Over the last few days, not one but three signals I use to read the tea leaves in REITs—one of our favorite places to hunt for big, and growing, payouts—all flashed “buy.”

That means it’s finally time to start selectively picking up these income plays. I’ll name two with dividends on multi-year growth runs below. Tickers in a sec. First, let’s talk timing. Here’s why REITs are jumping up our dividend priority list now:

- They haven’t followed stocks higher in ’23—so our “landlords,” which own everything from shopping malls to warehouses, apartment buildings and cellphone towers, are cheap in relation to the popular kids of the S&P 500. So …

- Their yields are (still) historically high, at around 4.6%, the average REIT pays more than triple the 1.5% the typical S&P 500 stock dribbles out, plus …

- We’re rolling into “stock season,” with October, November and December typically being three of the best months for stocks, and September being one of the worst. With stocks in the red so far this month, September is playing its usual “spoiler” role—and keeping our buy window open.

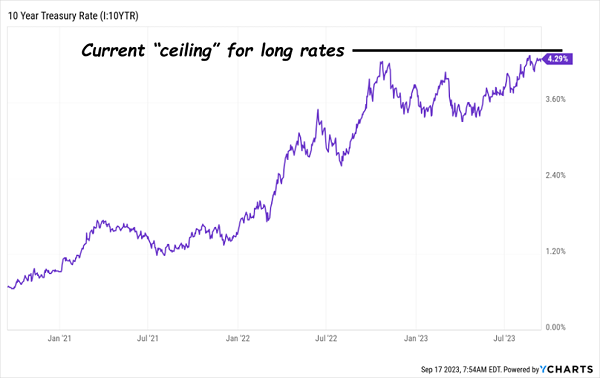

We’re also getting a green light to buy REITs from an unexpected place: rising Treasury yields. As I write this, the 10-year Treasury yield is bumping its head on the 4.3% ceiling that it’s bounced off of repeatedly in the last year.

Each time has been a great opportunity to buy bonds because bond prices rise as yields fall. Well, select REITs should do even better. Over the short run, REITs trade like bonds. They decline when rates rise—and rise when rates decline.

But a good REIT beats a great bond. REITs are actual businesses that can grow cash flows simply by raising their rents. Which means, not only are their prices low today, but they have more room for gains than a bond fund.

By the way, we shouldn’t go further without tipping our caps to Uncle Sam, whom we can thank for REITs’ high yields: the government gives REITs a hall pass on corporate taxes so long as they pay 90% of their income as dividends. The resulting savings—and the fact that this hoard must be passed to us—drive those big dividends, and often fast dividend growth, too.

So if you like a fat yield and a dividend that soars every year (and sometimes quarterly), REIT-land is the place for you.

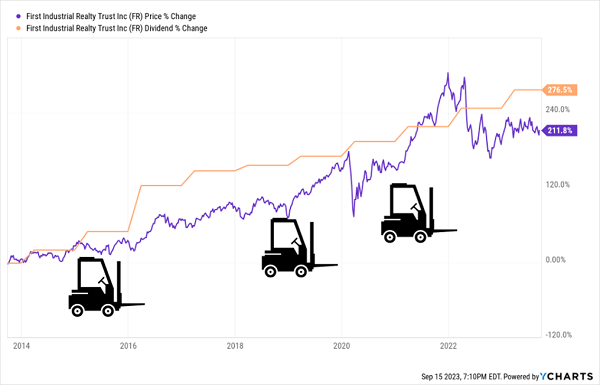

And there’s more working in our favor here, too. I know we’ve talked about the “Dividend Magnet” again and again. But there’s a good reason: a rising dividend is the No. 1 driver of share prices. Take a look at this price and dividend action on warehouse REIT First Industrial Realty Trust (FR).

Heck, maybe in the case of FR we should call it a “Dividend forklift!”

First Industrial Realty Trust: Dividend “Lifts” the Share Price Higher

That’s the payout and price action on First Industrial Realty Trust (FR) in the last 10 years. FR owns 444 industrial properties across the US, with a focus on the coasts.

As you can see in the chart above, FR’s dividend went a bit flat in the mid-teens. But it’s been sprightlier lately, pulling up the price. As you can also see above, the stock now lags the dividend—and it tends to “catch up” over time.

These days, FR’s catching a tailwind from “onshoring,” or US and multinational companies shifting their operations to the US and away from basket cases like China.

Every month, it seems, we’re reading about a new factory opening in America, and all that hammering, welding and assembling happening here has cranked up demand at FR’s warehouses: in the second quarter, occupancy was 97.7%. The company also renewed or initiated 43 new leases in the quarter at an average rent increase of an eye-popping 74%.

