Worried the economy is teetering on the brink? I don’t blame you.

Rather than running for the hills, let’s focus on recession-resistant dividend stocks. Big payout growers. We’re talking 25% to 56% dividend growth (yes, that’s no typo).

The safest dividend is the one growing the fastest. Take UnitedHealth Group (UNH), the largest health insurance carrier in the US. Its business is beautifully recession resistant. As a result, UNH is one of the most consistent growth stocks out there. Mark it down for 10%+ gains, per year, every year.

Gains in what? Every metric that matters. UNH’s sales soared 13% year-over-year. Profits popped, too. And the company raised its dividend by 14%.

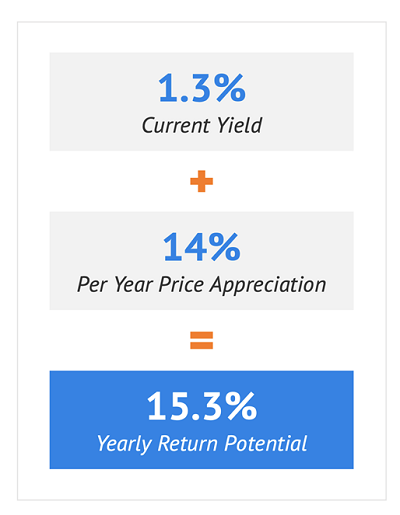

This is a formula for 15.3% returns per year, every year, holding UNH. Let’s walk through the math.

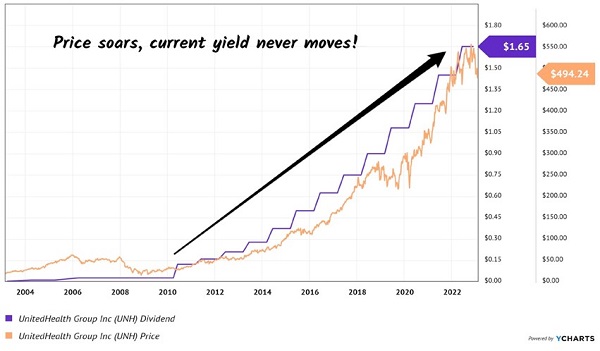

UNH yields 1.3% today. On paper, that’s peanuts and why this stock is overlooked by many vanilla dividend investors.

UNH’s yield bounces between 1% and 1.5%, for years on end. Which is interesting, because we would think that a company with 677% dividend growth over the last decade would pay more.

Well, it’s not for a lack of effort on UNH’s part. These dividend advances are “absorbed” by Mr. and Ms. Market. They see the hike and bid up the shares. The current yield never moves because the price, over time, soars! Check out these 20 years’ worth of dividend uplifts that don’t show up in the current yield. Why? Because the price chases the payout higher:

20 Years’ Worth of Dividend Hikes (and Price Gains)

UNH’s price is “in line” with its payout and rarely falls behind. That’s fine. In fact, it’s more than fine—it’s a formula for 15.3% total returns per year, every year.

Want to make more than 15.3% per year? Then find dividends that are growing even faster than UNH’s payout.

Here’s a handful of companies that raised their payouts quite generously this time last year. Raises in the range of 25% to 56%.

If they can keep it up, shareholders will be showered in riches! If not, well, they’ll be wishing they bought reliable-old UNH instead!

Pool Corp. (POOL)

Dividend Yield: 1.2%

2022 Hike: 25.0%

Projected Q2 Dividend Announcement: Early May

Pool Corp. (POOL) is the world’s largest distributor of swimming pools, swimming-related products and other outdoor goods, boasting more than 200,000 branded and private-label products throughout nearly 420 sales centers in North America, Europe and Australia. That covers everything from pools and hot tubs to pool pumps and chemicals to barbecue grills and patio lighting.

POOL was a COVID-era darling, which is probably no surprise to you. Most of us know (or are) someone who dealt with travel restrictions by putting in a pool or hot tub, expanding a deck or installing an outdoor kitchen. That sent POOL shares through the roof—at least for a time.

Like with many COVID winners, Pool Corp. has come back to earth. Which was really just a matter of time—it’s a great operator that’s well-managed, but it was caught up in breathless overbuying, and a drawback was inevitable.

Some of my readers might remember that around this same time last year, I openly wondered what kind of dividend increase Pool Corp. (POOL) would deliver in Q2 2022. At the time, I said its “dividend increase is largely up to whether it’s a reward for another good year or reflective of a difficult growth path to come.” Investors were rewarded with a massive 25% hike, and the company followed that up with a much better full-year 2022 financial performance than it originally projected (record sales on 17% revenue growth, and 17% EPS growth).

But in the same report, Pool Corp. anticipated a 12% decline in EPS at the midpoint of its expected range, largely blaming “challenged” pool construction levels compared to the past two blowout years. POOL has plenty of room to expand the dividend by expanding its low 20% payout ratio, but I wouldn’t be surprised at a much more modest payout increase in early May, when it typically announces its annual hike.

