Today I’m going to give you a shot at the next Texas Instruments (TXN), which has delivered a dividend that’s surged 104% since members of my Hidden Yields service bought it in 2017.

Or the next Jefferies Financial Group (JEF), whose dividend has popped 67% higher in the last year alone.

The key to breakneck payout growth like this is investing in megatrends that reshape society. Right now, we’re tracking six:

- Technology, as it reshapes all our lives in the COVID era.

- Healthcare, as more people pay attention to their health (and more employers entice scarce workers with enhanced medical benefits).

- The surging finance sector, as inflation becomes more than “transitory”—sorry, Jay Powell—and interest rates rise. (More on this in a second.)

- Soaring industrials, as supply-chain woes get worked out and demand continues to soar.

- Dine at home, which, despite what the talking heads on CNBC say, still has legs as the Delta variant tightens its grip.

- Smart retail, which is all about companies that leverage their e-commerce businesses with well-run stores at which consumers pick up their orders—fueling some nice “knock-on” sales. Think winners like Best Buy (BBY) and Home Depot (HD). It’s a savvy setup that Amazon.com (AMZN) can’t beat.

To make it simple for you to “track and trade” these shifts, our Hidden Yields premium portfolio is split into six “buckets,” one for each trend. They contain specific stocks, complete with clear buy, sell and hold recommendations on each.

These buckets also tell you in an instant how to weigh each of these megatrends. All you have to do is tally up the buy recommendations in each one!

Finance Pullback, Rising Rates Set Us Up for Gains (and Surging Dividends!)

These days, we’re focusing on financial stocks, with all five names in this bucket listed as buys, as banks and insurers cash in on the “yield curve,” rewarding shareholders with surging dividends as they do.

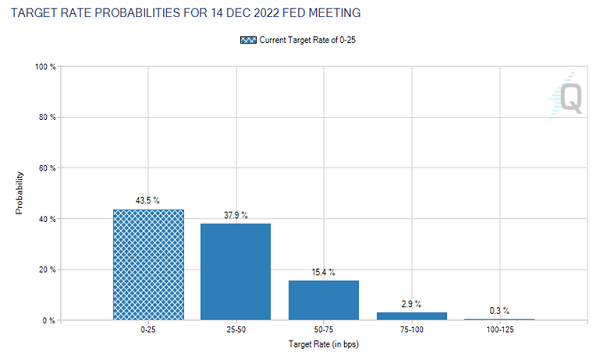

At one end of the curve is Jay Powell’s overnight-lending rate, at which banks lend to each other. It’s pegged at zero, where it’ll likely remain until late next year, according to traders wagering through the Fed funds futures market:

Source: CME Group

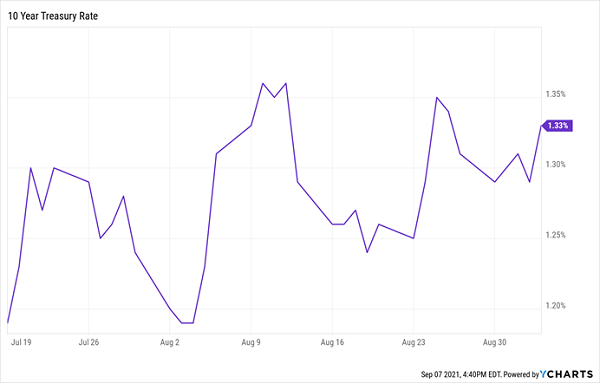

Then there’s the other end of the curve—the yield on the 10-year Treasury note, which Powell can’t control.

It’s the benchmark for the loans banks offer to consumers and businesses, and it rises with inflation; banks profit on the difference between the two rates. And since the yield on the 10-year bottomed in July, it’s been grinding higher:

10-Year Treasuries Climb, Taking Finance Profits With Them

I’m sure you can see where I’m going here: with the Fed’s key lending rate at zero for at least the next year and the yield on the 10-year rising, we’ve got a setup for continued finance-sector profits (and rising dividends, and share prices, too!).

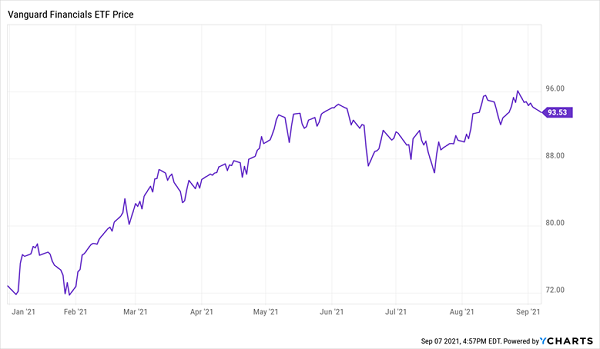

At the same time, financial stocks, shown below by the Vanguard Financials ETF (VFH), have leveled off since their big run-up earlier this year:

First-Level Investors Discount Higher Rates—and Our Buy Window Opens

How high can the yield on the 10-year go? Recently, I sat down (virtually) with Adam McCabe, head of fixed income for Asia and Australia at Aberdeen Standard Investments, to get his take (even though Adam is focused on the Far East, he’s got his finger on the pulse of rates around the world).

