Five growth companies are about to hike their dividends. Let’s front run these payout moves.

Many vanilla income investors miss these stocks because their current yields are modest. These armchair analysts are missing a critical point. These stock prices climb with each and every hike thanks to a phenomenon known as the “dividend magnet.”

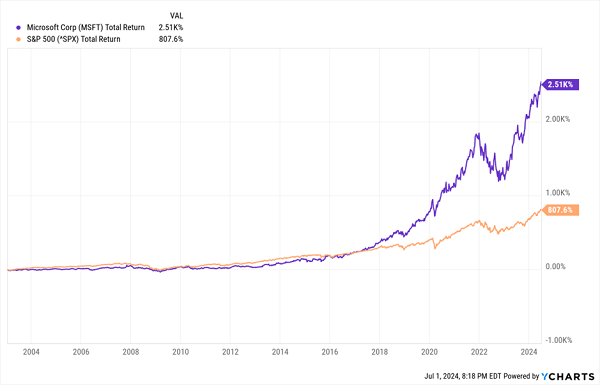

Consider tech giant Microsoft (MSFT). Sure, Microsoft’s 18-year-old payout isn’t exactly old compared to fellow Dow components like Coca-Cola (KO) and Procter & Gamble (PG), which have been writing dividend checks since the 1800s, but it’s awfully long in the tooth for a member of the technology sector.

Microsoft initiated its first dividend in 2003. The tech giant eventually became a big raiser. Shareholders enjoyed a doubler-plus in both the dividend and stock price.

The Dividend Magnet Kicks Into High Gear

And the full track record is pretty clear: Microsoft’s dividend wasn’t the end of the company’s growth—it was just the beginning.

Microsoft Has Tripled the S&P 500 Since Initiating Its Dividend

The attraction behind the dividend magnet is simple. Growing payouts gain shareholders for a number of reasons. Dividend investors love higher yields, and they love payouts that don’t lose ground to inflation.

And perhaps most importantly, dividends are actually a statement of confidence from corporate management—a signal that not only are profits strong, but that they’re sustainable and, in fact, likely to grow.

So the underlying financial strength that allows a company to continuously hike its dividends also helps push shares in the right direction.

That’s why I pay close attention to dividend announcements. On my radar right now are five stocks that have posted red-hot dividend growth of 20% to 100% in the past year—and that are due to announce new dividend actions over the next couple months, if the past is a precedent.

Marsh & McLennan (MMC)

Dividend Yield: 1.3%

2023 Increase(s): 20%

Projected Q3 Dividend Announcement: Mid-July

For more than 150 years, Marsh & McLennan (MMC) has offered a wide variety of professional services, including insurance broking, risk advice, strategic advisory services, analytics solutions, career advice, brand consulting, and much, much more.

The past decade has been something of a renaissance for insurance brokers, which have built up massive scale, and fatter margins as a result. Marsh & McLennan, for instance, recently celebrated its 16th consecutive year of margin expansion, to 26% in 2023 from 24.7% the year prior.

And MMC has been happy to share the wealth.

Marsh & McLennan hasn’t just been improving its dividends—it has been accelerating the rate of its hikes. Its dividend growth has averaged 11% over the past 10 years; 2023’s hike was nearly twice that, at 20%.

Marsh & McLennan’s next hike appears likely to come in mid-July.

Westlake (WLK)

Dividend Yield: 1.4%

2023 Increase(s): 40%

Projected Q3 Dividend Announcement: Mid-August

Westlake (WLK) is a global manufacturer of performance and essential materials (PEM), as well as housing and infrastructure products (HIP). The former business includes materials such as PVC, ethylene, polyethylene, styrene and more, while the latter involves a variety of PVC products, including sidings, mouldings, decking, pipes, and more, as well as other products including landscape edging and masonry joint controls.

Materials is an exceedingly cyclical business, and Westlake is no exception, but the arrow has broadly been pointed in the right direction. 2023 revenues of $12.5 billion are roughly triple those a decade ago.

Profits have been expectedly mercurial, too. The company suffered a big dip in earnings last year thanks in part from difficulty in performance and essential materials. But housing and infrastructure has been spiking—in fact, the division’s Q1 2024 EBITDA surpassed PEM for the first time.

But WLK reported record earnings in 2021 and 2022, which likely gave Westlake the ammo it needed to take its dividend to the next level in 2023.

