Let’s kick off 2024 with great news: despite the Santa Claus rally, there are still some sweet dividend deals on the board—many hiding in plain sight.

In a second, we’ll name names and dive into my 2024 outlook, including my forecast for a 2024 recession and exactly what we’re going to be looking for in dividend payers (and growers) this year.

First, let’s tee up 2024 by reviewing the game tape from the last quarter of ’23.

Buying Fear Drove Fast Double-Digit Gains in Late ’23

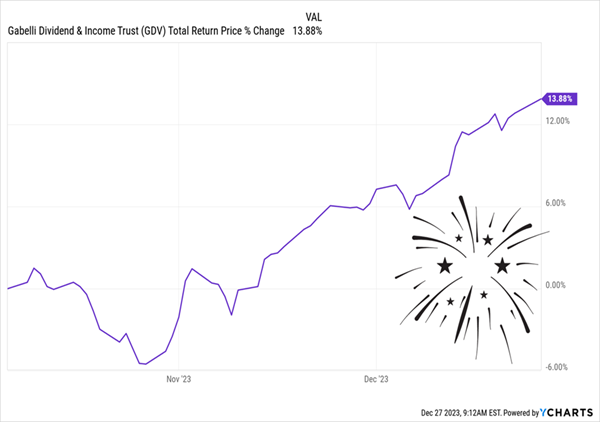

Readers of my Contrarian Income Report service will recognize the Gabelli Dividend & Income Trust (GDV), one of the picks we grabbed when panic was running high in October.

I bring up GDV because the fund—a closed-end fund (CEF) run by legendary value investor Mario Gabelli—holds blue chips you can set your watch to, like Mastercard (MA), JPMorgan Chase & Co. (JPM) and Microsoft (MSFT).

When we snagged it on October 6, it yielded a sweet 6.9%. Just under three months later, we’re sitting on a 14% total return (including three dividend payouts, as GDV pays monthly). This is why we always buy our blue chips through CEFs, not ETFs.

GDV Soars Into the New Year (While Dishing Us 3 Monthly Payouts)

Where does that leave us?

To be sure, there’s still plenty of optimism out there, and that’s taken some dividend deals off the table (with a few of our Contrarian Income Report holdings—including GDV—flipping from “buys” to “holds in recent days). But as I said, there are still some deals to be had, as well.

The “Recession-Resistant” Payers We’ll Aim for in ’24

At the top of our list? Stocks with growing dividends, which tend to pull their share prices higher over time, despite recessions, inflation, geopolitical messes or whatever. We also want companies with an edge that bolsters them in a recession, which I expect later this year.

Those “recession-resistant” strengths include strengths like reliable revenues from, say, rent payments or customers who must buy their services no matter what. Our first stock is a good example.

2024 “Dividend Deal” #1: The “Energizer Bunny” of Payout Growth

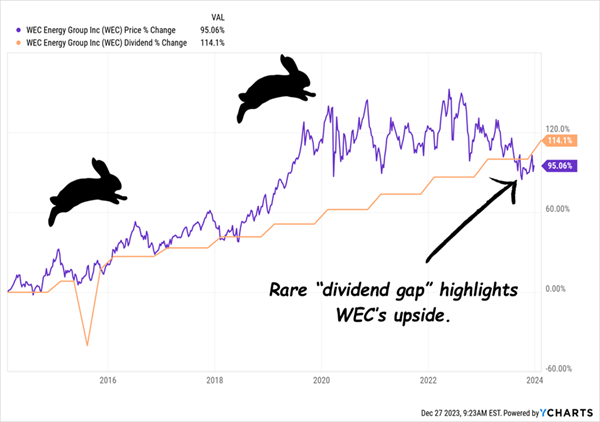

WEC Energy Group (WEC), which we last wrote about on September 6 here on Contrarian Outlook, sports a fast-growing dividend that continues to hold our attention. On December 20, management said it plans to declare a 7% payout hike in January—the new rate will be payable on March 1 to shareholders of record on February 14.

The increase will mark WEC’s 21st straight year of hikes, putting it on track to move into the vaunted “Dividend Aristocrats” club in 2028.

WEC, is a Midwestern utility with 4.6 million power and gas customers in Wisconsin, Illinois, Michigan and Minnesota. It’s also making big moves in renewable power, with nearly 3,500 megawatts’ worth in the pipeline.

The 2024 hike will add to a payout that does nothing but grow, having more than doubled in the past decade:

WEC’s Price Springs Higher With Its Payout

(Don’t worry about that dip in 2015—the payout was pro-rated due to WEC’s acquisition of Integrys Energy; it wasn’t cut!)

WEC’s Dividend Magnet doesn’t only have a pull on the share price—it has a pull on us, too, for a couple of reasons:

- It shakes off whatever the economy is doing: Global pandemic? Inflation? High rates? Low rates? Take another look at the chart above: WEC’s payout stair-steps higher no matter what.

- Its price is “gapping” its dividend: You can see that WEC’s share price (in purple above) hardly ever falls behind its payout growth (in orange). And when it does, it stays there for a very short time. That makes today’s gap unusual—and worth looking at before the purple line jumps over the orange one again.

Here’s a third reason why WEC has our attention: it’s yielding 3.73% as I write this, just below the 3.98% it hit in October 2023, which itself was a high not seen since 2000.

That gives us a high “base” to start from on a buy made today, as WEC continues growing its payout. The yield on a buy made today, at WEC’s historically high yield, would result in a roughly 8.6% yield on that purchase in 2034.

We have every reason to believe that will happen, as the payout is well-supported. In the company’s latest dividend announcement, executive chairman Gale Klappa said the new payout lines up with WEC’s plan to pay out 65% to 70% of earnings as dividends—safe for a company with steady revenue like WEC.

