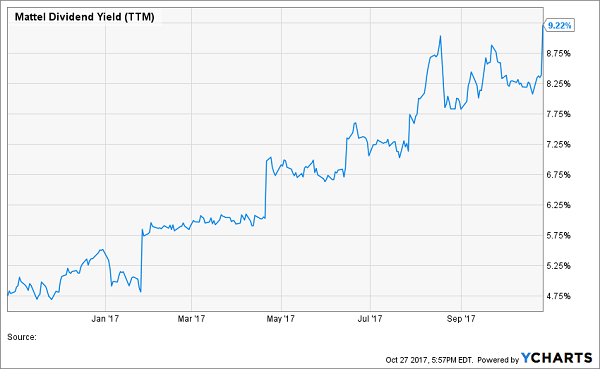

This is an example of a bad almost-10% yield:

When a Bullish Chart is Bad

Mattel’s (MAT) yield was rising for the wrong reason – because its stock price was dropping faster than its payout. Going forward, that shouldn’t be a problem. The firm officially suspended its dividend on Friday.

I warned you that the toy maker was a dividend disaster waiting to happen. In June’s edition of our Dirty Dozen: 12 Dividend Stocks to Sell Now report, we discussed how falling profits were going to be a serious problem for the stock’s payout:

When Mattel last raised its dividend, from 36 cents to 38 cents quarterly at the beginning of 2014, few people batted an eye. The company had earned $2.58 in 2013 – a payout ratio of roughly 60% that no one would’ve deemed worry-worthy.

Fast-forward a few years, and the dividend is not only unchanged, but it’s far, far more than the company’s profits.

When Will Mattel’s (MAT) Bottom Line Hit Bottom?

Mattel’s ubiquitous brands like Fisher-Price and Barbie will always be worth something, and the company isn’t ignorant to technology, offering products such as the voice-controlled smart-baby monitor Aristotle. But the loss of the Disney (DIS) Princess license to rival Hasbro (HAS) in 2014 was a shot to the gut, and Mattel doesn’t have a knockout brand like Hasbro’s Marvel line, which seems to have unlimited potential.

Mattel’s dividend is in serious danger of a cut, and if the company continues its current failure spiral, one could see Hasbro or private equity taking Mattel out of the picture via acquisition.

Since I wrote those words, Mattel’s stock has dropped 39%:

Mr. Market Sniffs Out Mattel’s Faulty Payout

The stock now “boasts” a 9% trailing yield. Investors are likely to see 0% on a forward basis.

If you’re interested in avoiding the next Mattel and running a quick “dividend disaster” check on the stocks you currently own, here’s a 3-step test you can follow today.

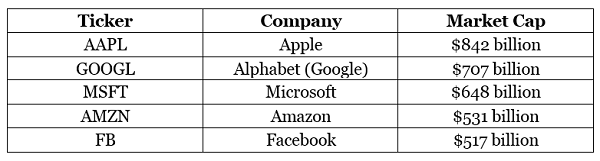

Step 1: Check the Industry (and Don’t Buy a Dying One)

Business disruption is accelerating today as entire industries are being eaten alive. There are five locomotives steamrolling business models across the country (and globe). They are currently the five largest firms by market cap:

2017’s Five Business Bullies

Notice a pattern? All five are tech titans. More specifically, they are the five best companies at writing software – which they use to scale their own businesses, at the expense of countless others.

Here are three entire industries – and payouts – that you should generally stay away from today because they are being steamrolled on the tech train tracks:

- Retail and Retail REIT Dividends

- Consumer Staple Dividends

- Restaurant Dividends

For a discussion of “why”, please click here to review our discussion of the rotten trends in each sector. Now, let’s look at individual companies.

Step 2: Check the Earnings and Cash Flow Trends

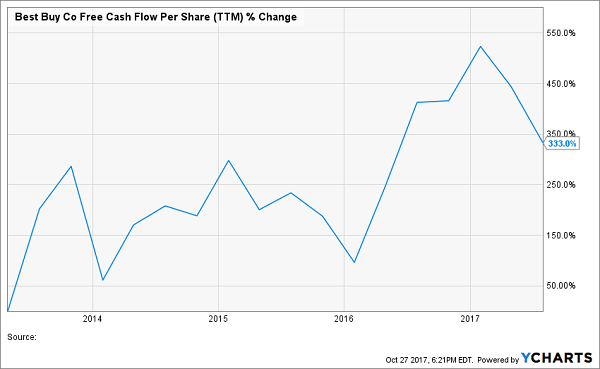

Exceptions to the rule above? Of course. For example, Best Buy (BBY) has “defied Amazon’s gravity” and continued to not only survive but also thrive.

