“Don’t you own that, B.O.?”

Go figure. While some people are thought of for their jokes, their hobbies or their families, a reader thought of me when they read about a Vanguard fund underperforming of late.

The poor ol’ Vanguard Dividend Growth Fund (VDIGX). Longtime readers know I’ve yapped about this before. While I rarely mention (let alone endorse!) mutual funds, VDIGX is notable for two reasons:

- I plow 100% of my 401(K) contributions into this fund, and

- It’s a pretty good option as far as retirement plans go.

Why this fund? Because in my “Brett Inc.” company plan, I have a set list of Vanguard funds to choose from. This is “set-it-and-forget-it” money, so my goal is to maximize long-term returns. The best way to do this, of course, is to buy dividend growth stocks.

My own portfolio dedicated to this approach has earned 15% per year. I’ll share the details with you in a minute.

But first, what has Vanguard Dividend Growth been up to? Lawrence Strauss, who conjures up some relatable income ideas over at Barron’s, recently caught up with VDIGX manager Don Kilbride:

(Don’s) not happy about the fund’s relative underperformance recently. Its year-to-date return is about 8.9%, placing it near the bottom of its Morningstar large-cap blend category. “I’m disappointed [but] I’m not necessarily surprised, given what the market has chosen to value versus what it has chosen to ignore,” he says.

Let’s give credit where credit’s due. Over the long haul, the VDIGX has done well for itself. Its 10.8% average annual return is 141 basis points better than the category average over the past 15 years, and better than 93% of its peers.

But with all due respect, unless you’re also forced to invest within a Vanguard 401(k), we can improve on this portfolio by buying dividends with the will (and the cash) to grow their dividends at a brisker pace than the “low double digits” VDIGX’s holdings historically have grown their payouts at.

In fact, we can grow our payouts by almost twice as much—at a forecasted average of 22.6%—by turning to the DIVCON system.

DIVCON is primarily known for being a dividend safety system. However, it ranks more than a thousand dividend-paying stocks not just on their ability to maintain their payouts, but also their ability to grow them over time.

DIVCON looks at some telling metrics to compile its rankings. For instance, it likes a high levered free cash flow-to-dividend ratio, which means there’s ample cash left over after making the regular distribution. Lots of cash left over means the dividend is well-covered, with plenty of headroom for larger dividends.

It also looks at share repurchases to dividends. Why? Because if the economy gets really turbulent, a company that currently spends a lot on repurchases could cancel those buyouts to keep the dividend running while still conserving cash.

That’s thinking ahead.

Best of all, DIVCON filters all this data down into a simple 1-to-5 scale. DIVCON 1 or 2? Weak dividends that could be cut in the future. DIVCON 3? An OK payout.

And DIVCON 4 or 5? Well, those are stronger, better-funded dividends with a higher likelihood of growing down the road.

So if you’re looking to beat Don at his own game, consider these four stocks that are projected to expand their dividends by an average of nearly 23% over the next year.

L3Harris Technologies (LHX)

Dividend Yield: 1.9%

Expected Dividend Growth: 18.7%

L3Harris Technologies (LHX) is a defense contractor and technology services provider with a laundry list of products for governmental, defense and even commercial applications.

Among its offerings? The Sky Warden Intelligence, Surveillance and Reconnaissance (ISR) Strike Aircraft, T7 Multi-Mission Robotics System (think explosives disposal), Ageotec remotely operated underwater vehicles, CellDefender Cellular Access Management System and more.

LHX, like the rest of the stocks we’ll talk about here, is a DIVCON 5, meaning these payouts just don’t get much safer.

But they could get bigger.

L3Harris receives high marks for its levered FCF, which is more than three times what it needs to cover its $1.02 quarterly payout. That represents a hefty 20% increase over 2020’s dividend, which was announced not long after LHX reported 13% profit growth for 2020.

DIVCON thinks there’s more where that came from, projecting 19% dividend growth the next time LHX raises the bar. That’s great news for shareholders, as L3Harris is a perfect example of a stock that likes to chase its payout higher.

Like Birds of a Feather

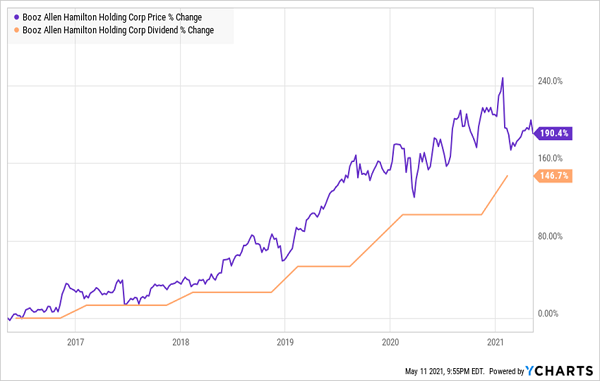

Booz Allen Hamilton (BAH)

Dividend Yield: 1.8%

Expected Dividend Growth: 22.3%

Another familiar face at the DoD is Booz Allen Hamilton (BAH), though its expertise is less on the battlefield and more so … well, almost everywhere else.

BAH provides consulting, analytics, engineering, cybersecurity and other services for civil government, defense, the intelligence community and Homeland Security, but also the private sector, across health, transportation, energy and utilities.