He sees longer-term Treasury rates between 2% to 3%, assuming a continued slow recovery (leading the Fed to keep its key lending rate lower for longer) and higher inflation (which boosts the yield on the 10-year).

I agree—and the midpoint of his estimate, 2.5%, would put Treasury yields 88% higher than they are now. That means our buy window in finance is still wide open.

So what, specifically, are we going to buy? Well, it’s no coincidence that three of the five buys in our Hidden Yields Finance bucket are insurance stocks.

Insurers in the Rising-Rate “Sweet Spot”

Insurance, of course, is a great business. The smartest insurance companies generate tremendous amounts of free cash. (Which they can then shower upon us shareholders in the form of growing dividends.)

Insurers collect payments upfront from their customers but may not have to pay them out in claims for a long time, if ever. The companies invest that money—called the “float”—and pocket the income they earn.

Insurance can be an all-time gravy train. Warren Buffett figured this out early in his career and became one of the richest people on the planet. And in Hidden Yields, insurance stocks have been very good to us, with past sells resulting in profits of 92%, 58%, 28% and 20%:

Hidden Yields Insurance Stock Alumni

These companies invest their excess cash in the safest fixed-income securities, which, of course, haven’t paid much in recent months. But with the 10-year Treasury rate poised to rise further, float profits are due to follow.

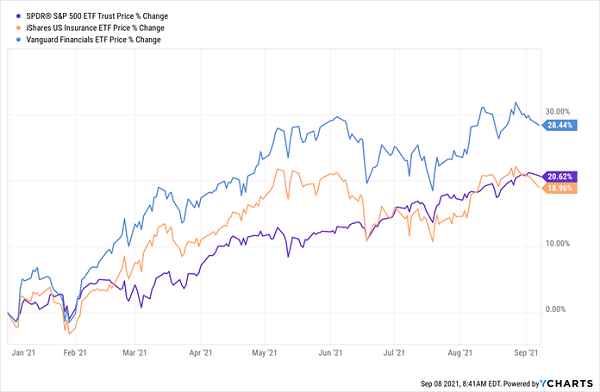

Here’s yet another sign insurers are a smart buy: the benchmark iShares US Insurance ETF (IAK) has lagged both the Vanguard Financial ETF (in blue below) and the S&P 500 benchmark SPDR S&P 500 ETF Trust (SPY), in purple, this year.

Insurers Ignored in the Rush Into Financials

Target Insurers With “Accelerating” Dividends

If you’ve been reading my columns on Contrarian Outlook, you know I talk a lot about a company’s “Dividend Magnet.” This just means that, over time, a company’s share price will tick higher with its dividend.

It’s inevitable!

So it follows that if you buy a company with a dividend that’s not only growing but accelerating, you’ll set yourself up for strong gains (and a bigger payout, too!)

To see this in action, look at Assurant (AIZ) from the table above, which handed us that 92% total return in just over four years. In the five years prior to my buy call, Assurant’s dividend magnet had been pulling its share price higher, point for point:

AIZ: Dividend Up, Share Price Up

That was more than enough to get our attention, so I issued a buy call in Issue No. 1 of Hidden Yields, which we released on September 18, 2015.

Over the next four years, AIZ kept following its dividend higher, until investors got a little too exuberant and the share price outran the dividend (a solid sell signal, as the dividend magnet can work in reverse, too—something we want to avoid):

AIZ Tracks Its Payout Higher—Then Caps Off Our Gains

As it turns out, our AIZ sale was savvy: in the nearly two years since our sale, the stock has risen 28%, trailing SPY’s 41% gain.

Where does that leave us? With a simple plan. We’re going to target insurers with:

- Accelerating dividends and …

- Share prices that lag their payout growth.

Then we’ll lock in as the yield on the 10-year grinds higher, driving rising profits for insurers and rising dividends (and share prices!) for us.

7 URGENT Buys to Double Your Nest Egg in 5 Years (or Less)

I’m going to save you the trouble of hunting down the next AIZ by doing it for you. All you have to do is agree to “road test” Hidden Yields for the next 60 days with no risk and no obligation whatsoever.

Your no-risk trial gives you immediate access to the service’s portfolio, including the names of all five urgent finance-sector buys and 23 rock-solid dividend growers in all.

I’ll also give you an exclusive Special Report outlining the 7 stout dividend growers I’m urging ALL investors to buy now.

These under-the-radar buys boost their dividends every single year, which yanks their share prices higher, as we saw with AIZ above. And thanks to their surging payouts and bargain valuations, I expect these stocks to deliver reliable gains and dividend payouts no matter what the market does.

Don’t miss your chance to get this breakthrough Special Report and your 60-day trial to Hidden Yields. The whole wealth-building package is waiting for you here.