Best Buy Defies “Death by Amazon” for 100%+ Gains

How’s an investor to know that Best Buy is an exception? Simple – look at its free cash flow (FCF) trend, which drives its dividend growth (and stock price):

Best Buy’s FCF Growth Drives its Dividend Growth

Fine, but how do we know that this retailer’s cash flow will keep humming while other retailing giants are eaten alive by the Amazon and broader Internet at large? That’s where a bit of “second-level analysis” makes all the difference.

In Best Buy’s case, a prescient investor would have been bullish on the firm’s online “price-match” policy, which kept in-store customers from buying elsewhere via their phones. He or she also would have also appreciated the retailer “doubling down” on the quality of its physical stores (which Amazon doesn’t have). And the Best Buy bull no doubt would have known that turnaround CEO Hubert Joly, who took the helm in 2012, was the key to everything.

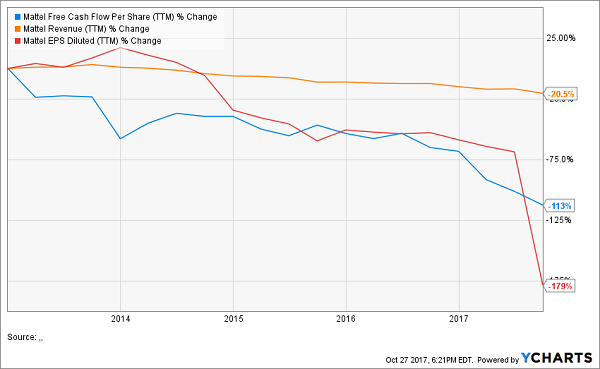

On the other hand, the bearish case for Mattel was obvious well ahead of its actual dividend cut. It had already hit the dividend disaster trifecta, with sales, earnings and cash flow all in a downward spiral:

Mattel’s Foreboding “Dividend Disaster Trifecta”

Step 3: Follow the Smart Money

Legendary investor Peter Lynch was fond of saying that corporate insiders may sell their shares for a variety of reasons (estate planning, divorce, sending the kids to college). But there’s only one reason they buy – because they think the price is going up.

Insiders at dividend payers have one more reason, however – they obviously believe their payout is rock solid, too.

I’m actively involved in three small businesses today. Our next quarter results are never a surprise to me. When you’re actively involved in a business, you see things develop well before the outside world does.

I’d buy more shares in my own ventures if I could. But my equity is capped. So I’m content to grow these businesses – and reinvest my personal profits in my favorite dividend payers.

When possible, I prefer to buy insiders who are putting their own money into their own stock (or fund).

And today, three of my favorite dividend machines – with forward yields up to 10% – are increasing their personal stakes and buying as much stock as they can get their hands on!

I understand why. All three businesses are recession-proof, and should continue to cruise no matter what’s in Trump’s next Tweet. These companies have captive, growing audiences – and they’ll be able to continue raising the rent without a problem.

And best of all, as I said, these stocks pay current yields up to 10%. They are cornerstones of my “no withdrawal” portfolio, which lets retirees and near-retirees generate enough income from dividends that they never have to sell a share of stock.

I’m sure you’ve considered this strategy. Maybe you’re dismayed that it’s impossible to execute with rates near historic lows. After all, with paltry dividends, there’s not enough income to live off.

That’s why a different approach – a contrarian one – is needed today. We must locate yields that are 7% or 8% or higher, and also make sure they’re secure. And what better way to do this than to follow CEOs buying their own out-of-favor, high yielding shares!

I’d love to share the names and tickers of these three insider-loved payouts with you. Click here and I’ll explain in my full analysis – and I’ll also outline my entire “no withdrawal” strategy so that you can live off dividends alone.