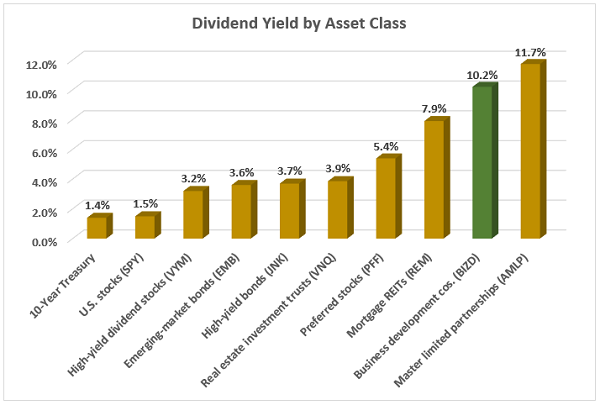

Anyone up for a 10.2% payout? One that is powered by profits that should actually rise alongside interest rates?

If so, I’ve got a three-letter acronym for us:

B-D-C.

Business development companies provide debt, equity and other financing to small and midsized companies, effectively acting as banks because banks often don’t want to take on that level of risk. And because they’re primarily investing in companies that aren’t on public markets, BDCs serve as de facto private equity investments—but ones that retail investors like us can get in on!

BDC structures are similar to real estate investment trusts (REITs). Both were created by Congress—REITs in 1960, BDCs in 1980. And both enjoy special tax privileges, but on the condition that they return at least 90% of their taxable profits to shareholders as dividends.

But BDCs pay a lot more than REITs right now. In fact, BDCs are doling out 2.6x more—a terrific 10.2% yield:

Many BDCs also tend to thrive as rates rise. That’s because they extend loans to small businesses, and often times, these loans have a “floating rate” component extended. Thus, higher rates mean more profits.

Let’s remember, however, that there’s no such thing as a risk-free 10% yield. Stock-picking in the BDC space is always challenging. We must carefully consider the loans that BDCs extend before we buy them. Today, we’ll look at three of them, paying between 8.9% and 9.6%.

Ares Capital (ARCC)

Dividend Yield: 8.9%

Ares Capital (ARCC)—the largest BDC by market cap at just under $8 billion—is considered a blue chip in the space. If a business needs financing, Ares will find a way. The BDC will invest in a number of ways—anything from revolver debt, first and second lien loans, unitranche, non-control equity and more—across a number of transaction types, including growth capital, recapitalizations, general refinancing, restructurings and acquisitions.

ARCC’s investments are spread across 350 portfolio companies in a number of industries, but most prominent at the moment are healthcare services, software/services, commercial and professional services and consumer services. Target companies typically generate anywhere between $10 million and $250 million in EBITDA.

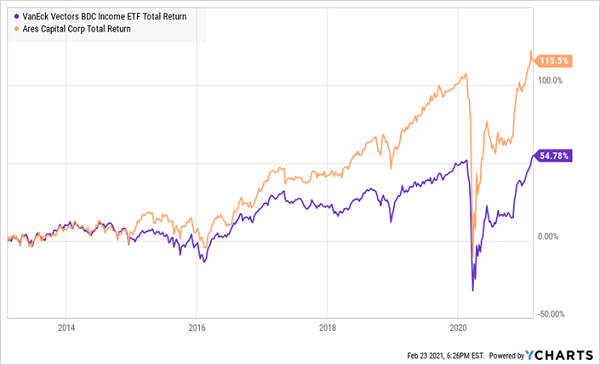

And it’s a standout compared to its peers.

ARCC Is a Perpetual Outperformer

ARCC shares’ rebound has continued over the past few months in part because of optimism over rates; 84% of its total investments, at fair value, are floating-rate in nature.

Shares recently hit pause after the company’s Q4 earnings, but there were plenty to like in the numbers. Net investment income (NII) of 54 cents per share was well better than estimates, and came on the back of record originations. It also represents 135% of what it needs to cover its 40-cent quarterly dividend.

Credit quality improved, too, and non-accruals (when payments are 90 days or more past due) declined to 3.3% at cost, compared to 5.1% in Q3.

Ares Capital trades roughly 6% above its NAV—a modest premium to the value of its portfolio.

BlackRock TCP Capital (TCPC)

Dividend Yield: 9.6%

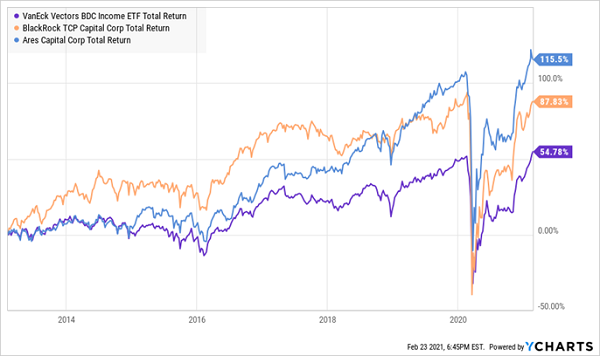

BlackRock TCP Capital (TCPC), whose portfolio is about 92% floating-rate, also compares well with BDCs-at-large.

