Mortgage rates reached a new milestone last week, and it’s one of the most important—and underreported—events in economic history.

For the first time ever, 30-year mortgage rates fell below 3.99%, on average. This is stunning for several reasons, but the most important is that the Federal Reserve is actively working to get mortgage rates higher. By increasing its Federal funds interest rate target, the Fed is hoping to make borrowing more expensive for everyone—companies, students and, yes, homebuyers.

But it’s not working.

And perhaps the biggest reason why it’s not working is that bond investors don’t think economic growth is going to strengthen, so they’re effectively daring the Fed to keep raising rates. In fact, bond investors have gotten so confident that the Fed won’t be able to raise rates quickly that they’ve helped lower the yields of long-term Treasuries, which, in turn, has helped drive mortgage rates down, since the two are tangentially linked.

This has taken a lot of people by surprise, including mortgage bankers themselves. Remember when bank stocks, like Wells Fargo (WFC) and Bank of America (BAC), soared late last year? A big reason for that bull run was an expectation that interest rates would keep going up, thus fattening these lenders’ profit margins.

Now that isn’t happening, which leads us to wonder whether financial stocks are overbought. That isn’t an easy question to answer, because lower mortgage rates might actually encourage more people to take out home loans and buy houses.

Instead of trying to figure out this enigma, we’re going to jump on an easier way to benefit from the low interest rates we’re seeing in the mortgage market: real estate investment trusts.

REITs are set up to invest in real estate, then pass on the vast majority of the income they earn from renting out that real estate to shareholders. With some REITs paying out yields of 6% or more, it’s no surprise that they’re popular among retirees.

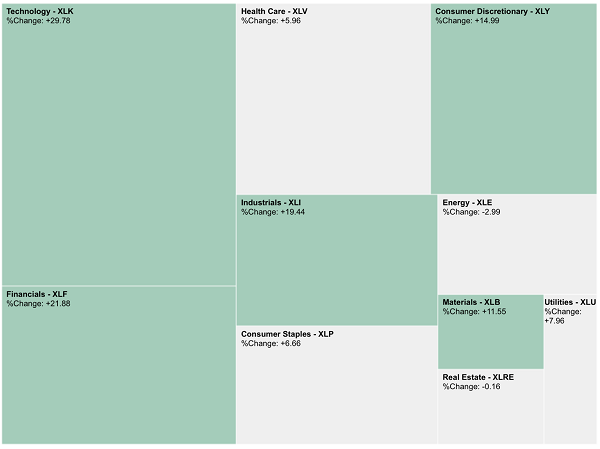

But REITs have been doing awful as of late. In fact, they’ve been one of the worst-performing sectors over the last year:

REITs Get Little Market Love

But REITs are ideally positioned to benefit from the unexpected low-mortgage trend for two reasons.

First, low mortgage rates will mean more demand for property, which will drive property values higher. Since REITs hold most of their assets in the form of real estate, this is a balance-sheet bonanza. Higher demand is going to boost REIT book values … and the market hasn’t priced this in yet.

The second reason why REITs will benefit is that they will be first in line to use mortgages to buy choice properties. Although not technically called mortgages, the loans REITs use to invest in real estate carry interest rates that go up and down with mortgage rates. And lower rates mean REITs will be able to borrow even more cheaply, letting them get bigger through property acquisitions that will, in turn, drive their earnings higher.

Despite these wonderful tailwinds, the sector is getting little market love. So it’s time for us to be a contrarian and snap up some REITs.

Avoiding the Wrong REIT

On days when REITs are beaten down, everything looks undervalued. But investors have abandoned some recently hard-hit firms for good reasons.

A good example: Wheeler Real Estate Investment Trust (WHLR), which is down a shameful 31% year to date. Not many people saw that coming, since the REIT was trading in a narrow range until it finally collapsed last month:

A Steep Downturn

What happened? A dividend cut, of course.

Wheeler slashed its $0.42-per-share quarterly payout by 19%, which was inevitable given that the prior quarter’s funds from operations (FFO) was only $0.15 per share. Crucially, this is also far short of the new lower payout, suggesting another dividend cut is on the way.

