Are interest rates heading to zero in the US? Or, dare I say, negative range?

I don’t think so. But if they do, real estate investment trusts (REITs) are going to absolutely skyrocket. This year-to-date has been a sneak preview. Most REITs have seen their valuations expand with the market rally, but we haven’t missed out on all of them.

In a minute, we’ll discuss a trio of dirt-cheap REITs with attractive yields between 5% and 6%. But first, let me show you just how overstretched this market has become.

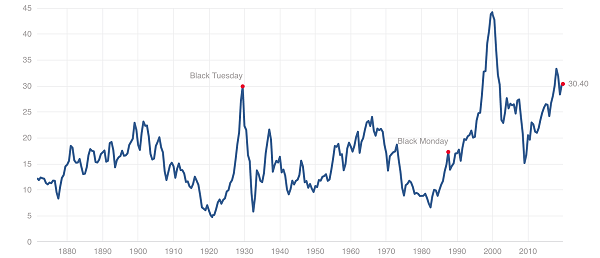

First, let’s look at the “Shiller PE.” This is the “second-level” price-to-earnings ratio, created by legendary economist Robert Shiller, that factors in average inflation-adjusted earnings over the past decade. It has only been this expensive twice in American history: The 1999-2000 tech bubble … and right before the stock market collapsed in October 1929.

Stock Valuations are Pricey (Per Shiller PE Ratio)

Source: Multpl.com

The market’s valuation doesn’t look as dire if you just look at trailing 12-month earnings, but even then, the S&P 500 has only traded this richly a handful of times previously (and in all those cases, market drops weren’t far behind).

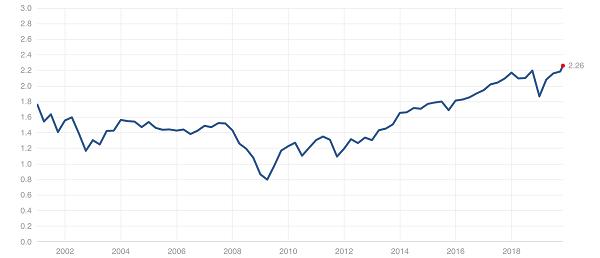

It’s not just earnings either. Stocks are exorbitantly priced based on sales:;

Investors are Paying Up for a Dollar in Sales

Source: Multpl.com

Real estate investment trusts (REITs) are no exception. The Real Estate Select Sector SPDR (XLRE) has rocketed 25% higher year-to-date, and now yields less than 3%. The average price-to-FFO ratio in the space has jumped from 15.3 at the end of 2018 to 16.4 as I write this.

I don’t know about you, but I prefer my REITs with big dividends at bargain prices!

The REIT industry does boast several names that are trading for far less than the average, but the question is: Are they cheap for a reason?

Let’s explore three REITs yielding 5% to 6% that are trading at least 25% cheaper than their peers, and see if Wall Street is missing out on any hidden gems.

Summit Hotel Properties (INN)

Dividend Yield: 5.8%

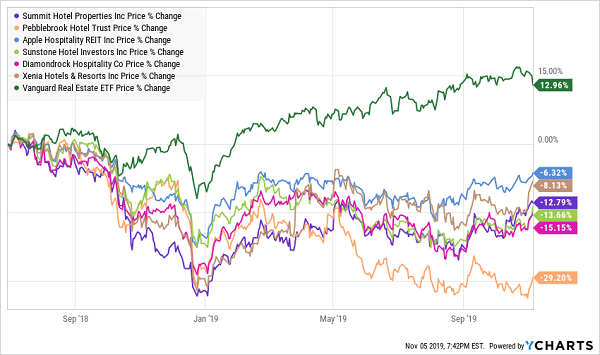

Many of the cheapest REITs on the market right now are hospitality-focused property owners. While many of them have joined the sector’s rally in 2019, they’ve been among the most notable laggards of the past 15-18 months.

Hotel REITs Have Been Inhospitable

Summit Hotel Properties (INN) is no exception. The firm boasts a 70-hotel, roughly 11,000-room portfolio that spans 24 states across the country. This is a truly diversified portfolio, too, with no single city contributing more than 9% to portfolio EBITDA. (Atlanta, San Francisco and New Orleans are its top three markets, combining to make up about 23% of EBITDA.)

Leases involve upscale brands across Marriott International (MAR), Hilton Worldwide (HLT), Hyatt Hotel (H) and InterContinental Hotels Group (IHG). However, you’ll find “efficient” peppered across the REIT’s marketing and investor materials. Properties will eschew outdated, ornate trappings and amenities such as full-service restaurants, and instead lean toward modern, functional rooms and services, as well as high-quality bars with tighter menus.

Summit also leans on in-house corporate revenue managers, exhaustive property inspections and data analytics to squeeze cash out of its properties.

Of particular interest, however, is Summit’s 51% stake in a joint venture with GIC—Singapore’s sovereign wealth fund—that it entered earlier this year. The JV’s purpose is to acquire U.S. hotels; Summit announced in its third-quarter report that it completed a four-hotel acquisition, bringing the new JV’s portfolio to five properties, worth about $300 million, in high-growth markets.

This focus on growth is great, as is its price: a dirt-cheap 9.7 times adjusted FFO. But it comes at a price: a suddenly lethargic dividend. INN, after multiple dividend increases across 2016 and 2017, has kept its payout fixed at 18 cents per share for eight consecutive quarters.

