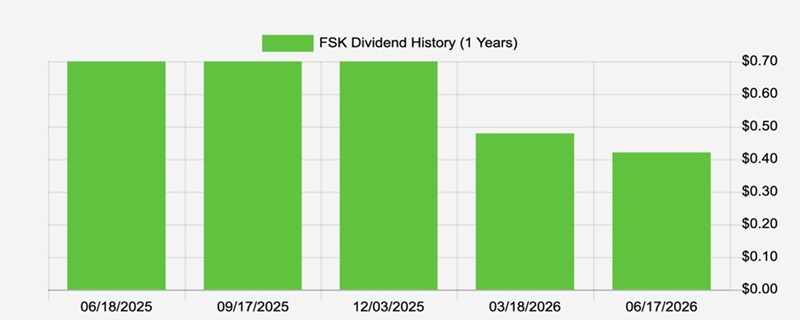

Two dividend cuts in the last two quarters, and we are buying.

Wait. What?

When do we ever chase one dividend cut, let alone two? Let me tell you when, my fellow contrarian!

A Terrible Divvie Trend and We’re In?

Let’s start with the fantastic yield. At 15.3%, FS KKR Capital Corp (FSK) has our attention. That doesn’t mean buy—we don’t chase headline yields around here without doing our homework. But in this case, management is redirecting the money saved from these cuts into share buybacks.

Which means we’ll likely see price appreciation as shares move closer to fair value. Plus, fewer shares outstanding make it easier for management to cover that fat dividend.

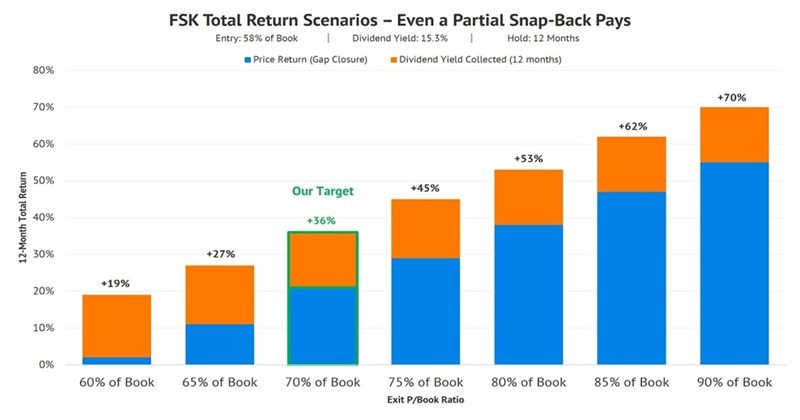

Right now, the rubber band is stretched wide on the pessimism surrounding FSK. Shares trade for just 58 cents on the dollar. Translation: in healthy markets, FSK trades closer to book value—a dollar of loans for a dollar of stock. (Which is 75% up from here.)

What is FSK? A business development company (BDC), a publicly traded fund that lends to small and mid-sized American businesses. It’s run by KKR, one of the most respected private credit shops on the planet.

The management team at KKR just put up $600 million in cash and committed capital to defend their beaten-up dividend stock. Their ante has our attention despite the disastrous headlines.

Now, what happened at FSK in the first place? Why is it so beaten up?

Well, BDCs as a group have been taken to the woodshed this year. The middle-market companies they lend to are under pressure, struggling to service their debt at higher rates. That credit pain flows straight through to the BDCs that fund them.

Historically, BDCs have lived in the safer corner of credit. They lend senior-secured to private American businesses and collect their interest payments like clockwork. Basically, they’re annuities… boring, predictable, yield-y.

But now the entire BDC universe is wrestling with the same headwinds. Credit spreads are widening and non-accruals (delinquent debtors!) are creeping higher across the sector. The clockwork annuity isn’t ticking.

FSK inherited a chunk of legacy investments from prior mergers, and management has spent the last several quarters writing them down. Net asset value (NAV), the per-share value of FSK’s loan portfolio, dropped from $20.89 to $18.83 in just the first quarter of 2026. Non-accruals (loans not paying interest) climbed for the third straight quarter to 4.2% of the portfolio.

In their May 11 statement, FSK’s top execs admitted “certain new non-accrual assets” continue to surface. Translation: more credit pain on the way.

That’s the bad news. The good news? This storm is all priced into the stock, and then some.

At 58 cents on the dollar, KKR sees value. So, last week, the management team announced four actions to close that discount window. Backing it up with a $600 million investment.

First, a KKR subsidiary will buy $150 million of FSK preferred stock, convertible into common shares at the current NAV price of $18.83. Yup, KKR is putting its own capital into FSK at a conversion price 75% above today’s stock price. This is a big bet that FSK trades back toward book value.

Second, a KKR subsidiary will tender for $150 million of FSK common stock at $11.00 per share. KKR is buying shares directly at a price the company’s leadership publicly states is below intrinsic value but slightly above where it trades today, just under $11. (Saying hey, there is serious value here!)

Third, FSK itself just authorized a $300 million share repurchase program running through June 2027. With FSK trading under $11, that retires roughly 10% of total shares outstanding. Every share repurchased below book accretes NAV for remaining holders, makes the dividend easier to pay (fewer shares!). This math compounds, too.

Fourth, KKR waives half of its subordinated income incentive fee for four straight quarters. You read right: KKR skips its own compensation to support FSK’s net investment income and by extension, the dividend. An admission that hey we kinda stunk, so we’re taking a pay cut. Management falls on its sword.

Add it up and we have $600 million of fresh KKR capital flowing into a $3 billion market cap—a 20% “booster shot”:

This is simply unique. I can’t recall a sponsor putting up this level of capital and structural support to a single fund simultaneously.

I realize the FSK rearview mirror is ugly. But the math from here is forgiving. From 58 cents on the dollar to 70 cents, a 21% price move (to the $13.30 neighborhood). Add the 15.3% yield we collect over the next year and we’re looking at a 36% total potential return on a partial mean reversion:

Caution: This is a trade, not a buy-and-hold! We’re not wedding ourselves to FSK.

We’re simply stepping in and drafting KKR’s $600 million “whale bet” on FSK shares. As the gap between the stock and fair value closes, we’ll collect payouts—and, sooner rather than later, cash in our chips.

Looking for a big dividend that you can hold for years and years instead? Then my contrarian dividend blueprint is for you, featuring yields to 14.9%.