We contrarians like to follow the insiders. Those “in the know” who buy and sell their own stocks based on value.

These “smart money” types fade sentiment. Insiders tend to buy low and sell high.

And, to be honest, we really don’t care when they sell. Maybe they were short of cash for a new yacht! Or a vacation home. Or a private jet. You get the idea.

More importantly, these insiders only buy for one reason, and one reason alone:

They believe their stocks are going to go up.

On that note, let’s discuss a few dividends yielding up to 11.9%—because the people who know the companies best are putting their money where their mouths are.

Insider buys are really noteworthy right now given the uncertainty in the financial markets. Which is why we want to follow the true dividend believers.

Let’s start with Kelcy and Bradford.

Energy Transfer LP (ET)

Dividend Yield: 9.8%

Recent Noteworthy Buys:

- Executive Chairman Kelcy L. Warren: 3 million shares ($37,795,500) between 5/12/23-5/24/23

- Executive Vice President Bradford Whitehurst: 10,000 shares ($124,300) on 5/30/23

A few months ago, I pointed out how billionaire Kelcy Warren was greedily gobbling up shares of master limited partnership Energy Transfer LP (ET). The co-founder and current executive chairman is only a couple years removed from stepping down from the CEO role, but he hasn’t lost his hunger for ET shares.

Indeed, over a roughly two-week period in May, he hoovered up another $38 million worth of shares! (Also worth noting is a six-figure purchase by EVP Bradford Whitehurst.)

Energy Transfer is responsible for nearly 125,000 miles of America’s energy infrastructure—according to the company, some 30% of the country’s natural gas and crude oil moves through its pipelines.

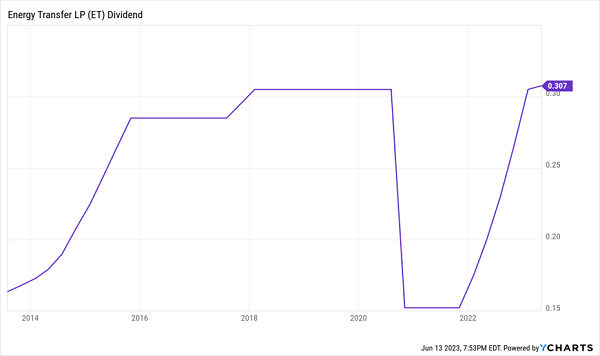

ET has delivered a much-appreciated comeback in its distribution. Energy Transfer, like other stocks, was shredded during the COVID bear market and “zero oil” crisis. The distribution was halved in 2020, from 30.5 cents per unit down to 15.25 cents. But a thorough recovery in the business has sent that distribution back north. As we predicted, ET announced another rate hike in late January to bring its distribution back to even at 30.5 cents per unit—and in April, Energy Transfer eclipsed that with a modest hike to 30.75 cents.

ET’s Distribution Is Back, Jack—Er, Kelcy!

I can’t say I blame Kelcy and Bradford, who are no doubt excited about recent record earnings as well as the nearly $1.5 billion acquisition of Lotus Midstream, which adds roughly 3,000 miles of crude gathering and transportation pipelines that run through New Mexico, Texas and Oklahoma.

Distribution growth could remain modest in the near-term, as ET plans to spend more capex on expanding an NGL export terminal. But given the size of the yield and healthy cash flows to support it, that’s not much of a worry for income collectors.

Carlyle Secured Lending (CGBD)

Dividend Yield: 11.9%*

Recent Noteworthy Buys:

- CEO Aren LeeKong: 9,216 shares ($127,736) between 5/25/23-6/9/23

- CFO Thomas Hennigan: 3,900 shares ($52,221) on 5/18/23

This last business might not be sexy, but its roughly 12% payout sure is.

Carlyle Secured Lending (CGBD) is a BDC, which stands for “business development company” but might as well stand for “big dividend company.”

BDCs do what many banks won’t, providing financing to small and midsized businesses. They’re similar to real estate investment trusts (REITs) in that they were created by Congress to spur investment in a less-accessible sector. And similarly to REITs, they’re required to pay out at least 90% of earnings in the form of dividends to their shareholders.

And these aren’t just any dividends. These are some of the biggest dividends you can find. Even a plain-vanilla ETF holding these stocks will net you 11%!

The problem is, business development is a tough industry that seems to produce more losers than winners, which means a plain-vanilla ETF will hold more duds than studs. That’s why we have to be picky and look at individual names.

Carlyle Secured Lending is an externally managed BDC—and you’ll be unsurprised to find that its manager is a subsidiary of multinational asset manager Carlyle Group (CG). It invests primarily in U.S. middle market companies with between $25 million and $100 million in annual EBITDA. Its investments lean heavily toward first-lien debt (69%), though it also works through second-lien debt and equity, and it also holds investment funds. Its 133 portfolio companies cover a couple dozen industries, including healthcare/pharmaceuticals, software, aerospace/defense and leisure products/services.

