You may think $500,000 isn’t enough money to retire on.

It is. Because with two quick steps, you can transform any $500K “buy and hope” portfolio into a $3,279 monthly income stream:

- First, sell everything. Including the 2%, 3% and even 4% payers that simply don’t yield enough to really matter. Then,

- Buy my 8 favorite monthly dividend payers.

The result? $3,279.69 in monthly income every month (from an average 7.6% annual yield, paid every 30 days).

With upside on your initial $500,000 to boot!

Traditional dividend stocks simply can’t keep up, and I’ll show you why. Let’s take a 4-pack of popular names Procter & Gamble (PG), McDonald’s (MCD), Altria (MO), and General Mills (GIS) to illustrate how much they’ll pay investors the rest of the year.

I chose Mickey D’s to keep the quarterly timing fair, as they’re due for a dividend payment next month and again in December. But you can choose any four dividend aristocrats you like. It won’t matter – they’ll all get trounced by my consistent monthly payers like this:

Consistent Monthly Payouts

“But… but… you’re forgetting dividend growth!” I can hear the aristocrat fanboys stammering now.

I’m not forgetting growth. First, I accounted for likely dividend hikes for Altria and McDonald’s in October and December respectively.

Secondly, and more importantly – when executed correctly, this strategy actually captures more upside than “America’s best blue chips.” I know this because since inception, my Contrarian Income Report readers have enjoyed 14.3% annualized gains versus 11.5% for the S&P 500 over the same time period.

And this strategy isn’t capped at $500,000. If you’ve saved a million (or even two), you can just buy more of my elite eight monthly payers and boost your passive income to $6,349 or even $12,698 per month.

Though if you’re a billionaire, sorry, you are out of luck. These Goldilocks payers won’t be able to absorb all of your cash. With total market caps around $1 billion or $2 billion, these vehicles are too small for institutional money.

Which is perfect for humble contrarians like you and me. This ceiling has created inefficiencies that we can take advantage of. After all, in a completely efficient market, we’d have to make a choice between dividends and upside. Here, though, we get both.

Heck, This Grandma Makes $387,000 Last Forever

Recently I was chatting with a reader of mine who manages money for a select group of clients. He’s using my No Withdrawal Portfolio to make a client’s modest savings – a nice grandmother with $387,000 – last longer than she ever dreamed:

“She brought me $387,000,” he said. “And wanted to take out $3,000 per month for ten years.”

“Well she’s already withdrawn money for eight months (at $3,000 per month) and her balance has actually grown to $397,000. If the portfolio continues yielding 7% per year plus 2% per year in capital gains, and she withdraws $3,000 per month, it will pay my fees and still last her 27 years!”

Now many retirement experts pitch real estate as the best way to bank monthly income. But this grandma isn’t hustling to collect rent checks, or fix broken light bulbs. She’s simply collecting her “dividend pension” every month, which is 100% funded by her stocks and funds.

Actually her monthly salary is more than 100% financed – which is why her portfolio has grown by $10,000 as she’s withdrawn $3,000 per month.

How is This Possible? With “B-List” Cash Cows

If you’ve researched monthly dividends before, you’ve probably come across Realty Income (O). This real estate investment trust (REIT) was the first to stake its claim as “the monthly dividend company.” In fact, it trademarked the phrase!

Realty Income has been a fantastic investment through the years. But there’s a problem with popularity – low yields:

The Bear Market in O’s Yield

And unfortunately for investors, the Big O is more popular than ever at a time when its investments are shakier than ever. As a retail landlord, it’s a crapshoot every month as to which rents are going to get paid – and which tenants will succumb to “Death by Amazon.”

As with stocks, we can’t just buy any monthly payer. We must focus on the bargains that mainstream sites and newsletters don’t talk about.

B-List Feature: A Discounted Cash Cow

Here’s an example. Last May, I recommended a closed-end fund (CEF) run by the renowned PIMCO. Its funds are rarely bargains, but its PIMCO Dynamic Credit and Mortgage Fund (PCI) was misunderstood – and cheaper than it should have been. At the time, I wrote:

One corner of the investment universe is still depressed – it’s under a cloud atoning for sins from a decade earlier. Just as militaries tend to fight the last war, investors tend to fear the last crisis. They’re still scared of these assets, so their prices remain artificially depressed.

These asset are mortgage-backed securities (MBSs), and they had the lead role in the last financial crisis. They have recently been immortalized in the book and movie The Big Short. MBSs blew up the financial system in 2008 and have been outcasts ever since.

But a “second-level” look at mortgage payments shows these assets have successfully completed financial rehab. And they’re beginning to enjoy the benefits of clean living – defaults and delinquencies are down while credit scores and down payments are up.

PCI was paying a 10% annual dividend (or almost 1% per month), fully funded by the profits from its bond investments. The fund itself, meanwhile, was so out-of-favor that it was trading at a 10% discount to its net asset value (NAV). Which means we were able to buy its assets for just 90 cents on the dollar.

That gave us three ways to profit:

- The fund’s safe 10% yield,

- The likelihood that its discount window would narrow or close altogether, and

- Rising NAV thanks to the best bond managers on the planet.

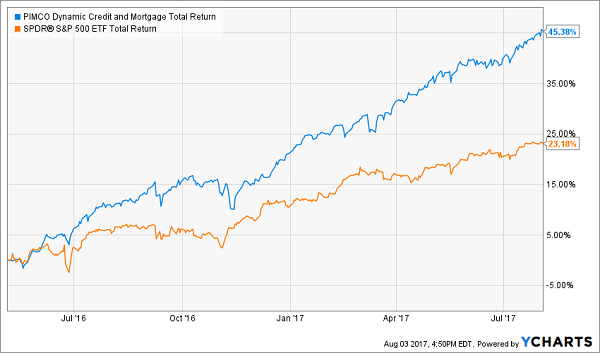

We cashed in all three. Meanwhile the S&P 500 did fine, but it really only has one way to win (you buy it and hope it goes up). So it was no contest – even though the S&P did in fact rise an impressive 23.2%.

However we enjoyed 45.4% total gains and doubled up the broader market in just 15 months – while receiving fat dividend payments every month to boot:

Dividend or Growth? Why Choose!

Today the “free money” discount window is completely closed. But there are still promising places for meaningful monthly income and price upside today.

My Top Elite 8 Monthly Payers for 7.9% Dividends, Plus Upside

My all-star retirement portfolio contains 8 of the absolute best preferred stocks, REITs and CEFs out there. It’s well diversified across all types of investments and sectors, and the cash flows funding these dividends will do well no matter what happens in the broader economy or stock market.

Plus, relentless dividend growth means your 7.9% yield will be more like 10% in short order.

I’m ready to take you inside this “no-worry” retirement portfolio now. Click here and I’ll show you the 8 bargain investments inside it and give you their names, tickers, buy-under prices and much more.