One of the worst investing mistakes you can make is blindly sticking to “rules of thumb” given out by so-called “experts.”

That goes double when you use these overly broad guidelines for the most important decision you can make: planning for your financial future.

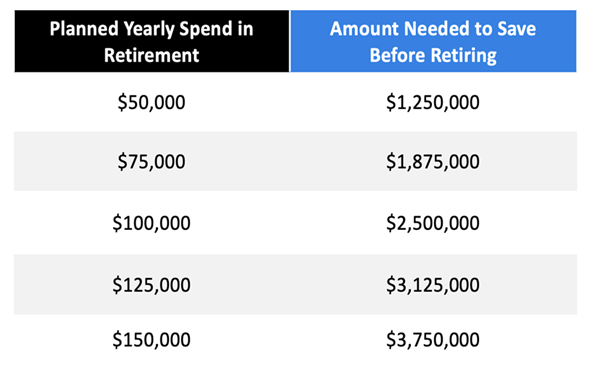

Consider a recent article by Bankrate telling retirees to follow the “rule of 25,” which is as simple as it is deceptive. This piece tells us that you “should have 25 times the annual amount you plan to spend in retirement saved before you leave the workforce.”

That’s a lot of money! Take a look at the table below to match up how much you plan to spend in retirement (to make things easier, we’ll set inflation aside and use today’s dollars) with how much you’d need to save.

Now let’s say that you’re earning $100,000 a year and save 20% (much more than the average American) to get to retirement quickly. At that rate, assuming the 8.5% historical return in stocks continues, it’s going to take you a bit over 29 years to clock out. If you’re young, that surely sounds like a long time, and if you’re older, you might think you don’t have enough time to get there.

In both cases, though, this anxiety is built on a false premise, because the rule of 25 has been debunked by none other than its original author.

William Bengen invented the 4% safe withdrawal rate based on historical research in 1994. Under this approach, you’d need to have saved 25X your planned retirement spending. If you have less, you face the risk of running out of money when you’re very old, the worst time to be broke.

However, Bengen updated his rule to 4.7% in 2022, based on new data, which would be more like the 21.27X rule. Not the nice, whole round number that most people would like, but more grounded in the actual data. Even then, there are a lot of assumptions in Bengen’s model.

There is, however, a much better alternative.

CEFs: The Key to a Faster Retirement

There are many closed-end funds (CEFs) that are specifically designed to translate the long-term roughly 8.5% annualized returns of the stock market into a regular income stream retirees can use to replace a salary.

For example, consider the Liberty All-Star Equity Fund (USA), a broad-based equity CEF that holds stocks like Microsoft (MSFT), UnitedHealth Group (UNH), Amazon.com (AMZN), Visa (V), Danaher Corp. (DHR), Sony Group (SONY) and other stalwarts of the US economy. USA currently translates gains from those stocks into a 9.6% dividend yield.

On that basis alone, we could say that an investor needs just $1,046,667, which would take 18 years and about nine months to get for someone making $100,000 and saving 20%.

Even so, naysayers often attack CEFs, saying their high payouts aren’t sustainable, so let’s look at the past.

USA has been around for 37 years and has paid about 82.4 cents per share per year on average in dividends. That’s about 11.6% of the $7.13 at which it traded back in 1987, which could cut our saving time to get to $100,000 down to about 17 years. It also makes for the even more awkward Rule of 8.58369.

USA’s Multiple Entry Points

While the chart above might look worrisome, with USA’s current market price below where it was nearly 40 years ago, when it started trading, remember that the fund strives to pay out almost all of its profits to investors as dividends.

And USA delivered a strong passive income stream through the end of the Cold War, the burst of the ’90s housing bubble, the dot-com bubble, the Great Recession and, of course, the slow recovery of the 2010s and the recent pandemic and its aftermath.

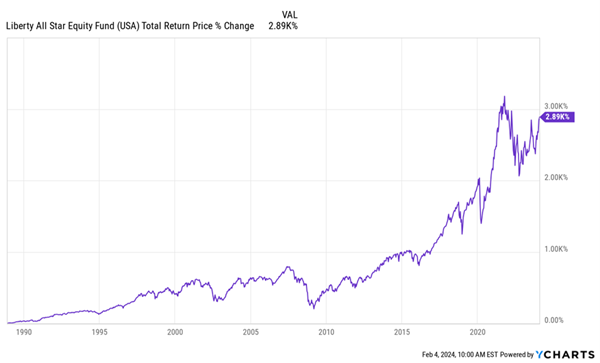

And if you’d reinvested your dividends in those years, you can forget about the price chart above. This is what your return would’ve looked like in this timespan:

Strong Long-Term Profits

That’s a staggering 2,890% profit over several decades, thanks to USA’s ability to translate profits into dividends we can choose to either put back in the fund or use to pay the bills. USA, and CEFs like it, give us the power to make that choice.

4 MORE Bargain CEFs That “Translate” Price Gains Into CASH

I don’t know about you, but when it comes to investing, I prefer to get as much of my gain as possible in safe dividend cash. Picking up USA today is one way to do that.

But there are plenty of other CEFs out there that literally take the price gains their portfolios generate and “convert” them to 8%+ CASH dividends!

The result? A huge—often double-digit—payout flowing our way.

That’s what my top 4 CEFs to buy for 2024 (current yield: 10.2%) offer—and they’re ripe for buying now. Click here and I’ll share more details on each of them with you, as well as our complete CEF-buying strategy.

You’ll also get to download a FREE Special Report naming all four of these funds, including their tickers, current yields, discounts and everything else you need to get in on them now, while they’re still cheap.