I want you to think about your very first reaction when you flick on the TV and see the Dow has crashed 300, 500—even 800 points. It feels like you’re drowning, right?

It’s physical, like a gasp after falling into a cold lake. Your first instinct is likely to reach for the closest “life preserver.” For most folks, that means panicking and flipping holding after holding over to cash.

You’ve probably made this mistake. You might’ve made it last Christmas, when many investors, burned by last year’s selloff, threw in the towel …

… just in time to miss the 18% total return stocks have delivered since!

That’s no isolated incident. Look at the dips the market’s seen on its way to a 253% return in the last decade. Clearly, buying each one would have amplified your gain.

Our Next “Buy the Dip” Opportunity Is Here

Your Best Move for “Pullback-Proof” Gains

Look, I’m not going to suggest we plunge into an index fund like the SPDR S&P 500 ETF (SPY). Instead, we’ll take out some “insurance” on our gains by picking some of the best stocks in my favorite hunting ground for 5%+ dividends: real estate investment trusts (REITs).

REITs are the perfect “pullback-proof” plays,” for two critical reasons, which we’ll dive into now. Along the way, I’ll reveal two attractive “China-proof” REIT picks, plus two laggard REITs that could be collateral damage in the trade war.

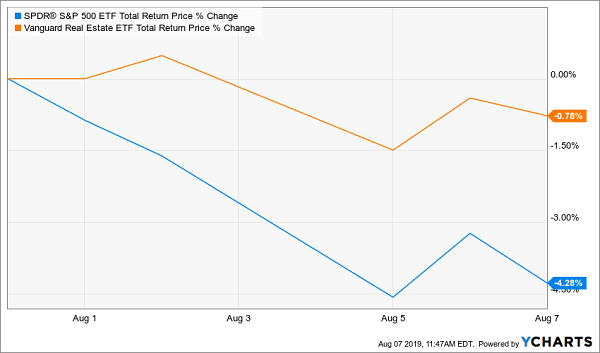

The Fact: REITs Beat Back Downturns

Most folks don’t know this, but REITs don’t fall as far as stocks in a correction, and they bounce back faster. Look at this latest pullback: the Vanguard Real Estate ETF (VNQ) barely missed a beat, while the S&P 500 flamed out:

REIT “Life Preserver” Bobs Through the Tweetstorm

You can see it again in last year’s correction, where REITs fell half as much as stocks:

REITs Halved Stocks’ Decline …

… And Bounced Back Faster

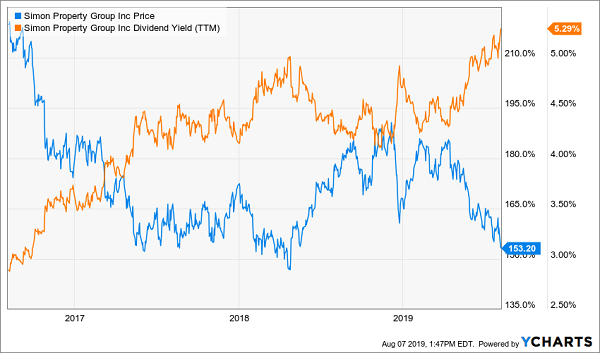

The Laggards: Simon Property Group (SPG) and STAG Industrial (STAG)

This is a great time to discuss the two REIT laggards you need to dump now, because our first one is VNQ’s No. 5 holding, mall owner Simon Property Group (SPG)—whose brick-and-mortar tenants will have to raise prices when China tariffs rise on September 1. That comes as Amazon.com (AMZN) keeps squeezing retailers!

Simon’s mall occupancy, by the way, continued to tick lower in the second quarter, to 94.4% from 95.1% in the first and 95.9% in the fourth.

And by the way, the REIT’s 5.3% yield is a mirage—it only exists because the stock cratered 30% in the last year.