Westlake Doles Out a Big Cash Reward

So, what can we expect in mid-August, when Westlake is likely to make its next dividend announcement?

It’s possible that the company might rein in its generosity following a 2023 that saw GAAP earnings drop by 78%. But Westlake still has plenty of room to make improvements, as the dividend accounts for just 22% of next year’s EPS estimates.

Comfort Systems USA (FIX)

Dividend Yield: 0.4%

2023 Increase(s): 61%

Projected Q3 Dividend Announcement: Late July

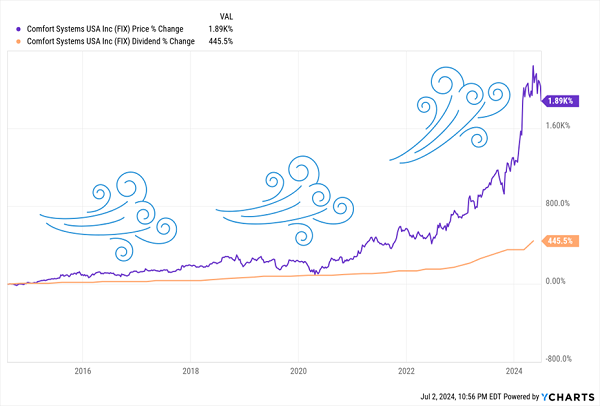

If you ever find yourself in a commercial building, it’s possible that Comfort Systems USA (FIX) has set up many of the systems that make the building usable and comfortable. Comfort Systems USA installs, renovates, maintains, repairs and replaces heating, ventilation, air conditioning, plumbing, electrical, monitoring, fire protection and other systems.

The company provides its services for buildings that serve a wide variety of sectors. Its two largest customer types are manufacturing and technology—and the latter is considered to be a significant driver of growth. One area of opportunity is artificial intelligence (AI); as technology companies continue to build the data centers necessary to power AI, they’ll need the types of HVAC and electrical solutions Comfort Systems provides and installs.

Comfort Systems’ ability to deliver for different industries has produced strong and steady growth. Revenues have grown every year for a decade, and up 370% in that time; profits haven’t been as consistent, but they’ve been up more often than not, and have exploded from $27.3 million in 2013 to $323.4 million last year.

That has driven an explosion in both FIX’s stock price and the company’s dividend.

FIX’s Dividend Jumps, And Shares Go Vertical

Comfort Systems has become more aggressive about dividend hikes as its fortunes have improved. It had been increasing two and even three times per year, but starting in 2023, it has hiked each and every quarter. Its July 2023 hike came out to a 12.5% improvement on the prior dividend, and 61% year-over-year growth.

That puts late July on our watch list for another potential hike … and given that FIX’s dividend accounts for less than 10% of earnings, Comfort Systems certainly has the room to make another splash.

Boise Cascade (BCC)

Dividend Yield: 7.6%

2023 Increase(s): 67%

Projected Q3 Dividend Announcement: Late July

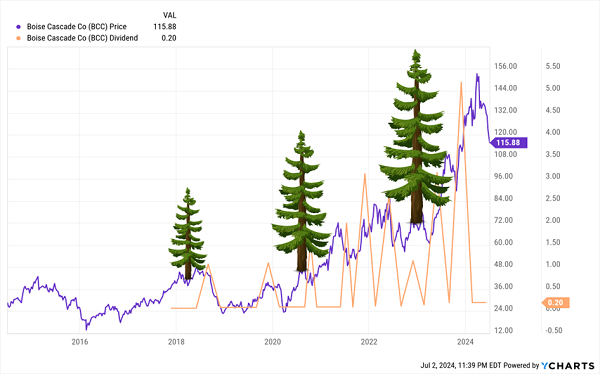

Boise Cascade (BCC) makes and distributes building materials in the U.S. and Canada. It operates in two segments: Wood Products, which includes laminated veneer lumber, laminated beams, I-joists, plywood panels, appearance-grade boards, and more; and Building Materials Distribution, which distributes strand boards, plywood, lumber, siding, decking, insulation, roofing, and more.

Boise has enjoyed largely persistent top-line growth for years, though predictably, its profits flip-flopped over time.

Until COVID, that is.

