2 “Guard Dog” Monthly Dividends That Fight Off a Crisis

Brett Owens, Chief Investment StrategistUpdated: May 26, 2020

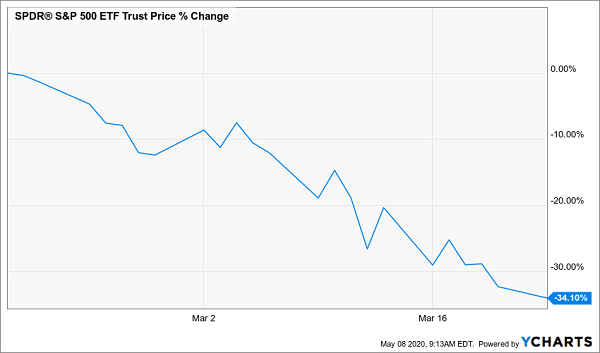

Right now, millions of people are plowing cash into this market, gambling that the worst of the dividend cuts is behind us.

I hope you’re not one of them, because this “dividend trap” is likely to spring—and steal away the income (and value) these folks have spent years building!

Just look at the numbers: unemployment is likely over 20%. Consumer spending cratered 7.5% in March, before this mess even really got started. And now Uncle Sam is demanding that any company seeking government aid first send its payout to the scrapyard.

Meantime, even cash-rich companies are pulling in their horns, like the Walt Disney Co.… Read more