A Classic Sucker’s Yield

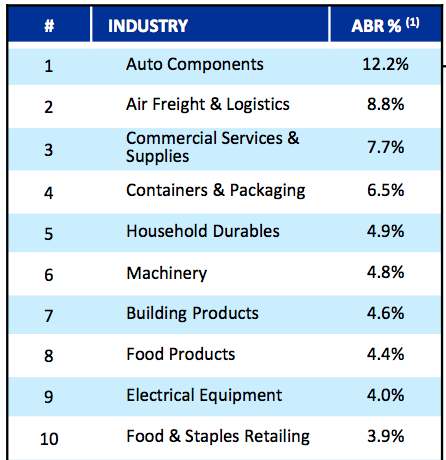

Another REIT, STAG Industrial (STAG), might also take you in with its 4.9% monthly payout.

But I’m worried about STAG, which devotes a lot of space to the slowing car business and trade-sensitive areas like logistics, containers and machinery:

STAG’s Weakness Is Obvious

Source: STAG Industrial spring 2019 investor presentation

So take a pass on these two and add stability (and growth) to your portfolio with …

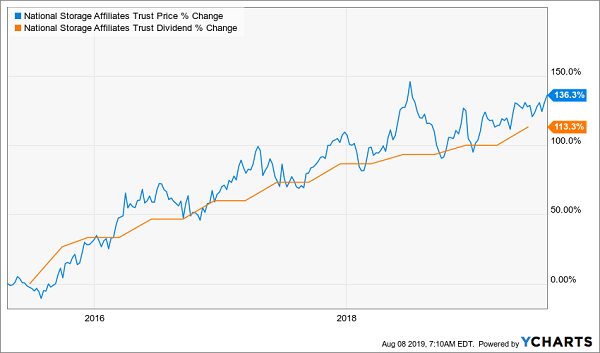

The Winner: National Storage Affiliates (NSA)

Self-storage is a great business—all you have to do is hand out the keys to the lockers and dust and sweep the place every once in a while. Self-storage REITs are also oblivious to trade and benefit from long-term trends, like baby boomers downsizing.

Enter NSA, the smallest player in the space, with 729 properties across the US and a market cap of just $1.8 billion.

But going small pays in this sector, because few folks realize NSA has one of the highest yields in the business, at 3.9%, plus the fastest dividend growth.

As I wrote in “My Ultimate Retirement Strategy for 15% Yearly Returns Forever,” a rising dividend is the key driver of share prices. NSA is the poster child, with a surging payout that’s paced the stock ahead of all other self-storage REITs. Check out how NSA’s stock rises with each individual dividend hike. The pattern is unmistakable.

A Growing Dividend Is Your Best Pullback “Insurance”

It follows, then, that NSA should continue rising so long as its dividend keep popping higher. That’s a lock: funds from operations (FFO, the REIT equivalent of earnings per share) surged 12% in Q2, and the payout is a manageable (for a REIT) at 80% of FFO.

Now let’s move on to our second reason why REITs are critical to fending off a pullback and setting yourself up for market-beating longer-term gains:

The Fact: Collapsing Rates Will Ignite REITs

Bob Michele, CIO and head of global fixed income at JPMorgan Asset Management, recently said the 10-year Treasury yield was “headed to zero.”

It’s a clever way to grab headlines, but Michele is on to something: with the Fed in easing mode, the long bond’s yield has cratered from over 2.1% to below 1.8% since Trump’s August 1 tweet.

Lower rates aren’t necessary for REITs, but they do throw gas on the fire by cutting borrowing costs and driving folks toward REITs’ big yields. And with rates headed lower and the panic (temporarily) slowing REITs’ rise, now is the time to strike.

The Winner: Digital Realty Trust (DLR)

DLR, like most data-center REITs, carries significant long-term debt on its balance sheet: about $10.8 billion worth, so it would certainly benefit from lower rates.

On the dividend side, the stock doesn’t look exciting (at first), with a 3.5% current yield. But we don’t care about the current yield; we care about the yield on our original cost. And that’s where things get exciting.