2024 “Dividend Deal” #2: A 453% Payout Grower That’s a “Stealth” AI Play

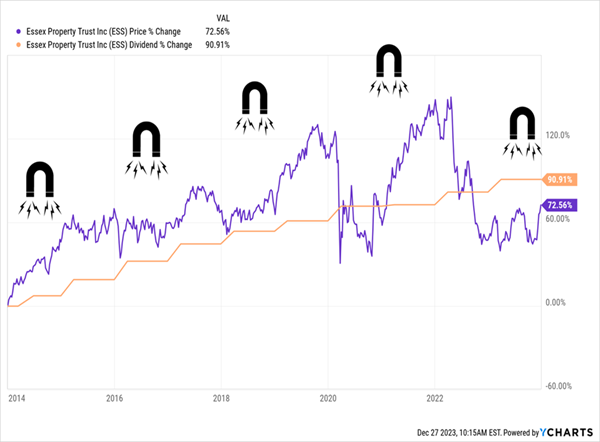

Essex Property Trust (ESS) is another stock we last brought to your attention on Contrarian Outlook in September—the 19th, to be precise. And like WEC, it’s back on our radar again, this time because it’s doing what we said it would: handing out some spectacular growth, with its price jumping some 16% since.

That’s started to close the gap between the firm’s share price and dividend growth:

As Predicted, Essex’s “Dividend Magnet” Is Doing Its Thing

But not to worry—there’s still room to get in on the 3.7%-paying REIT, which owns more than 62,000 apartment units in California and Washington State. It’s an indirect play on two megatrends sweeping its tech-powered markets:

- Surging AI investment, driving a jump in venture-capital funding in the Bay Area.

- The (partial) return to the office, as more firms, like Salesforce (CRM), Apple (AAPL), Meta (META), Amazon.com (AMZN) and Alphabet (GOOGL), now require staff to be in the office at least three days a week.

In effect, Essex is a savvy way for us to use real estate—and the income it provides—to tap into IT trends like AI, network security and EVs—Essex has a presence in Fremont, home to a Tesla (TSLA) factory.

Not to mention tech trends you rarely hear about. Remember cloud computing? It’s still out there, and surging: according to research firm Mordor Intelligence, it’ll post a compounded annualized growth rate of 16.4% from 2023 to 2028.

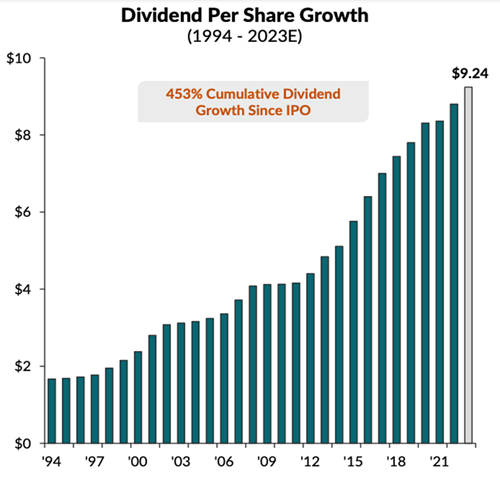

Those forces are supporting Essex’s cash flow—and dividend. History is also on our side with the payout, which has grown yearly for 29 straight years, putting Essex where WEC is headed: among the Dividend Aristocrats.

Source: Essex Property Trust November 2023 investor presentation

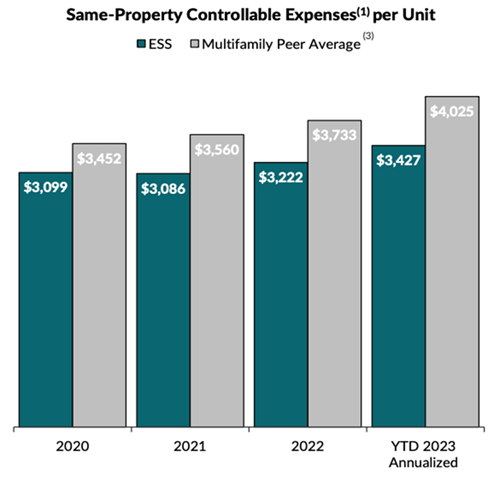

Another thing we like about Essex is management’s iron grip on costs. To be sure, operating expenses have risen for Essex (and everyone else!) these past couple years. But Essex consistently tops its peers in cost-control, and its lead has been growing:

Source: Essex Property Trust November 2023 investor presentation

Finally, the dividend is safe, with management boosting the midpoint of forecast 2023 core FFO to $15.00; the annualized quarterly payout accounts for a comfortable (for a REIT) 61% of that.

Buy This 2024 Pick Now—and “Lock In” a 14% Gain—in Cash!

Essex and WEC are terrific stocks to own—but with a chance of a recession later this year, it’s a good time to get more of our dividend income upfront, with current yields that dwarf the 3% to 4% these stocks pay.

Enter another stock (closed-end fund, to be precise), that I’m pounding the table on as we move into 2024. This underappreciated bond fund gives us the best of all worlds, with a 14% current yield, a monthly dividend, dividend growth and a history of special dividends!

A “Once-in-a-Generation” 14% Dividend Opportunity

Source: CEF Connect

What’s more, that immense payout is delivered by a manager whom Morningstar previously named Fixed Income Manager of the Year. He has also been inducted into the Fixed Income Analysts Society Hall of Fame.

To say he knows his field is an understatement—and now we can get him working for us, just in time to help us navigate the shifting winds we’ll no doubt encounter in the year ahead.

Don’t miss this opportunity, which I’m urging investors to buy now, just in time for 2024. Click here to learn more about this 14%-yielding income play and get a free Special Report revealing my latest research on it.