I’m no mind reader, but I’m guessing you’d leap at an investment with the stability of a bond and the upside of a stock right now.

Sounds like something tailor-made for a crisis, right?

The good news is that it’s no pipe dream. These handy “crash-resistant” plays are out there and ripe for buying. We’re going to take a close look at how we can tap them for huge dividends now—yearly cash payouts all the way up to 9.7%!

It’s a retirement strategy every investor should take a look at. Unfortunately, too few even know these “shapeshifter” investments exist.

Lender Today, Shareholder Tomorrow

I’m talking about convertible bonds. As the name says, you can switch these income chameleons from a bond to a share of stock whenever you like.

And these days, the crisis has US companies tapping the convertible-bond market with abandon, giving us lots of choice: according to Barron’s, $31 billion of convertible bonds have been issued since the beginning of April alone, more than half of the $53 billion issued in all of 2019.

Southwest Airlines (LUV), for example, issued $2 billion of convertible senior notes on April 28. The notes, due in March 2025, offer the holder the option to convert to stocks at a share price of $38.48. As I write this, Southwest trades at $32.55, so converting would cost you $5.93 a share. So it’s safe to say there won’t be many conversions happening now.

But converting could still bag you a big double-digit return as the crisis eases and people hop back on planes. Consider that the last time Southwest hit $38.48 prior to COVID-19 was in September 2016—and once it hit that level, it ripped 77% higher, to a record $66, in just 14 months.

LUV Bondholders Wait for History to Repeat

Meantime, you do get downside protection in the form of your initial investment back at maturity. And even if the coronavirus grounds Southwest permanently, convertibles are higher up the capital structure than common stocks, so you’d get paid before regular shareholders in the event of a bankruptcy.

There is a cost to convertible bonds’ “lottery ticket” potential, though: less income. Southwest’s convertibles yield 1.25% today, below the stock’s current yield of 2.2%.

This is where most income-seekers give up, and that’s too bad because there’s a back-door play that lets us tap these bonds for dividends up to eight times bigger than what Southwest’s convertibles currently pay.

Convertible Bonds: Where Beating the Index Is a Snap

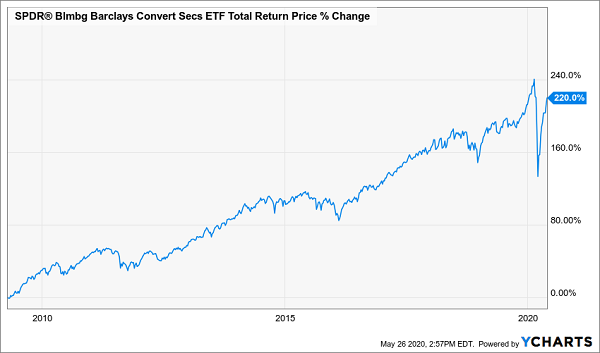

That strategy is to avoid buying convertible bonds individually—which is nearly impossible for individual investors like you and I anyway—and buy them through a fund instead. Most folks automatically default to an ETF like the SPDR Bloomberg Barclays Convertible Securities Fund (CWB).

That’s not the worst option: CWB will more than double the yield on the individual Southwest Airlines bond, with a 3% payout. And the fact is, it’s done all right since inception a bit over 11 years ago:

Plain-Vanilla ETF Does Okay

But there’s a problem with the ETF approach: when a company issues convertibles, huge investment houses like BlackRock, which manage trillions in cash, get the first pick. Plus, the fund managers at these companies have access to cheap money—especially today—they can use to leverage returns.

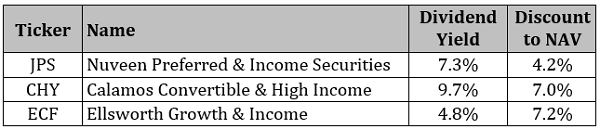

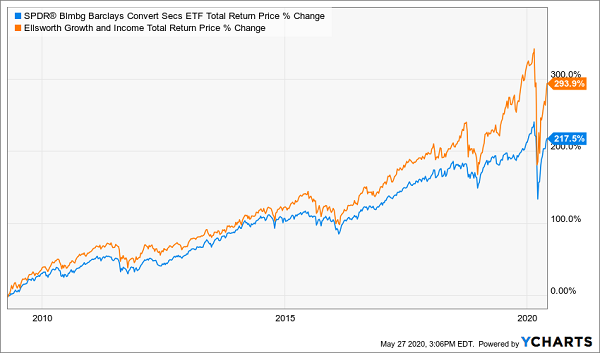

That’s a one-two punch that the algorithm running CWB can’t counter, and it’s why the ETF trails actively managed CEFs in this space. As you can see below, three major convertible-bond CEFs, the Calamos Convertible & High Income Fund (CHY), Ellsworth Growth & Income Fund (ECF) and the Nuveen Preferred & Income Securities Fund (JPS), have all bested CWB since the ETF’s inception in 2009.

