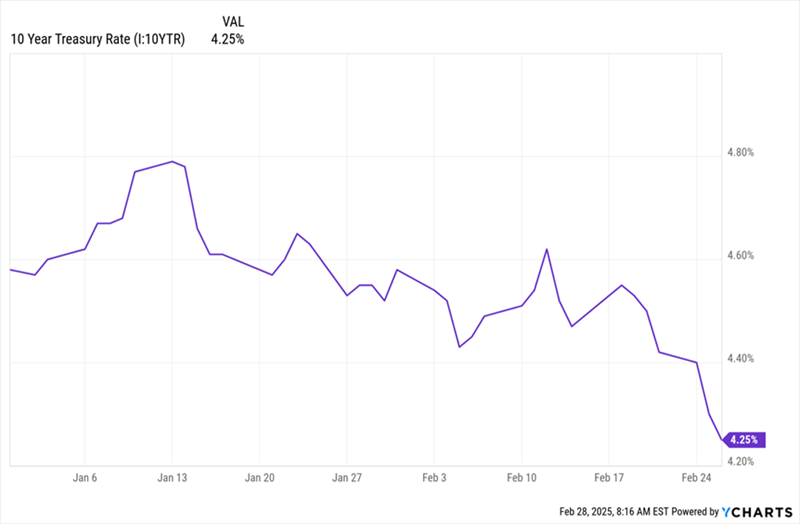

Let me say right now that, like most people, I have no idea where the trade tensions we’re living through will end up. But here’s something I will say: Whenever I have any doubt about the future, I look to the 10-year Treasury rate—and I recommend you do the same.

And the 10-year rate—pacesetter for rates on most loans—is screaming one thing at us right now:

Fade the inflation fears that are everywhere these days.

So we’re going to take Mr. 10-Year’s advice and “buy the dip” in 2 “bond-proxy” closed-end funds (CEFs)—each yielding around 7%—that we’ll discuss in a bit.

We’re pouncing now because the 10-year rate has done something stunning this year: drop. That’s the opposite of what it would do if inflation worries were legit.

Inflation Fears Surge—and Interest Rates Fall?

The key takeaway for us is simple: By dropping, the 10-year is saying an economic slowdown, NOT surging inflation, is the main risk now. That, in turn, tells me that the Fed will likely cut rates faster than most people think.

2 More Signs Inflation Worries Are Off the Mark

The 10-year rate’s message lines up perfectly with a couple of recent studies that have said tariffs are NOT inflationary, because they slow economic growth, which acts as a drag on prices.

The Centre for Economic Policy Research found that tariffs do not boost inflation because rising prices depend on a hot economy—and a trade war does the opposite.

The Financial Times reached a similar conclusion. Yes, tariffs squeeze company margins due to upward wage pressure and higher costs. But these are typically absorbed by the firms—and their shareholders!

Look, I know neither a jump in inflation nor a jump in unemployment is a happy story. But for investors, the key takeaway is that slowing growth means lower rates—and that means higher bond prices (because rates and bond prices move in opposite directions—it’s the law of Bond-land).

This is why we’ve pivoted our Contrarian Income Report portfolio toward bonds and “bond proxies”—like utilities.

That’s where those two 7%-paying closed-end funds (CEFs) I mentioned earlier come in.

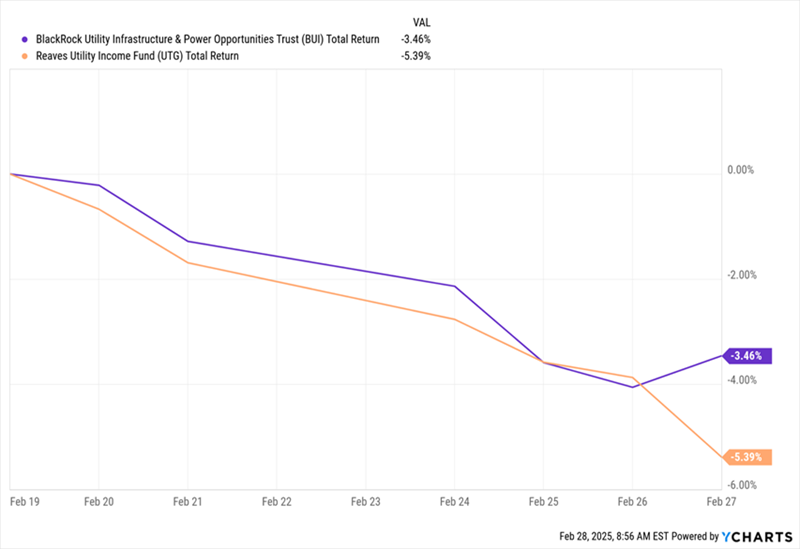

Both have been tossed over the side in the last couple of weeks, as the 10-year Treasury rate dropped. That shows us how far off track first-level investors are here: If these two funds were truly taking their cues from the 10-year rate, they would’ve gained.

Therein lies our opportunity. Take a look at the declines in the Reaves Utility Income Fund (UTG), in purple, and the BlackRock Utility Infrastructure & Power Opportunities Trust (BUI), in orange, in the last couple weeks:

Utility CEFs Drop, Signaling Our Opportunity

Let’s delve into them, starting with Contrarian Income Report pick UTG.