Skyrocketing lumber prices super-charged Boise Cascade, whose earnings jumped from around $81 million in 2019 to $175 million in 2020, to $713 million and $858 million in 2021 and 2022, respectively.

But as lumber prices have fallen off, so too have profits—by 44% last year, to be specific.

That makes Boise something of an enigma heading into its likely upcoming dividend announcement in late July.

What Happens as the COVID Boom Cools?

Boise raised its regular dividend twice between 2022 and 2023—by 25% to 15 cents per share in late 2022, then another 33% to 20 cents per share in July 2023, good for a 67% year-over-year improvement. And given a mere 7% dividend payout ratio, another big move could be in store.

But that’s practically a distraction compared to Boise’s special dividends. BCC regularly pays out specials—it delivered $8 per share of them, which comes to a 6.9% yield, which is the vast majority of Boise’s 7.6% listed yield. So while you’re likely to see a higher regular payout (if not in late July, at some point in the future), it’s possible that the specials will recede as profits have.

Voya Financial (VOYA)

Dividend Yield: 2.2%

2023 Increase(s): 100%

Projected Q3 Dividend Announcement: Late July

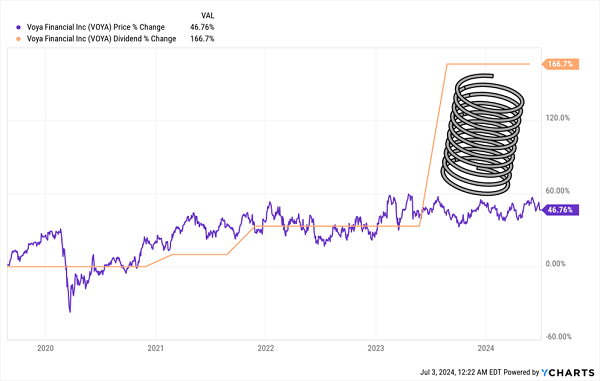

Voya Financial (VOYA), which was spun off ING Groep (ING) in 2013, is a financial company that specializes in workplace benefits and savings. Many of its offerings should sound pretty familiar—it provides retirement products, non-qualified plan administration services, wealth management services, group disability insurance, whole life insurance, health account solutions, benefits administration, and much, much more.

This is a difficult-to-read business that’s affected by investment success, employment, underwriting results and a variety of other factors. Indeed, Voya sports the most volatile financials of all the stocks here—the company’s revenues peaked in 2014 but jumped 75% between 2021 and 2023. Voya has posted red ink in four of the past 10 years, and last year’s profits were a quarter of what they were in 2021.

No wonder, then, that shares have largely been flat over the past few years. But perhaps the dividend magnet is about to go to work.

Is Voya Ready to Launch?

Immediately? Possibly not. The stock has no clear catalysts on the horizon, and shares are fairly valued.

And the dividend? It’s difficult to tell exactly when Voya will raise because it’s not consistent. Voya announced hikes in January and October 2021, nothing in 2022, then its dividend doubler in late July 2023. So if Voya were to get on a consistent dividend-raising schedule, late July 2024 would be the time.

But given its spotty history, we might get nothing.

A Simple, Safe Way to Lock In 15% Yearly Returns … For Life!

The dividend growers above aren’t exactly perfect, but they’re still excellent examples of the right strategy—a simple but potent two-step recipe for success that has proven itself to investors again, and again, and again:

- Step 1: Buy aggressive dividend growers that are actually expanding their businesses, too.

- Step 2: That’s it! There is no Step 2! Just keep targeting elite dividend growers!

If you invest your money with corporate managers who both effectively deploy capital for growth and know how to reward shareholders, you will clobber the market on a regular basis—and better still, as the years roll on, more and more of those returns will come from cold, hard cash.

You can put this income-printing strategy to work today with a simple-to-manage, easy-to-understand group of just 5 specific tickers that are quietly handing investors a steady 15%, 17%, 21% or more every year—and growing income streams!

Better still, they’re trading at far more attractive prices—a value proposition that will further boost our price returns over time.

Your next move is simple: Buy now and you could set yourself up for annual returns of at least 15%. That’s far better than the market’s historical average, and it’s a level of return that would double your nest egg every five years!

You can get the full breakdown on each of these standout names within seconds. Click here for the full story — and how to get the names, tickers and a full breakdown of their operations—everything you need to buy with confidence.