TCPC: Not Elite But Beats the Pack

BlackRock TCP Capital, which outsources its management to Tennenbaum Capital Partners, an indirect BlackRock subsidiary, primarily invests in the senior secured debt of middle-market companies worth between $100 million and $1.5 billion in enterprise value. While its portfolio is smaller than ARCC’s, its 101 investments still provide a wide range of exposure.

Here, internet software and services, diversified financial services, software and textiles/apparel/luxury goods are the biggest slices of the pie, but even that only represents less than 40% of its firms; the rest is split among another 20 or so industries.

The company hadn’t yet reported Q4 earnings, but its preliminary release was encouraging. Net asset value was expected to improve by about 4% from the previous quarter, to $13.22-$13.25 per share, which would indicate shares are trading at a roughly 6% discount. Also, its NII range of 34-35 cents per share was better than expected, and easily covers the 30-cent dividend.

That’s encouraging, but BlackRock TCP Capital is playing with something of a handicap. Unlike Ares, which has provided some dividend growth in recent history and maintained its regular payout throughout the downturn, TCPC’s payout has gone nowhere for years and was reduced by more than 16% last summer. We retirement investors prefer payouts that we can count on.

PennantPark Floating Rate Capital (PFLT)

Dividend Yield: 9.5%

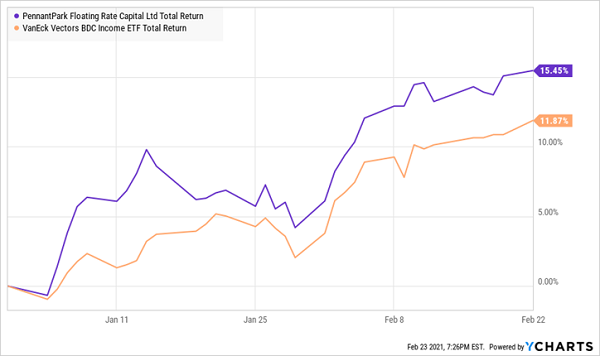

The name says it all. PennantPark Floating Rate Capital (PFLT) invests in middle-market businesses almost entirely through floating-rate senior secured loans. And that exposure is giving it an edge in 2021.

PFLT Is Off to a Hot Start

PFLT current portfolio includes a tidy 100 investments, scattered across industries such as aerospace, education, retail, financial services and transportation.

Q4 saw its net asset value improve by 4.3% to $12.32 per share, implying a modest 3% discount at current prices. That, and a 9.5% yield—paid monthly—are intriguing.

Dividend safety, on the other hand, isn’t so great. Its most recent quarterly NII was just 91% of what it needed to fund its payouts. That’s bad. What’s worse is that Janney Montgomery Scott’s analysts are predicting that PennantPark Floating Rate’s NII won’t cover the dividend in 2021 or 2022.

Sky-High Dividends You Can Count on For DECADES

What good is a nearly 10% yield if it could suddenly drop to 8%, 6% or worse overnight?

You’d flip your lid if your employer suddenly slashed your pay without warning. It’s no different for retirement investors that rely on dividend consistency to make it through their golden years.

Fortunately, that’s something investors in my “Perfect Income” portfolio never have to worry about.

Even blue-chip dividends dropped like flies in 2020 as the pandemic poked holes in supposedly solid companies. That has sent income investors scattering for better sources of income, but unless you perfectly bought the March dip, you’re mostly out of luck. Even if you had a million dollars in cash to plunk down right now, the S&P 500 would earn you just $15,000 a year! You’d do even worse with a traditional 60/40 portfolio!

Forget about retiring happily on that level of income. You can’t even survive on it!

Thankfully, the dividend-rich stocks in my “Perfect Income Portfolio” can and do deliver so much more.

Most of my readers have told me that these stocks have doubled and even tripled the dividends they were earnings from their old income portfolios. (And in a couple of rare cases, readers reported a 4x jump in their regular checks!) That alone is an upgrade, but the Perfect Income Portfolio delivers that level of cash while also …

- Paying those dividends consistently, predictably and reliably.

- Surviving, even thriving, in market crashes.

- Delivering double-digit returns across several safe investments.

- Gambling your hard-earned nest egg on flimsy day-trading strategies, options contracts or penny stocks.

Stop obsessively staring at your 401(k) or IRA while it yo-yos up and down. You don’t need to pray to the Federal Reserve to keep your retirement hopes alive.

Instead, just let me show you the stocks and funds you need to stabilize your retirement … and even teach you more about this incredible strategy itself, so you better understand exactly what you’re investing in.

Take control of your financial legacy today. Let me show you how to get 2x to 4x your current income with this simple, straightforward system. Click here to get a FREE copy of my Perfect Income Portfolio report, including tickers, buy-in prices, dividend yields, full analyses of each pick … and a few other bonuses!