If you take the mainstream financial media at face value, you might be under the impression that all high yield bonds are in big trouble with interest rates on the move.

Wrong.

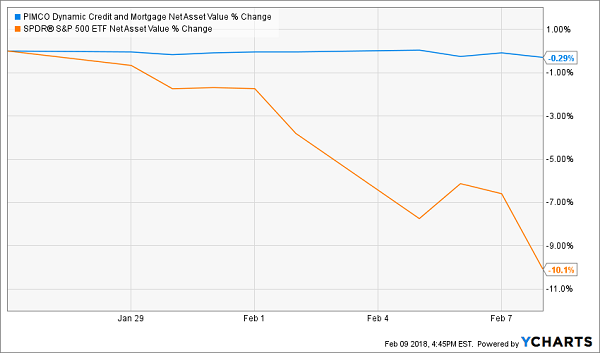

The best bond portfolios haven’t actually budged since the recent market insanity began. Take, for example, our favorite PIMCO play. Its net asset value (NAV, the actual market value of its holdings) held steady while the stock market was dropping sharply:

What Crash? This NAV is Steady

The fund’s price, meanwhile, eased down 2.2% from peak to trough. But we shouldn’t confuse price with value – we should focus on the latter, which is a more accurate measure for investing profits.

If we’re going to obsess over a ticker, let’s follow the NAV (which is updated daily) instead of the share price (which is updated too often for anyone’s well being).

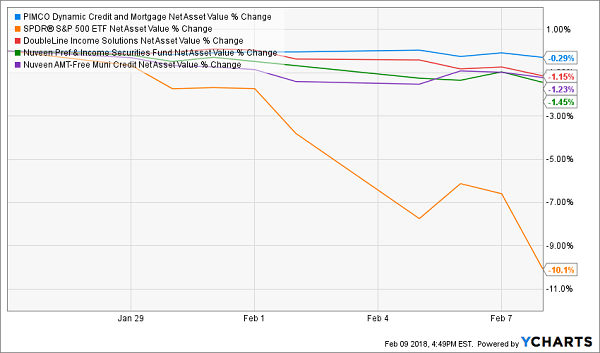

When we expand our “crash stress test” to include a few more of my Best 8% Payers for 2018 we see that their NAVs have also held quite steady while stocks swooned:

What, Us Worry?

Sure, these funds all saw price declines in excess of their NAV drops (from -1.5% to -3.3%). This caused their discount windows to widen during the market mayhem – a sign of fear that we contrarians should capitalize on.

Remember, the bigger the bargain we buy, the higher the yields and price upside we secure. Let me explain.

How to Buy Rate-Proof and Crash-Proof 8%+ Bonds

No safe bond pays 8% itself today. But we can generate 8%, 9% or even 10%+ yields from a portfolio of secure bonds – if we choose the right vehicle and buy at the right time.

The secret is similar to successful dividend investing. Why buy a stock and be content pocketing “only its dividend” when we can have the payout with price upside to boot?

Most income investors aren’t very thoughtful when they purchase bonds. They fixate on the coupon rate (or yield). And they watch their bonds lose value as rates spike (and/or stocks crash).

A better idea? Follow this two-step formula to find fixed income that even the reborn “bond vigilantes” – the mythical market characters that punish fiscally irresponsible governments with higher rates – or a shaky stock market can’t touch.

- Focus on rate-proof, crash-proof and vigilante-proof portfolios.

NAV-watching, as discussed, is more productive than ticker-watching. We must also make sure that the bond manager we give our money to is “delivering alpha” with his or her strategy. The manager must have an edge, and it must be an advantage that is insulated from market movements.

The portfolio must be positioned for future NAV gains, in other words.

Then, we buy when fear is high.

- Demand a discount (our margin of safety).

Closed-end funds (CEFs) are my favorite way to play and profit from bond market misunderstandings. Why is the CEF structure perfect for us contrary-minded investors? Their fixed pools of shares.

Mutual funds issue more shares whenever they want. But closed-ends have a fixed share count, with their funds trading like stocks. As a result, during times of panic (like right now), good funds can fall out-of-favor and find their shares trading at discounts to their NAV.

This is basically “free money” because these underlying assets are constantly marked to market.

CEFs can (and do) also trade at premiums and actually command more than a dollar for just $1 worth of assets. It’s generally a bad idea to buy these favored funds.

For example, let’s pick on a PIMCO fund that I often pan because it trades at steep premiums. Their Global StocksPLUS & Income (PGP) fund was crushed alongside the broader bond and stock market in two weeks. It faced the “double whammy” – its NAV dropped by 5.5% and it already traded at a premium. With no margin of safety, its price dropped by 6.2%.

Yet PGP still trades at a 16% premium to its NAV. I’ve been warning readers about it for years and it’s been a complete dog during that entire time period, returning negative 18% including dividends over the last three years!

An Expensive High Yield Dog

PIMCO of course has some of the smartest bond managers on the planet. But the price we pay (step #2) matters just as much. Investors who paid up for PGP’s premium chose a good horse, but they paid too much for it. As a result, they have been hurting alongside other “first-level” stock and bond market investors of late.

So don’t let anyone tell you that market timing doesn’t work. When we buy matters just as much as what we buy. And the best time to buy is simply when most investors are irrationally running for the exits.

Best Bond Bets Today: 3 Bargain 8%+ Funds With Price Upside

We don’t have to buy and hope for growth. We can snare amazing yields and price upside when we buy cheaply.

That’s why I always demand a discount. A bigger bargain means we have price upside (as the discount window closes) and our yield is higher than it would be if the fund traded for fair value (because income is earned per NAV unit – so the less we pay for it, the better).

Most Wall Street spreadsheet jockeys say we investors can’t have both the income and safety of bonds and the upside of stocks. We have to choose, or allocate, or whatever.

They’re wrong.

My three favorite funds to buy today are a cornerstone of my 8% “no withdrawal” retirement strategy, which lets retirees rely entirely on dividend income and leave their principal 100% intact.

Well that’s not exactly right. Their principal is more than 100% intact thanks to price gains like these! Which means principal is actually 110% intact after year 1, and so on.

To do this, I seek out closed-end funds that:

- Pay 8% or better…

- Have well funded distributions…

- Trade at meaningful discounts to their NAV…

- And know how to make their shareholders money.

And I talk to management, because online research isn’t enough. I also track insider buying to make sure these guys have real skin in the game.

Today I like three “blue chip” closed-end funds as best income buys. And wait ‘til you see their yields! These “slam dunk” income plays pay 8.5%, 8.7% and even 8.9% dividends.

Plus, they trade at 10-15% discounts to their net asset value (NAV) today. Which means they’re perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch funds will simply trade flat… and we’ll still collect those fat dividends!

If you’re an investor who strives to live off dividends alone, while slowly but safely increasing the value of your nest egg, these are the ideal holdings for you. Click here and I’ll explain more about my no withdrawal approach – plus I’ll share the names, tickers and buy prices of my three favorite closed-end funds for 8.5%, 8.7% and 8.9% yields.