Today we’ll talk about how to value REIT (real estate investment trust) stocks. I’ll show you specifically how to lock in high current yields and leave yourself open to 250%+ price upside as well.

A big thanks to my astute subscribers who have written in asking for this lesson. FFO in particular has been a hot question – what exactly is it, anyway? Let’s start here, because it’s what drives REIT returns.

Funds From Operations (FFO) is the Cash Flow That Matters

FFO represents the amount of cash a REIT actually generates from its operations. It’s where our dividend originates – which makes it the building block for everything else in the REIT world.

To calculate FFO, we start with net income. Then we add back depreciation and amortization (which are accounting expenses) and subtract profits from property sales (which are one-time events).

Some firms will emphasize AFFO (adjusted FFO), which subtracts recurring capitalized expenditures. I don’t have a preference myself – I just ask for consistency from management.

What Percentage of FFO Can Safely Be Paid Out?

REITs are required to pay most of their earnings back to shareholders as dividends – but those are just paper profits. FFO represents the actual rent checks that can be dished back to shareholders as dividends.

Obviously we want to see FFO per share in excess of the dividend per share. If it’s not, it means the dividend isn’t really “covered” and management is funding the payout with borrowed money.

I generally look for dividend-to-FFO payout ratios below 80% for REITs. Again, every firm is different and some can get away with a higher percentage than others. Pay attention to management – most competent teams will say what their target ratio is. Note this, and hold them to it.

Declining ratios are often a good sign, because they indicate rising FFO. They’re often a precursor for dividend increases.

FFO Drives Dividend Growth

FFO is the driver of dividend growth for REITs. Figure out where FFO is going, and you know where the payouts are heading – and how fast.

If FFO is stagnant, a firm can only increase its payout by increasing its payout ratio. And this isn’t sustainable over time.

Rising FFO on a per share basis, on the other hand, will basically force management to raise its dividend. And that’s what ultimately drives the stock price higher, because dividend growth is all that matters for REITs. Figure out where the dividend is going, and you know where the stock price is heading.

Reason Being, Yields are Consistent Over Time

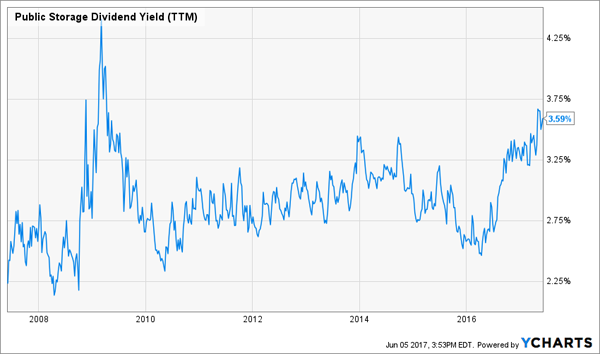

REIT yields tend to be quite steady over time. For example, blue chip self-storage name Public Storage (PSA) usually pays somewhere between 2.5% and 3.5% (absent a financial crisis):

PSA Pays the Same, More or Less

But be careful – just because the current yield goes nowhere doesn’t mean the stock price goes nowhere. In fact, it’s quite the opposite.

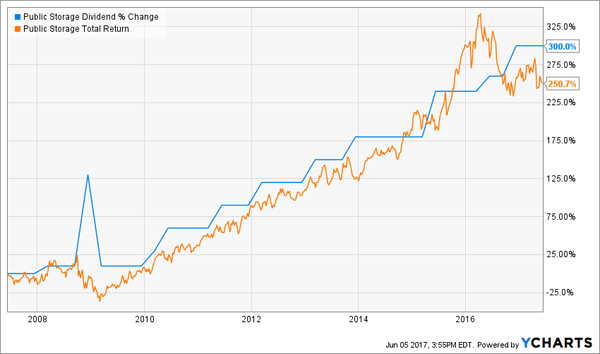

Over the last ten years, PSA has increased its dividend by an impressive 300%. Its stock has followed suit, delivering 250% total returns to shareholders!