That’s partly why WHLR is now yielding over 14%. And as appealing as that sounds, the firm’s failure to earn dividends from rental income means that payout will get cut again.

Could we have predicted this beforehand?

Yes, actually—but it wouldn’t have been easy. A close look at the firm’s earnings results over the last two years would demonstrate Wheeler’s limited ability to sustain its dividend, but you’d have to look at the firm’s rental incomes to see Wheeler’s biggest problem: lending rates.

That’s right, Wheeler has to pay lenders a very high interest rate to borrow money that it can use to invest in real estate, and that interest rate is too high relative to the rents it can earn. Wheeler has borrowed money at 8% and 9% interest rates in recent years, which is higher than what most REITs pay. In fact, you may be able to get a mortgage for a much lower rate then Wheeler … and go on to start your own real estate business!

It’s true that the gross rental revenue Wheeler gets exceeds that 8% to 9% borrowing cost, but don’t forget that Wheeler’s management charges fees, and the trust has to pay operating expenses, sales commissions and so on.

The result is not good—Wheeler actually reported a net loss attributable to shareholders in the last quarter. And if management can’t grow out of this problem by borrowing, the whole company is doomed.

REIT Funds to Consider

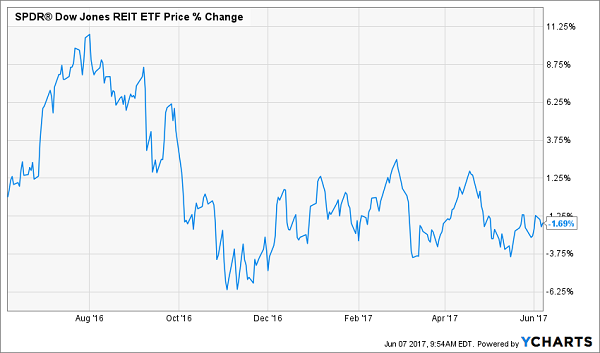

This is complex stuff, and many investors may be best off diversifying with a REIT fund like the SPDR Dow Jones REIT ETF (RWR), which focuses on large cap firms and offers a decent 4% yield. The fund is down slightly from a year ago, alongside the broader REIT market:

A Slight Loss With RWR

Of course that’s a much nicer looking chart than that of Wheeler! But some REIT funds have done better. There are funds like the Principal Real Estate Income Fund (PGZ), which is up a nice 10% from a year ago, thanks to its 9.7% dividend yield. However, PGZ doesn’t actually invest in real estate—it invests in mortgages, so it may get hurt if mortgage rates stay low and the Federal Reserve boosts its interest rate target.

How about another solid-performing real estate fund that actually invests in REITs, like the RMR Real Estate Income Fund (RIF)? Not only does this fund have some solid-performing REITs in its portfolio, like the skyrocketing Digital Realty Trust (DLR), but it also pays an impressive 6.2% dividend yield and is easily covering that payout with capital gains and investment income.

RIF also has the distinction of being one of the most heavily discounted REIT funds out there, since it’s currently selling at about a 17% discount to its net asset value.

4 Safe 7.0%+ Yields Hiding in Plain Sight

A 17% discount to net asset value (NAV, or the value of a fund’s underlying assets) is nice, but that’s no guarantee of a superior return.

In fact, I just released a new FREE report that reveals 4 other funds trading at narrower discounts than RIF, but all 4 are practically locked in for much bigger gains. I’m talking about easy 20% price upside in the next 12 months here!

It goes to show you that basing your investment decisions on a single indicator is a recipe for mediocre returns at best … and disaster at worst!

The best part: My 4 top fund picks pay incredible 7.5% yields, on average, right now. That’s 20% more than you’ll get from RIF today.

Oh, and before you ask, yes, these yields are safe: all 4 funds easily generate enough investment returns on their holdings to cover their massive payouts, and they give you far more diversification than if you just piled all your cash into REITs—as appealing as they are right now.

I can’t wait to show you the surprising secret behind these high, safe yields and give you everything else you need to know about these 4 little-known funds. Simply click here to get your own copy of this bombshell FREE report and kick-start your own safe 7.5% income stream now!