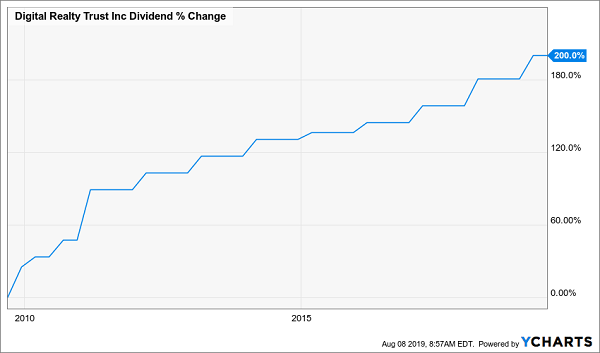

Check out DLR’s dividend growth:

DLR’s Payout Triples

Thanks to that surging payout, folks who bought back in 2009 can forget about a 3.5% yield; they’re hauling in a massive 9.9% on their initial buy today!

With the payout eating up just 62% of FFO in the past year, this “digital landlord,” which counts reliable tech players like IBM (IBM), Oracle (ORCL) and Verizon (VZ) as clients, is virtually certain to drop more hikes our way.

To get a sense of what that might look like a decade from now, let’s conservatively say the payout grows half as fast in the next 10 years as it did in the last 10. That would be enough to give you a 7.3% yield on your original cost!

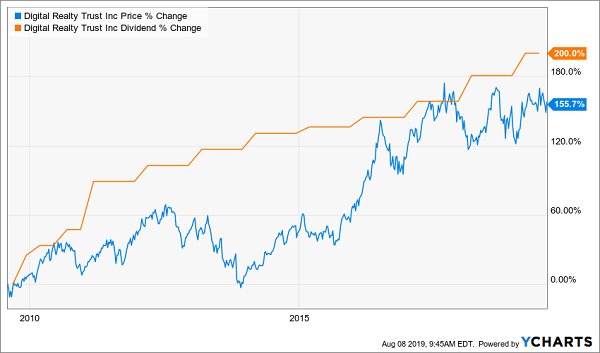

And yes, as with NSA, DLR’s payout has paced its share price higher. As you can see below, every time the stock price and dividend have diverged in the past decade, the stock has invariably popped back up to meet the dividend. The current gap represents the upside waiting for us now.

DLR’s “Dividend Magnet”

It’s only a matter of time before the first-level crowd catches on to DLR’s surging dividend and gain potential. This pullback is your chance to beat them to it.

My 2 Top REIT Buys Now (8.9% Dividends, 25%+ Upside Ahead)

These 2 REITs are solid buys now—especially, as I mentioned above, with interest rates set to fall. That sets up a nice two-part tailwind as these REITs’ borrowing costs drop and income-starved buyers pile into their stocks.

There’s just one problem: I prefer more of my return in cash than these two can provide—and we don’t want to wait a decade to get a 7%+ payout, especially when there are bigger dividends on the table right now.

That’s where the 2 other REITs I have for you today come in. Take a look:

- High-Dividend REIT Buy No. 1 taps its parent company’s massive resources to borrow cash cheap, reinvest it in a diverse portfolio of commercial properties and hand you the proceeds in the form of a rock-steady 7% payout.

- High-Dividend REIT Buy No. 2 boasts a genius business model that sets it up to benefit from rate cuts … but also positions it to gain if Powell has a change of heart. Plus, this off-the-radar pick hands you a massive 8.9% dividend!

Thanks to their ridiculously cheap valuations, these 2 picks are also poised for a nice hit of upside, especially as falling rates drive the income-starved masses into their huge—and safe—cash payouts.

How big of a gain am I talking about here? A 25% price rise in the next 12 months.

I’m ready to spill the beans on these 2 elite REITs now. Click here for full details: names, tickers, buy-under prices and more. Plus I’ll share my personal 5-step REIT picking system—it gives you everything you need to tap REITs big (and growing) dividends with confidence!