Human Managers Overload the Algorithm

Better still, these CEFs pay huge dividends: JPS yields 7.3%; ECF pays 4.8%, and CHY throws off a gaudy 9.7% today!

Second, CEFs can (and often do) trade for significant discounts to their net asset values (or NAVs—the market value of the convertible bonds they hold, giving us downside protection (and upside!) while we enjoy their huge dividends.

Take a look:

3 Cheap Convertible-Bond CEFs Paying Up to 10%

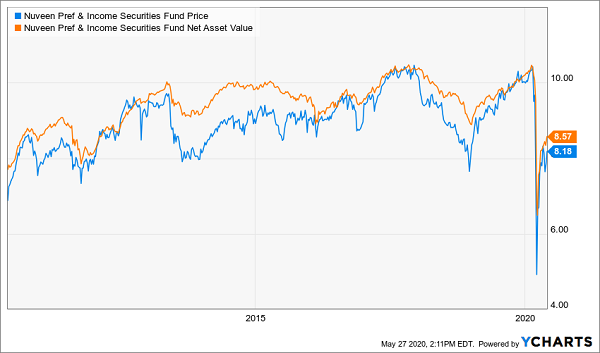

If you’re a member of my Contrarian Income Report service, JPS probably rings a bell. It’s a long-time hold, and its management firm, Nuveen, recently expanded its mandate, allowing the fund to pick up preferred shares and convertible securities.

Every few years, JPS falls out of favour for whatever reason, and we get a chance to pick up shares cheap and add to the dividends we receive from the fund, which drop into our account monthly.

JPS: Buy When the Blue Line Drops

A 9.7%-Paying Fund With … Free Management Fees?!

Here’s something else you can forget about with these funds: management fees!

Take CHY, which held 60% of its portfolio in convertible securities as of April 30, including convertible bonds from the likes of Tesla (TSLA), Carnival Corp. (CCL), Broadcom (AVGO) and, yes, Southwest.

The team at the top has flipped from bondholder to shareholder so successfully that it’s delivered a nice 7.9% annualized return on NAV since inception, and has consistently run well ahead of CWB since the ETF’s inception in 2009—a gap it’s now restoring as its overdone 7% discount shrinks.

CHY’s Managers Crush the Benchmark

Right now, CHY charges 1.8% in fees, but because we’re buying at a 7% discount, that cost is basically comped! The deal is even better on ECF, whose 1.2% fees barely register against its 7.2% discount.

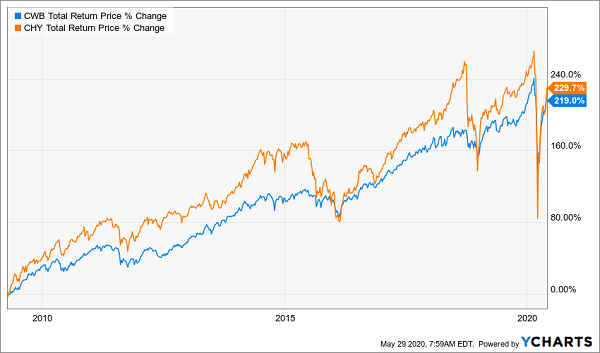

You’ll sacrifice some income with ECF, which only yields 4.8%, but you’ve got a greater shot at upside thanks to its wider discount and history of outperformance—it’s vastly outrun CWB since the ETF’s inception:

Lower Dividend, Bigger Upside

That outperformance, along with the fact that ECF relies more on price gains than dividends to deliver your return, could make it a great pickup if you’re younger, or have less need to tap your portfolio for income.

5 MORE “Recession-Resistant” Dividends (Up to 13%!)

Here’s something else hardly anyone knows: steady 9.7% dividends are common with CEFs—and some of these funds’ monster payouts run well into the teens!

Like one CEF I’m pounding the table on now—it pays a gaudy 13% dividend!

Think about that for a second: buy this amazing fund now and every single year, 13% of your original buy boomerangs back to you in CASH! Fast-forward 6 years and you’d have piled up enough in dividends to match your entire upfront investment.

In other words, everything you gain in price appreciation is gravy!

If that’s not the very definition of safety, I don’t know what is.

To make the deal even sweeter, this unusual fund is trading at a double-digit discount as I write this—so not only are we getting nearly double the market’s historical return in CASH, we’re also getting a massive discount that gives us extra downside protection and a shot at big price upside, too!

It really is the best of all investment worlds.

And that’s not even the full story: this “recession-resistant” 5-pack of CEF picks also includes a fund paying a gaudy 11% dividend now (and also trading at an outrageous discount). Another pick pays a tax-free 6.3% dividend that could be worth 8% or more to you, depending on your tax bracket!

These 5 picks are the perfect combination of stocks and funds to own in this crisis, and I can’t wait to show them to you. Click here for a full briefing on all of 5 these ironclad income plays, including names, tickers, dividend histories and a complete analysis of their management—literally everything you need to know!