It’s possible that Summit re-prioritizes the dividend once the JV begins to yield fruit. But if you want management to place as high a priority on income as you do, look elsewhere.

Pebblebrook Hotel Trust (PEB)

Dividend Yield: 5.8%

Pebblebrook Hotel Trust (PEB) is another underpriced hotel REIT, though it shares little in common with Summit. Pebblebrook invests in upper-upscale, full-service hotels and resorts. While it does feature a few hotels under easily recognizable brands such as Hilton and Westin, the majority of its properties are more like The Donovan in Washington, Sir Francis Drake in San Francisco, or Boston’s Liberty Hotel, a boutique lodging in the former Charles Street Jail where you can dine at the “Clink” and enjoy libations in the jail’s drunk tank.

While Summit and similar operators are sprinting away from these types of hotels, Pebblebrook is making a name with them. In fact, the REIT spent a whopping $5.2 billion to buy LaSalle Hotel Properties, in a deal completed in December 2018, to get its mitts on more of these experiential properties.

Despite this massive undertaking, PEB shares are trading at a lean 11.4 times funds from operations. That FFO, by the way, continues to grow at a mid-single-digit rate, even though hotel operating performance came in under internal expectations thanks to the effects of Hurricane Dorian.

Pebblebrook does share one other trait with Summit: a stalled-out dividend. The payout has been locked in at 38 cents per share since 2016, and given $2.2 billion in debt (versus PEB’s market cap of just $3.6 billion), it’s unlikely Pebblebrook will have the financial means to give income investors a boost anytime soon.

The Dividend Isn’t Doing Pebblebrook’s Stock Any Favors

This might be a good buy-in price for a potential rebound in PEB shares, as well as a solid yield on cost. But you might be stuck with this yield for a while.

Outfront Media (OUT)

Dividend Yield: 5.4%

Let’s step out of the hotel lobby and into the subway station.

And into the bus station. And into the airport. And onto the highway.

All these places, and so many more, are the purview of outdoor advertising REIT Outfront Media (OUT). The company catches America’s eyes via a network of more than 510,000 total displays across rural, suburban and urban markets.

Yes, Outdoor’s offerings include static billboards on the highway. But as I’ve written before, this REIT has truly embraced technology. Its dynamic digital displays in places such as airports, metro trains and urban centers that can be customized depending upon location. Rather than competing with internet and mobile advertising, it sees its solutions as a way to augment them, boasting that “consumers are 48% more likely to engage with a mobile ad after being exposed to the same ad on (Outfront’s ‘out-of-home’ displays) first.”

Outfront has been growing its AFFO slowly but steadily since 2014, at a little more than 6% annually. It ran into a bit of a hiccup recently, with third-quarter numbers coming in under analysts’ expectations. But even then, its AFFO still grew at 7.2% year-over-year. Sellers may have overreacted on that one.

Outfront (OUT) Takes a Dip on Good, But Not Great, Results

Regardless, OUT shares have run nearly 40% so far this year, and remain priced to buy at just 11 times AFFO. The yield is nice, too at well more than 5%.

But again, investors are being deprived of dividend growth, with the last upgrade to the payout coming in early 2017. What’s curious is, it’s not for lack of means. Outfront is paying just 64% of its AFFO out as dividends over the past 12 months.

The REIT can afford to be a little more generous. It just isn’t.

2 REITs That Can Double Your Money, Pay 8.9% Yields

You can ride REITs to rip-roaring returns—if you do it the right way.

And the right way doesn’t involve jumping into merely above-average yielders with spotty histories of dividend growth.

Instead, it involves a select class of elite REITs that boast growth, increasing payouts and big, fat yields of nearly 9%.

I’d recommend these REITs for retirement portfolios any day of the week. But the need to buy this specific group of real estate plays has gone from “pressing” to “urgent.” That’s because my Triple-Digit Profit System just did something it hasn’t done since 2015:

It tripped its final indicator for us to dive into a totally ignored corner of the market.

The last time all five of my indicators flashed green (like they are this very minute), the group of stocks I want to show you in my 2020 REIT Playbook—where cash dividends of 6%, 7% and even 8% are commonplace—started red-hot rallies that resulted in triple-digit profits.

One member of this snubbed group of stocks—a rock-steady “landlord” spinning off a 7%-plus cash dividend—did something that income plays just aren’t supposed to do:

It soared for a market-crushing 580% return.

Doubling the Market With Real Estate Sounds Crazy, But …

It wasn’t alone. Another one of these overlooked cash machines produced a total return (so, including dividends) of 379% in just more than six years. You’re lucky to get 100% out of the market in that amount of time.

And because this stock had such a large dividend, a big slice of those returns were in cold, hard cash.

That was four years ago. Fast-forward to today, and the Federal Reserve has put its hand on the easy-money spigot, triggering the last of my five buy signals. And now, I have another pair of urgent REIT buys—boasting triple-digit price potential and yields of nearly 9%—that I want to email to you now.

The payouts are simply “going parabolic,” but it’s important that you add these stocks to your retirement portfolio now. Because when their prices go out, you won’t just miss out on their triple-digit gains—but those dividends will shrink on new buyers by the day.