Look, we’re probably going to see a recession in 2023. And if you’re like most folks, you’re wondering how to respond.

Here’s the good news: overall I see a much better year ahead than the mess we lived through in 2022. But we could see a pullback—and a recession—before the market bottoms and bounces.

That leaves us contrarian dividend seekers in a tricky spot. It’s why we’ve held a lot of cash in my Contrarian Income Report service over the last 12 months.

But I also hear from a lot of folks who want stocks they can hold no matter what, to keep their payouts rolling in.

I get it. I feel the same way myself. Unfortunately, there’s no such thing as a stock that pays a high dividend and never falls. (If there were, your income specialist would be out of a job!)

Our 3-Part “Recession-Resistant” Dividend Strategy

But there are things we can do to secure our income streams in a pullback—and even use a market decline to our advantage—while holding for the long haul.

For one, we can use dollar-cost averaging (DCA) to move into our dividend payers. By investing a fixed amount on a fixed schedule, we’re naturally “timing” the market, buying more when stocks are cheap (as in a recession) and fewer when they’re pricey.

And we can focus our DCA plan on stocks with what I like to call “recession-resistant” dividends. In addition to high—and ideally growing—payouts, these companies have:

- Strong cash flows.

- Reasonable payout ratios (or the percentage of free cash flow occupied by the dividend—more on this below).

- Megatrend-backed businesses.

Now let’s move on to two sectors—and two stocks—that meet these benchmarks.

Energy Stocks: Long-Term Future Is Hot

To be sure, energy would take a hit in a recession. But over the longer term (I’m talking months to years here), I like its outlook. The crash ’n’ rally pattern I’ve written about before on Contrarian Outlook is alive and well. Here’s how it played out from 2008 to 2012—and how it’s repeating today:

- First, demand for oil evaporates due to a recession. The price of oil crashes (2008 and 2020).

- Next, energy producers scramble to cut costs. They cut production aggressively (2008 and 2020).

- Then, the economy slowly recovers. Energy demand picks up (2009 to 2012, 2020 to today).

- But there’s not enough supply! So, the price of oil climbs and climbs and climbs (2009 to 2012, 2020 to today).

- Energy producers bring supply back online, but it takes time to explore and drill. Supply lags demand for years, and the price of oil climbs and climbs (2009 to 2012, 2020 to today).

“Sure, Brett,” you’re probably thinking. “But haven’t oil prices been stuck in a rut for months now?”

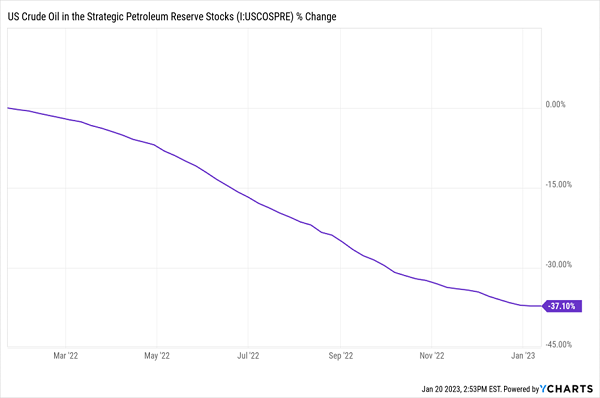

Yes! But remember that oil is being artificially held down by the Biden Administration’s drawdowns from the Strategic Petroleum Reserve. Eventually those drawdowns will have to be replaced, driving up oil prices (and demand!).

The SPR: Down 37% in the Last 12 Months

At the same time, China’s reopening from its over-the-top COVID controls will also spur demand—and prices.

Even so, as mentioned, energy stocks will fall in a recession, so you’ll want to either wait for my buy signal in Contrarian Income Report or look to a DCA approach for the long haul.

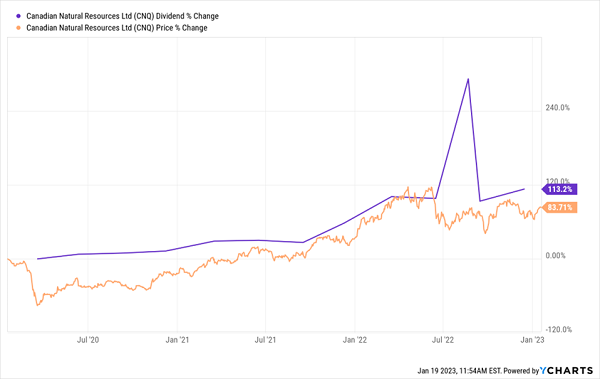

One dividend to put on your list? Canadian Natural Resources (CNQ), which yields 4.2% and is sitting on Canada’s largest natural gas reserves, a portfolio of heavy and light-oil properties in Canada, and deepwater operations in the North Sea and off the coast of Africa.