Utility CEF Pick No. 1: Reaves Utility Income Fund (UTG)

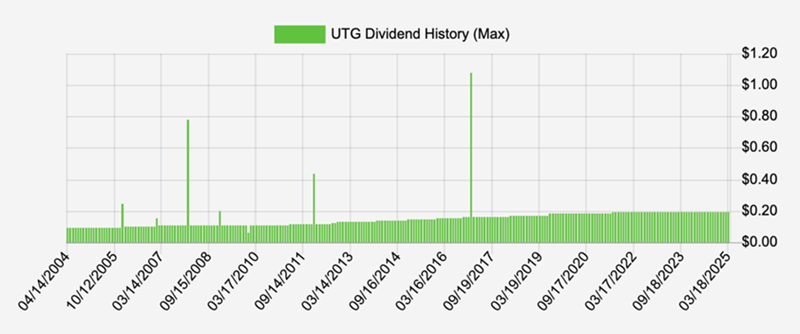

We bought UTG in CIR in June 2023—another time when inflation fears were overdone—and it’s rewarded us with a 38% total return since.

The fund yields 7.2%, pays dividends monthly and has kicked out a steady—and gently rising—monthly payout since it launched 20 years ago. It’s tossed in a few special dividends along the way, too:

UTG’s Dividend Powers Along

Source: Income Calendar

UTG is what I’d call a “pure play” utility fund, boasting US names like California’s Sempra (SRE), Texas-based Vistra Corp. (VST), PPL Corp. (PPL) of Pennsylvania and Louisiana-based Entergy (ETR).

That said, it does venture a little bit outside the electrical-power space here and there, with holdings in adjacent industries like pipeline operator Enterprise Products Partners (EPD) and data-center REIT Equinix (EQIX), which is, of course, profiting from AI’s surging demand for computing power.

We also like the fact that UTG only borrows against 19% of its portfolio—enough to grab a tailwind without adding too much risk. And of course, falling rates mean lower borrowing costs (and by extension higher profits) for the fund, too.

UTG trades around par, which is really a discount in disguise for us, as its five-year average premium to net asset value (NAV, or the value of the stocks it holds) is around 1%. That premium rose even higher back in 2021, and I expect something similar as investors realize the true concern is a slowing economy, not surging inflation.

Utility CEF Pick No. 2: BlackRock Utilities, Infrastructure & Power Opportunities Trust (BUI)

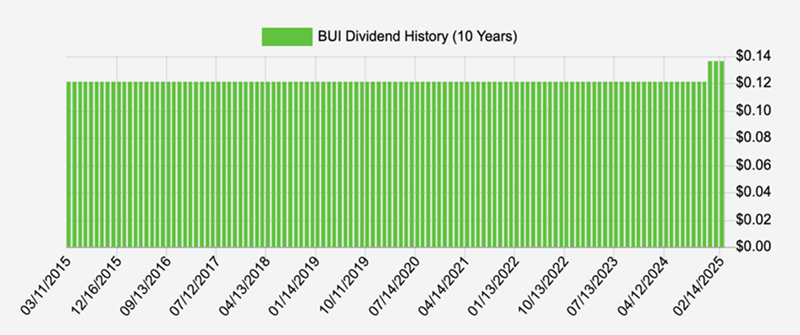

BUI isn’t a CIR holding, but it’s still worth a look if you want an “all-purpose” fund with a strong lean toward utilities. As mentioned, it yields 7%, and, like UTG, it’s been a reliable payer for the long haul, recently delivering a nice payout hike:

Source: Income Calendar

Now let’s talk about that different portfolio makeup, which gives us access to stocks beyond utilities but at a nice deal now, since BUI has dipped with other more concentrated utility funds.

BUI has about 44% of its portfolio in utilities, with big players like NextEra Energy (NEE) and Constellation Energy (CEG) both popping up in its top-10 holdings.

However, capital goods make up 30% of exposure, again in business we can view as tied into utilities, like HVAC specialist Trane Technologies (TT) and GE Vernova (GEV), a maker of renewable power gear that was spun off from GE last year. Finally energy is in the No. 3 spot (10%), including firms like Williams Companies (WMB).

BUI also gives us a bit of diversification beyond the US—not a bad idea, given the uncertain trade situation. Right now, US stocks account for 67% of BUI’s portfolio. The rest is invested in developed countries like France (8%), the UK (6%) and Italy (5%).

Another difference between BUI and UTG is that BUI uses no leverage, which cuts its risk even more. It also sells covered-call options, under which it sells investors the right to buy its stocks at a fixed price and at a future date.

That’s a smart way to generate extra cash—with utility stocks generally steadier and more predictable than other corners of the market. And UTG keeps the fee it charges for these options, no matter what happens.

Finally, like UTG, BUI trades around par. But also like UTG, I expect it to see a wider premium as the story flips from inflation to a slowing economy.

Another URGENT Buy as Rates Drop (Yields an Incredible 11%)

As we just discussed, “bond proxies” have been tossed on overdone inflation fears. But bonds themselves have, too! That sets up another big income opportunity for us.

Our target: Another CEF—this one kicking out a monster 11% dividend yield. It’s run by a guy who’s at the very peak of the bond world. He’s been named Fixed Income Manager of the Year by Morningstar and been inducted into the Fixed Income Analysts Society Hall of Fame, too.

Best of all, this overlooked income play pays dividends monthly.

But as with our utility funds, I expect our buy window to close fast as rates move lower, catching many investors by surprise as they do. Don’t miss out. Click here to learn more about this monster 11% dividend and get on the list to receive its next payout, which is just weeks away.