PSA’s Dividend Drives its Stock Higher

Retail landlord giant GGP (GGP), on the other hand, pays just half the dividend today that it did during its 2007 salad days. The net result? A 47% price loss (-30% even with dividends) for investors over the last decade:

Dividend Down, Stock Down

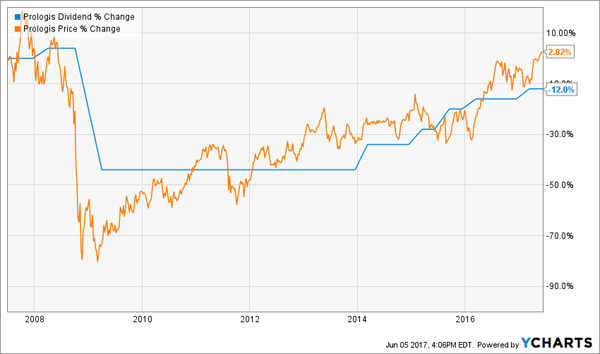

Meanwhile industrial landlord Prologis (PLD) pays about the same dividend it did a decade ago. Its share price has also tracked its dividend – perfectly sideways:

Dividend Sideways, Stock Sideways

REITs can be excellent yield vehicles. But why not buy them for growth too? It is possible to have your dividend and enjoy price upside to boot – and it all starts with rising FFO.

2 Dividend Growth REITs: 7.6%+ Yields and 25% Upside

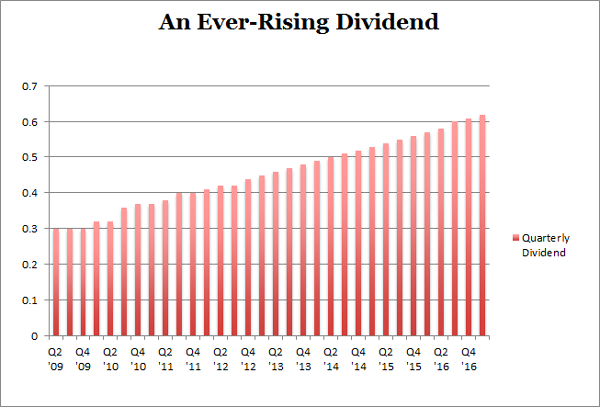

My favorite REIT today just raised its dividend again by 4% over last quarter’s payout. This marks the 19th consecutive quarterly dividend hike for the firm:

Dividend Hikes Every Quarter

It pays an 8.1% yield today – but that’s actually an 8.5% forward yield when you consider we’re going to see four more dividend increases over the next year. And the stock is trading for less than 10-times funds from operations (FFO). Pretty cheap.

However I expect its valuation and stock price will rise by 20% over the next 12 months as more money comes stampeding into its REIT sector – which makes right now the best time to buy and secure an 8.5% forward yield.

Same for another REIT favorite of mine, a 7.4% payer backed by an unstoppable demographic trend that will deliver growing dividends for the next 30 years.

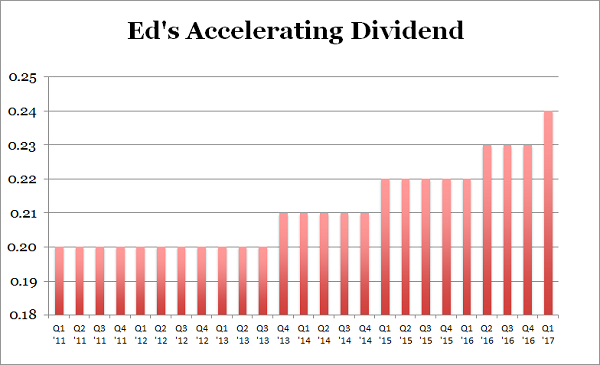

The firm’s investors have enjoyed 86% total returns over the last five years (with much of that coming back as cash dividends.) And right now is actually a better time than ever to buy because its growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

An Accelerating Dividend

This stock should be owned by any serious dividend investor for three simple reasons:

- It’s recession-proof,

- It yields a fat (and secure) 7.4%, and

- Its dividend increases are actually accelerating.

These two REITs are both “best buys” in my 8% No Withdrawal Portfolio – an 8% dividend paying portfolio that lets retirees live on secure payouts alone. And they can even enjoy price upside to boot, thanks to the bargain prices they’re buying at.

Remember, there’s never been a better time to buy REITs and live off their dividends. But it’s important to choose wisely. Retail REITs are dangerous, while other recession-proof issues are bargains. I’d love to share the latter with you – including specific stock names, tickers and buy prices. Click here and I’ll send my full 8% No Withdrawal Portfolio research you to right now.