CGBD doesn’t have much of a track record, going public less than a decade ago, in 2017. It spent its first few years middling, but it has risen from the COVID ashes more abruptly than its peers.

Carlyle Secured Lending’s Recovery Hasn’t Stagnated … Yet

Importantly, 99% of its debt investments are floating-rate in nature, so rising interest rates have been more of a help than a hindrance. Its performance has not only lifted shares—the payout has been growing, too, in multiple ways. CGBD pays a significant base dividend as well as a variable supplemental dividend, both of which have been trending higher over the past few years. The most recent payout of 44 cents is made up of a 37-cent base (10% yield) and a 7-cent supplemental (1.9% yield).

While Carlyle management is proving up to the task, I would worry about a combination of flattening interest rates and economic activity—the high core dividend seems safe, but shares and supplemental payouts could wane in a slowdown.

Eagle Bancorp (EGBN)

Dividend Yield: 7.6%

Recent Noteworthy Buys:

- Director Steven Freidkin: 10,000 shares ($175,000) on 5/16/23

- Director Kathy Raffa: 5,000 shares ($86,700) on 5/16/23

- President and CEO Susan Riel: 1,800 shares ($31,680) on 5/16/23

- Director Leslie Ludwig: 1,500 shares ($27,145) between 5/16/23-5/18/23

- Chief Legal Officer Paul Saltzman: 1,500 shares ($26,250) on 5/16/23

- CFO Charles Levingston: 1,124 shares ($19,928) on 5/17/23

Eagle Bancorp’s (EGBN) directors definitely understand the concept of “buy low.”

The question now is whether they’ll get their chance to sell high.

Eagle Bancorp is the holding company behind EagleBank, a regional bank serving the “DMV”—the District of Columbia, Maryland and Virginia—via 15 branches.

That branch count might be low, but the dividend is high: A wild yield of nearly 8%, on a payout that has roughly doubled (albeit in uneven fashion) in less than three years!

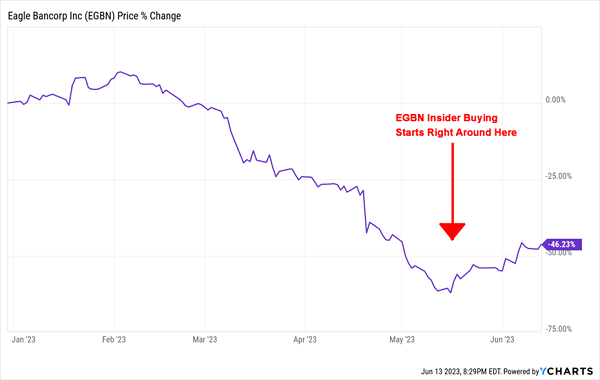

However, like with many regional banks, EGBN was flattened during the first half of 2023 amid the Silicon Valley Bank-inspired exodus from industry shares.

Make no mistake: EGBN’s selling was warranted. In April, the bank reported a 47% plunge in first-quarter net income as deposits plunged, to $7.4 billion from $9.6 billion the year prior.

But the bank is back on an upswing.

Did EGBN Management Time the Bottom?

Maybe investors were excited about EagleBank’s $45 million loan to refinance a “power center” retail property in Laurel, Maryland. But more likely they saw a gaggle of insiders turn bullish on a dime.

Six different corporate insiders bought stock in and around May 16. The biggest purchase was a $175,000 lot from Director Steven Freidkin—part of nearly $370,000 worth of buys from the board and other chiefs.

Their confidence is understandable. In May, regional banks were technically oversold at the same time it became clear that the sky was, in fact, not falling on the entire lot. EGBN’s disastrous quarter aside, the company’s credit remained stable—and the company even spent money to repurchase its own shares.

Give Me 4 Minutes, I’ll 4X Your Retirement Income

Of course, Eagle Bancorp’s board might feel some pangs of regret if a recession does bite in 2023’s second half—a risk you’d be taking with most regional banks.

And if you’re like most investors, the last thing your portfolio needs is another source of instability.

In just the past four years, you’ve been knocked around by not one, but two bear markets—including the longest bear run since 1948! And don’t get too excited about the new brewing bull—a second-half recession could stop it right in its tracks.

Fortunately, I don’t sweat these ups and downs anymore.

And you don’t have to, either.

My “Perfect Income” portfolio attacks retirement investing from a different angle. Rather than trying to time the market and chase trends, we target high-yield holdings (roughly 4x the S&P!) that walk their own path, no matter what the Fed, Congress or the rest of the world throws their way.

So, what makes these dividends “perfect”? Well, they have to have a few things in common:

- They DO pay consistently, predictably and reliably.

- They DO survive—and even thrive—in market crashes.

- They DO deliver double-digit returns, with safe, secure investments.

- They DO require minimal management time—just a few minutes every month!

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Let me show you the stocks and funds that can stabilize your dividend income. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!