Booz Allen has delivered pretty steady growth for some time, with five consecutive years of revenue growth, and fatter profits in seven of the past eight years (including 2020). And it’s happy to share the wealth. The payout has well more than doubled since 2017, from 17 cents then to this year’s fresh 37-cent quarterly distribution—itself a juicy 19% better than in 2020.

DIVCON notes that Booz Allen has more than 700% of the levered free cash flow it needs to pay its shareholders. So no wonder, then, that the system thinks the BAH dividend will be 22.3% higher around this same time in 2022.

Another Faithful Dividend Tracker

Best Buy (BBY)

Dividend Yield: 2.2%

Expected Dividend Growth: 22.6%

Electronics retailer Best Buy (BBY) has provided Wall Street with pleasant surprises for years.

People always remember the threat Amazon.com (AMZN) posed to Best Buy thanks to “showrooming” and the general trend of consumers toward e-commerce. But they forget that, before that, Walmart (WMT) and Target (TGT) had started trying to eat its gadgetry lunch.

While it’s still not quite the powerhouse it once was, everything has been pointed in the right direction. Three straight years of revenue growth. Best Buy has also been soundly profitable ever since absorbing losses back in 2012-13, and it appears to be on its way to a third consecutive year of earnings growth.

And if you haven’t been paying attention, you might be surprised to find out that it’s thrilling income investors, too.

The 2.2% yield isn’t much to look at, sure. But payouts are up 106% since 2017, including a fat 27% jump this year to its current 77-cent quarterly dividend. That’s in large part because it’s a sneakily strong cash generator, with DIVCON noting that BBY has more than seven times what it needs to cover the payout at current levels.

That makes its projection for nearly 23% dividend growth by next year sound plenty realistic indeed.

Best Buy’s Comeback Story Is Told Through Its Dividend, Too

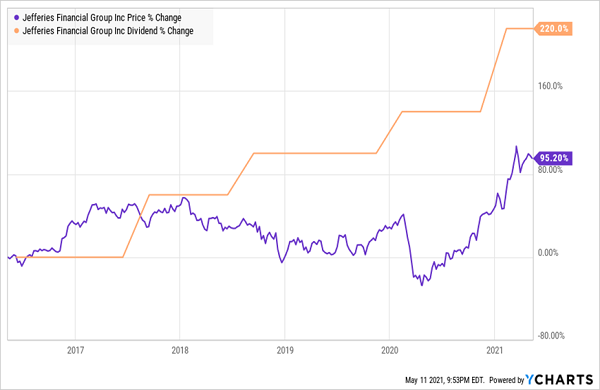

Jefferies (JEF)

Dividend Yield: 2.4%

Expected Dividend Growth: 26.9%

Investment banking firm Jefferies (JEF) provides clients with asset management, brokerage, financial advisory, research and IPO underwriting services.

This is a business that is inextricably linked to the markets, so its operational performance tends to be far more cyclical than the other dividend growers we’ve evaluated so far. It made $171.7 million on $4.8 billion in revenues in 2017. In 2018, it made $1.2 billion on sales of $5.2 billion. And last year? $775.2 million on nearly $7 billion in revenues.

But thanks to adept fiscal management, Jefferies has turned into quite a dividend-growth powerhouse. This year’s 20-cent-per-share quarterly dividend is 33% better than it was last year, and more than triple the 6.25 cents it was paying just four years ago.

And If Jefferies’ Stock Catches Up … Watch Out Above!

Despite this, we could actually accuse Jefferies of being quite the penny pincher.

DIVCON data says that the financial firm has 1,681% of the cash it needs to keep the dividend checks flowing!

Don’t expect the acute financial minds at Jefferies to start doubling the payout every year to catch up … but do expect the dividend growth to keep up a brisk pace.

7 Stocks That Can Deliver 15% Yearly Returns … For Life!

This is a simple but potent recipe for success that has proven itself to investors again, and again, and again:

- Step 1: Buy aggressive dividend growers that are actually expanding their businesses, too.

- Step 2: That’s it! There is no Step 2! Just keep targeting elite dividend growers!

If you invest your money with corporate managers who both effectively deploy capital for growth and know how to reward shareholders, you will clobber the market on a regular basis—and better still, as the years roll on, more and more of those returns will come from cold, hard cash.

Valuation is becoming a real concern with several of the stocks outlined above, so consider them stocks to monitor for better opportunities later.

But you can still put this income-printing strategy to work today with a simple-to-manage, easy-to-understand group of just 7 specific tickers that can deliver a steady 15% every year—for life!

These seven stout income picks follow the exact same playbook as Jefferies or L3Harris, growing their businesses and their dividends.

In fact, they all have one critical thing in common: They’re quietly handing smart investors growing income streams plus annual returns of 15%, 17%, 21% or more!

And they’re trading at far more attractive prices—a value proposition that will further boost our price returns over time.

Your next move is simple: Buy now and set yourself up for annual returns of at least 15%. That’s easily enough to outrun any inflationary wave we’ll see, because a return like that would double your nest egg every 5 years!

You can get the full breakdown on each of these 7 standout buys within seconds. Click here to get my complete research: names, tickers and a full breakdown of their operations—everything you need to buy with confidence.