Drill baby, drill is driving vanilla energy investors nuts. Drilling permits spike one month and plunge the next. Crude oil itself is sitting in the $60s, too low for producers to make real money.

Our contrarian solution? Focus on the energy toll collectors—particularly a dividend duo dishing up to 8.1%.

Pipeline owners are paid every time oil and gas flow through their pipes. The latest headlines about GDP, drilling permits or (heck) the Federal Reserve don’t matter here, because there are plenty of hydrocarbons that need to move.

Big picture, US oil output has doubled since 2008. Back then, we were pumping about 5 million barrels per day. Today it’s a ballooning 13.4 million—a record. America is now one of the world’s largest exporters of oil.

Even though Texas drilling permits dropped from 772 two summers ago to 606 recently—a four-year low—actual production remains robust thanks to efficiency. Producers are pumping more oil out of each well.

For pipeline operators, that’s perfect. Oil and gas flows fuel their cash flows. It’s about volumes, not margins—and volumes remain near record highs.

Natural gas tells the same story. Appalachia’s Marcellus and Utica shales have turned into one of the world’s largest gas fields. That’s where Antero Midstream (AM) earns its keep.

AM owns and operates the pipelines that gather and move parent company Antero Resources’ natural gas. AM’s toll bridge simply collects cash from each cubic foot of gas that flows. No drilling risk!

AM has paid a generous dividend every quarter since its 2014 IPO and shows no sign of stopping. Cash flows safely cover the dividend, with about 30% to spare—plenty for a pipeline and promising for future raises.

And there’s more cash coming. Management has successfully deleveraged its balance sheet in recent years, trimming from over 4X EBITDA a few years ago to 3.3X today. The ultimate target is sub-3X.

AM buys back shares, which reduces its dividend obligation (freeing up cash for more dividend hikes) and supports per-share profit growth. And as AM nears its debt target, we expect more buybacks and eventually a dividend raise. Shares yield 5.1% today.

For those who prefer a wider net, we have Alerian MLP ETF (AMLP). It yields 8.1% and wraps the biggest U.S. midstreams—Enterprise Products Partners (EPD), Western Midstream Partners (WES), Plains All American Pipeline (PAA)—into one simple fund. Yes, no K-1 tax forms, just a clean 1099. EPD alone has raised payouts 25 consecutive years, and that consistency flows through to AMLP’s distribution. A $100K stake in AMLP throws off $8,100 annually in cash — pure toll income, insulated from drilling or oil-price swings.

The beauty of this model? Pipelines don’t depend on whether oil is $60 or $90, or gas is $2.50 or $4. Energy movement, not margins, pay them.

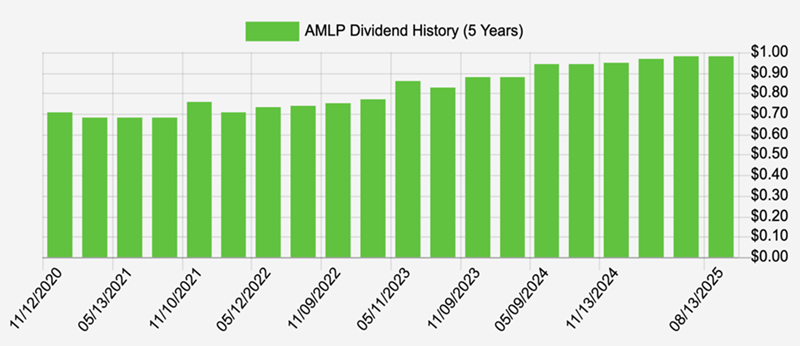

Many of AMLP’s holdings consistently boost dividends. This flows through to AMLP’s quarterly distribution:

AMLP’s Rising Dividend

Source: Income Calendar

In an uncertain world, we’ll take the reliability of these energy toll collectors. They face limited direct competition because building new pipelines requires massive cash outlays plus successful navigation of permitting and land-use restrictions. So, existing operators find themselves in an enviable position—with robust cash flows supported by steady, long-term contracts with their producers. Sign us up.

AMLP is the type of investment that helps investors retire on just $500K. Its elite 8.1% dividend turns a cash pile into an ongoing source of passive salary.

For example, $100K invested in AMLP gushes $8,100 per year in passive income alone. Plus, there is upside potential: raising its dividend boosts both yield and price!

This is the proven retirement strategy for 2025 and beyond—an income stream 100% funded by dividends that can turn $500K into a stable income stream that lasts for decades.