CNQ generates cash faster than it can dish it out to investors—in the third quarter, operating cash flow jumped 42%, to $6.1 billion (all amounts in Canadian dollars). The company’s soaring free cash flow prompted management to announce a $1.50-per-share special dividend in August and a generous 13% hike to the regular payout in November.

In all, the regular dividend has more than doubled in just the last three years, pulling the share price higher with it (you can see that hefty hike and the special dividend on the right-hand side of the chart below):

CNQ’s “Dividend Magnet” Fires Up

The stock’s bargain P/E adds further upside: CNQ trades at 7-times trailing-12-month earnings. It’s tough to find a single-digit P/E anywhere these days, let alone on a cash-flow machine like this. But here it is.

Finally, CNQ’s ultra-safe payout ratio of 33% of trailing-12-month free cash flow adds another layer of safety to its already-ironclad payout.

This Self-Storage REIT Is Built for a Pullback

Self-storage is about as simple a business as you can get: the owner throws up a building, hands out the keys, collects the rent and keeps the shelves dusted. It’s also a business that holds up well in a recession because it’s during pullbacks that people downsize—and need a place to store their stuff.

Trouble is, barriers to entry are also low—and that’s led the sector to overbuild in the past. So when we’re shopping the space, we need to make sure we buy a REIT with enough market share to keep its competitors at bay.

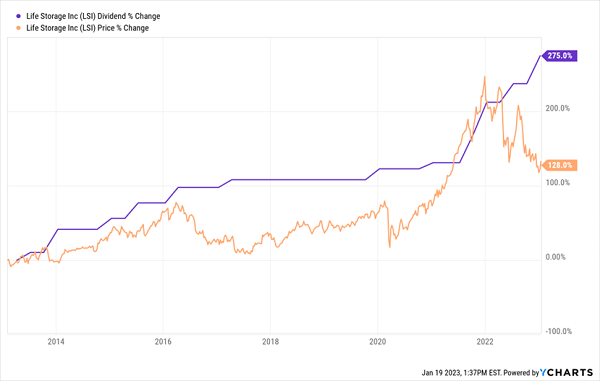

That’s what we get with Life Storage (LSI), payer of a 4.3% dividend. LSI has 1,100 storage facilities across 37 states, with a focus on Florida and Texas.

The company’s funds from operations (FFO) continue to grow, up 26% in the latest quarter, fueled by its expansion (it’s acquired about 232 outlets since 2018) and higher rental rates—it boosted same-store average rate growth per square foot by 17% in the third quarter, a sign of its ability to pass costs on to tenants.

That prompted management to announce a generous 11% dividend hike on January 3. In all, the company’s payout has soared 275% in the last decade. And as you can see below, the share price has mostly kept pace—until recently, when the 2022 selloff held the stock back. As share prices almost always track dividends, we can view that gap as our upside:

LSI’s Dividend-Powered Gains—Mind the Gap

The dividend growth should continue, as the REIT is forecasting about $6.44 in funds from operations (FFO—the best metric of REIT performance) per share for all of 2022. The newly raised dividend amounts to 74% of that on an annualized basis—very safe for a REIT with recurring revenue like LSI. The reasonable valuation of 15.5 times that forecast seals its place as a “recession-resistant” payout.

This Secret Income Portfolio Crushes Stocks—and Could 4X Your Income

The only trouble with the two stocks above? Their yields aren’t quite high enough to get our pulses racing! If we want to truly fund a safe retirement in the chaotic world we’re now living in, we need to do better.

We need SAFE yields of 7%, 8% or higher, so we’re relying more on dividends to pay the bills and less on erratic price gains!

My Perfect Income Portfolio delivers that. I’ve built it specifically to:

- Pay you consistently, predictably and reliably.

- Give you my top picks in undervalued, overlooked investments, which research shows have a far better chance of soaring than the overvalued, popular names that most folks buy.

- Take just a few minutes every month to “manage.”

- NOT involve day trading, buying on margin or any other risky strategy.

And most importantly…

Could 4x your current investment income if you’re stuck “grinding it out” with the typical S&P 500 stock!

I’m ready to share the details on this unique collection of investments—with yields of 7%, 8% and 9%+—with you now. Click here and I’ll give you the full story on this “perfect” portfolio and access to a Special Report naming the high-yield stocks that make it work.