If there’s one thing we need to remember when we buy high-yield closed-end funds (CEFs), it’s this: always demand a discount.

Well, make that two: always demand a high dividend! Because CEFs are renowned for their high—and often monthly—payouts, with the average CEF yielding around 8% today.

But back to discounts. Luckily for us, they’re common in the CEF world: of the 433 CEFs tracked by the CEF Connect screener, some 390 trade at discounts to net asset value (NAV).

These discounts are basically free money because they let us pick up, say, Mastercard (MA) for 83 cents on the dollar through a CEF like the Gabelli Dividend & Income Trust (GDV). This fund, run by value-investing guru Mario Gabelli, has MA as its top holding and trades at a 17% discount as I write this.

Another bonus of buying through a CEF is, of course, the aforementioned dividend. MA shares yield just 0.6%. But if you buy through GDV, you’ll get a 6.7% dividend instead—and GDV makes that payout monthly instead of quarterly, like MA.

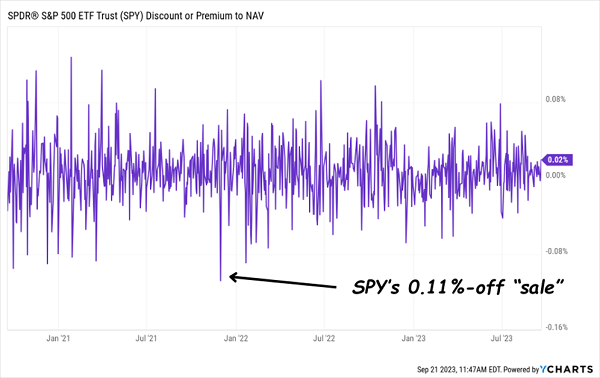

Discounts to NAV only exist with CEFs. Mutual funds and ETFs issue shares whenever they want, fixed each day at NAV. This is why the popular SPDR S&P 500 ETF Trust (SPY) is never cheap:

SPY’s Biggest Discount Is … 0.11%!?

When It Comes to CEF Discounts, Context Is Everything

Unlike mutual funds and ETFs, CEFs have fixed share counts, with their funds trading like stocks. As a result, their shares and per-share NAVs often trade at different levels—and usually at a discount.

But there’s one more piece to the story here, as simply buying a CEF with a deep discount and calling it a day is a recipe of ho-hum (at best!) returns. That’s because, just like some stocks are always cheap (or are cheap for a reason) some CEFs’ discounts never change.

So we need to dig deeper and make sure management has a plan to close the CEF “discount window.”

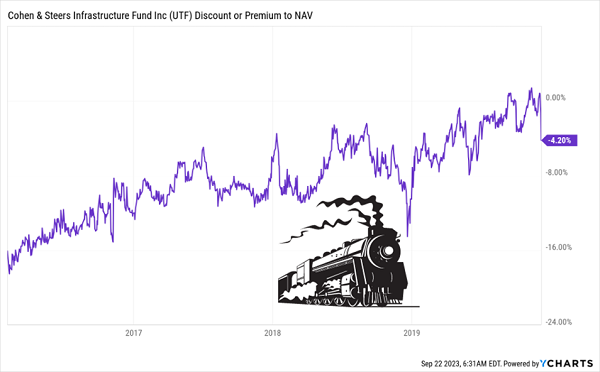

That includes not only looking at the current discount to NAV, but also the current discount in relation to its history. To see what I’m getting at here, consider the Cohen & Steers Infrastructure Fund (UTF), a fund that’s done a couple of tours of duty in my Contrarian Income Report high-yield investing service.

These days, as it did then, UTF holds a mix of electric utilities (currently 33% of the portfolio), pipelines (around 11% now) and infrastructure plays, such as toll roads (7.5%). Its current top holding is NextEra Energy (NEE), a renewable-energy leader that’s rarely cheap. But thanks to UTF, we have a shot at buying it at a rare “double discount” today—more on that in a bit.

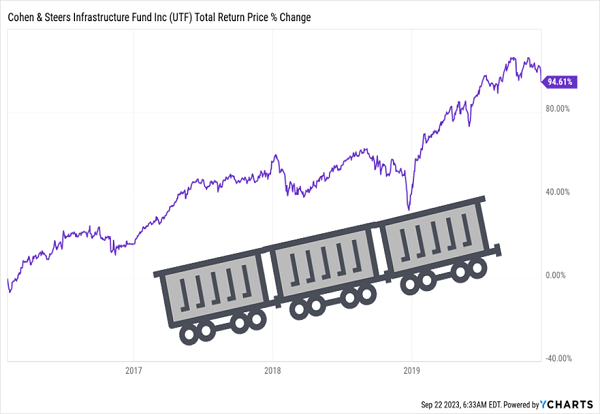

UTF’s first stint in CIR started back in February 2016, when it yielded around 8.8%, and ran to December 2019. As with all of our CEF buys, our play here was all about the closing discount. In that time—a bit less than four years—UTF’s discount collapsed from an unusually wide 16% when we bought to around 4% when we sold.

UTF’s Discount “Freight Train” Leaves the Station …

That drove the price higher in lockstep, to the tune of about 38%. And when you include UTF’s (monthly paid) dividend, which yielded 8.8% then and pays just a hair more—9%—today, you get a 94.6% total return in just under four years.

… Pulling Its Return to a Near-Double

That, by the way, highlights another danger of CEFs—judging them by price returns alone. That’s an easy mistake to make because popular screeners like Yahoo Finance and Google Finance only show price returns. But because CEFs give us so much of our income as dividends, we have to look at total-return charts to properly judge their performance.

But (once again!) I’m getting off track here. I mention UTF now because it’s a CIR holding once more, and its current discount, at around 7%, is once again below the long-term trend—its five-year average is right around par. Sure, that’s not the 16%-off deal we had in front of us back in ’16, but the disappearance of the discount alone would drive a 6% price increase.

There’s more: utilities are essentially bond proxies, so their prices have fallen as rates have shot up. But as the economy slows, rates will move lower. And while we wait for price upside, we’ll happily collect UTF’s monthly paid 9% dividend. That’s the second part of our “double discount” here.

And here’s something else few folks realize about CEF discounts: they can help secure a fund’s dividend. In the case of UTF, its yield based on its discounted market price is 9%, while the yield based on its per-share NAV is 8.4%. That second number is important because it’s what the fund needs to earn to cover the payout. To be sure, that’s not a massive difference, but it does give the payout a bit of extra cushion.

Finally, with rates topping out and likely headed lower, UTF will face less “dividend competition” from the likes of Treasuries. That, too, should help it catch income investors’ attention—and further narrow its discount.

Note From the Publisher

Kevin Wallen here, I’m the publisher here at Contrarian Outlook.

I’m writing to tell you that Michael Foster, our guru on CEFs—particularly smaller CEFs—has uncovered 5 monthly dividend funds with huge cash payouts.

They’re all top trades now that Jay Powell & Co. have tapped the brakes on interest rates.

- They throw off a 9.2% average yield.

- They pay dividends every month.

- They trade at big discounts that are set to evaporate as the Fed moves toward lowering rates in ’24.

This opportunity has been evolving quickly since last week’s Fed meeting, so we don’t have a lot of time. Click here to get the backstory on these 5 MONTHLY income plays and the opportunity to download a free Special Report revealing their names and tickers.