Most financial advisor hacks are dead wrong. You CAN comfortably retire on a modest $500,000 investment portfolio.

Of course you’ve heard the warnings that retirement is getting harder – and they’re true. With U.S. Treasuries paying paltry returns, it is harder to find a risk-free income stream for your golden years.

But there are low-risk “bond proxies” that can offer over $50,000 in dividends per year on an initial investment of $500,000. All you have to do is buy now and sit tight. The secret is a superstar dividend growth portfolio that follows a few simple principles.

First, we don’t want to overpay – so we’re only going to choose stocks with P/E ratios below 25 (and most of these stocks actually have a P/E ratio below 20).

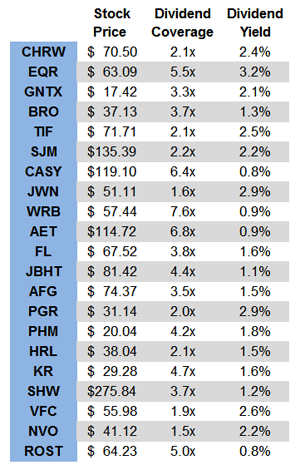

Second, we want solid dividend coverage. This means each stock’s earnings-per-share (EPS) for the last year is greater than its total dividends paid over the same time period. Some stocks, like Casey’s General Stores (CASY) have massive dividend coverage (Casey’s EPS is over 6-times dividends paid).

We also want companies that are growing, so we’ll choose companies who have boosted their revenues over the last 5 years.

Finally, we want a history of dividend growth, meaning we’ll require a half-decade of meaningful payout raises.

From there, I hand-picked my favorite 21 stocks. It’s a diversified portfolio that includes homebuilders, cyclicals, counter-cyclicals, retailers, biotechs, luxury goods, consumer staples and financials.

Note I did not mention technology (too popular today, in my opinion) and energy (too volatile). I want dividends, stable growth, predictability and reasonably priced companies – so I’m avoiding these sectors.

Here’s a breakdown of our current holdings, with their stock prices, dividend coverage (we required greater than one, the higher the better) and dividend yield:

Safe Dividends With Upside

Don’t be fooled by this portfolio’s low current yield of 1.8%! We’re not buying this portfolio for passive income today—we’re buying it for the dividends we will get in 10 years’ time. And that’s where compounding works wonders in our favor.

Safety, Growth and High Yields Over Time

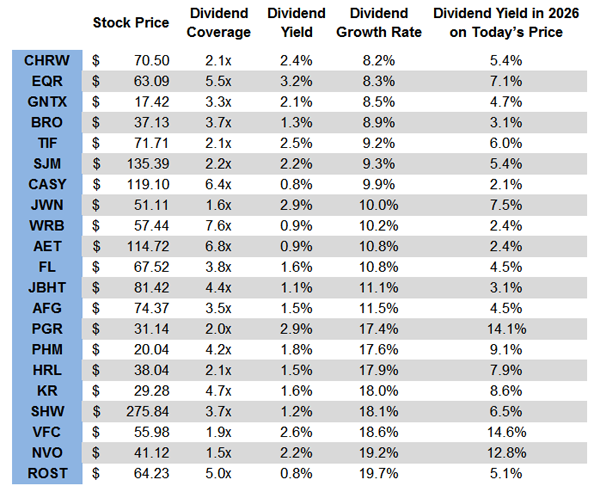

By 2026 our dividend growth rate means we will be netting much higher dividends based on our current price in 2016. Look at the 14% yields from VFC and PGR—extremely stable and high-margin companies with decades of proven earnings behind them. Not bad.

In fact, the entire portfolio now yields 6.5% – meaning we’re getting $2,708 monthly income from our initial $500,000 investment today! Now we’re getting somewhere.

And it gets better. The power of dividend growth investing makes compounding work in your favor twice. First, you get the dividend growth as the companies increase payouts. But you also get the growing capital base from reinvested dividends if you practice dividend reinvestment.

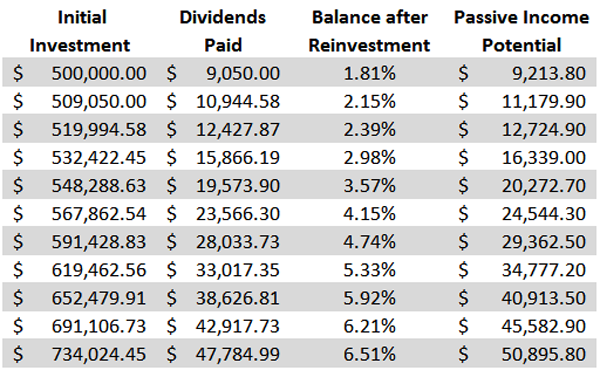

With that in mind, let’s look at how reinvested dividends increases our income stream in a decade:

The Power of Compounding

Look at the total in the bottom-right – it says there is $50,895.79 in annual passive income from dividends thanks to reinvested dividends. That’s $4,241 in monthly income, and a yield of 10% on our initial $500,000 investment.

And believe it or not, this figure is still conservative. We’re still assuming no additional investments over a 10-year period and we’re ignoring capital gains and portfolio rebalancing—strategies that would likely grow our investment even more.

This is the power of compounding. And notice how it doesn’t even take all that long to start working. We tend to think about retirement as the end of a 40-year career (or longer). We hear doom and gloom about insolvent Social Security, the impossibility of retiring in today’s low-rate world and a bunch of other nonsense that is supposed to scare us straight into the arms of expensive money managers and investment advisors.

Ignore that noise. Instead, look at the numbers and the power of selective investing in high-quality stocks with a strong history of dividend growth.

But what if you need a greater income stream today?

There’s a way you can have your dividend growth and cash your dividends too with my “no withdrawal portfolio.” It lets you live off the income stream from dividend payouts without ever selling a share.

After all, why rely on stock price appreciation in an inflated market when there are secure, high paying dividends you can simply live off of and keep your capital intact?

Most investors know this is the right approach to retirement. Problem is, they don’t know how to find 7% and 8% yields to fund their lives.

That’s why I specialize in finding safe, under-the-radar high income options. Click here and I’ll explain more about my no withdrawal approach – plus I’ll share the names, tickers and buy prices of my two favorite high income plays for 7.6% and 7.7% yields.