So it’s no wonder management boosted guidance to $2.35 to $2.43 in funds from operations (FFO, the key profitability metric for REITs like FR) for all of 2023. The dividend occupies just 53% of the midpoint of that range, so it’s plenty safe.

With onshoring still surging, warehouses in the right spots to capitalize, FFO rising and long rates looking toppy, FR’s shares—and payout—could catch a lift from here.

A 4.1%-Paying Residential REIT With a Tech Edge

Now let’s flip to the residential side, specifically to Essex Property Trust (ESS), owner of more than 62,000 apartment units in California and Washington State. It’s an indirect play on three trends sweeping its tech-powered markets:

- Surging AI investment, driving a rebound in venture-capital funding in the Bay Area, following a tough (to put it mildly!) 2022.

- Ongoing high mortgage rates, which are pushing more buyers out of the market—and into Essex’s rentals, supporting the REIT’s 96.6% occupancy rate.

- The (partial) return to the office, as more firms, like Salesforce (CRM), Apple (AAPL), Meta (META), Amazon.com (AMZN) and Alphabet (GOOGL), now require staff to be in the office at least three days a week.

Those forces are driving Essex’s FFO—and dividend—higher. History is also on our side with this 4.1%-payer, which has been hiking its payout annually for 29 straight years.

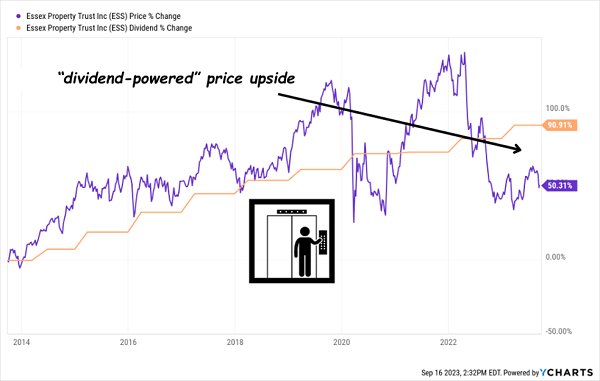

Over the last decade, we’ve seen Essex’s share price steadily track its payout higher, up till the washout of 2022, from which Essex—and REITs generally—have yet to recover. That’s our upside with this West Coast apartment maven:

Payout Takes the Elevator—Share Price Takes the Stairs

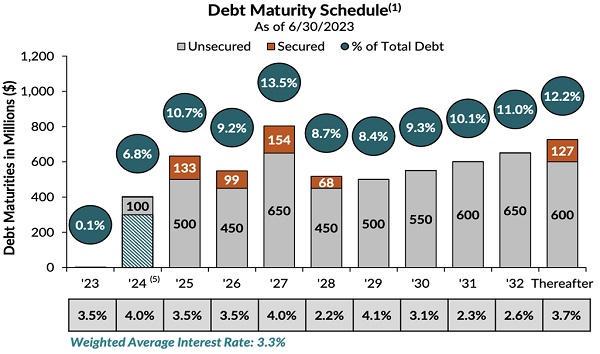

There’s more here, too—because the next time someone tells you that REITs are carrying too much debt in today’s high-rate world, show them the image below. It’s a snapshot of Essex’s team putting on a debt-management masterclass:

Source: Essex Property Trust Q2 Investor Presentation

That’s right—Essex is paying a weighted average interest rate of just 3.3%! If you’ve ever wondered if big companies are getting a better debt deal than you and me, well, there it is. And with just under 7% of its debt maturing by the end of 2024, when rates are expected to be on the downslope, Essex is in a nice spot indeed.

The kicker: the REIT saw same-property revenues rise 4% in Q2, far more than its interest payments. Meantime, operating expenses actually fell—it’s been a while since we’ve seen that!—to the tune of 1.2%.

Finally, the dividend is safe, with management boosting the midpoint of forecast 2023 core FFO to $15.00, and the annualized quarterly payout accounting for a comfortable (for a REIT) 61% of that.

Special Report: 5 Dividends “Spring-Loaded for 15% Yearly Gains

I’ve zeroed in on 5 MORE fast-growing dividends set to “lift” their prices higher year after year—no matter what happens with stocks or rates.

There’s nothing mysterious about these 5 stocks. They simply generate strong cash flows that are “recession-resistant.” One, for example, is a REIT that owns cell-towers—a goldmine in any economy because, let’s be honest, Americans will never give those up, recession or no!

I’ve put my research on these 5 names in a freshly updated Special Report, and I want to give you a copy now. Click here and I’ll tell you more about these 5 “recession-resistant” 15% growers and give you the opportunity to download your free copy.