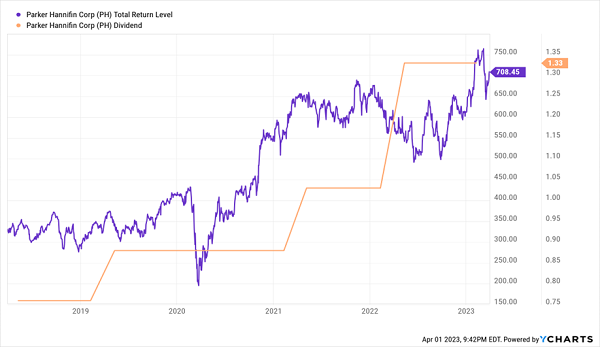

Parker Hannifin (PH)

Dividend Yield: 1.6%

2022 Hike: 29.1%

Projected Q2 Dividend Announcement: Late April

Parker Hannifin (PH) produces motion and control technologies and systems for a variety of industries, including aerospace, healthcare, energy, chemical processing, industrial equipment, transportation and more. Moreover, its applications for heavy construction equipment, as well as liquids removal for construction sites, prompted me to flag it as an infrastructure-bill winner a couple years ago.

But what makes Parker even more attractive is a series of acquisitions over the past few years that should increase its percentage of recurring sales, making it less cyclical than your typical industrial stock.

That’s good, because PH targets a dividend payout ratio of 30%-35%, so the only way to dividend growth is earnings growth. Indeed, it paused its payout at 88 cents per year during 2020, when COVID held back its business—but raised the dividend by 29% in 2022, amid a fiscal year that saw it grow profits by nearly 25%.

In turn, that means we might be able to expect more consistent stock growth from PH, which definitely seems to benefit from the dividend magnet.

As for this year: Parker Hannifin is tracking for a more modest year of single-digit earnings growth. So when it comes time for PH to announce its next dividend hike in late April, it could be a more limited improvement compared to 2022.

PH Could Be a More Dependable Industrial Stock

Lowe’s (LOW)

Dividend Yield: 2.2%

2022 Hike: 31.25%

Projected Q2 Dividend Announcement: Late May

Big-box DIY giant Lowe’s (LOW) is a rarity among Dividend Aristocrats.

Typically, once you break the 25-year threshold it takes to attain dividend aristocracy, it’s mostly downhill from there—not as a company, of course, but as an aggressive dividend grower. Growth slows, and there’s only so much of your profits you’re willing to pay out as dividends.

And if you’re sitting at more than a half-century of uninterrupted payout hikes, like Lowe’s is? Well, you’d figure the old boy would be limping into every dividend announcement.

And You’d Be Wrong

Lowe’s has allowed its dividend to balloon by more than 150% across the past five years, with the lion’s share of that coming over the past two years.

The story is much the same as Pool Corp: COVID provided a wonderful (but temporary) boost as Americans upgraded their homes. Profits soared as a result, and Lowe’s generously shared those profits with shareholders. But now, the company’s momentum is expected to slow this year—in fact, profits are expected to slide back by 1% or 2%—as the housing market eases. And that could limit Lowe’s next dividend increase, which should be announced in late May.

I’m not sour on Lowe’s, though. While stocks more tightly tied to homebuying and new-home construction could suffer more, the home-improvement market should be more resilient because homes don’t stop aging, and Americans still have high disposable income to re-invest in their houses.

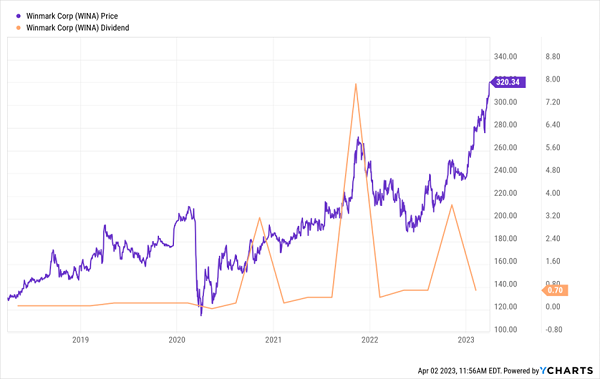

Winmark (WINA)

Dividend Yield: 1.1%

2022 Hike: 55.6%

Projected Q2 Dividend Announcement: Mid-April

Winmark (WINA) is as inconspicuous a dividend stock as you could ask for. Its sub-2% yield isn’t drawing any attention, nor is its business, which is as a franchisor of used-goods stores.

Winmark is the name behind a collective 1,300 or so locations of Plato’s Closet, Once Upon A Child, Play It Again Sports, Style Encore and Music Go Round—a group of retailers that deal in secondhand apparel, sports goods and musical instruments.

But the business—at least for Winmark—isn’t retail, but franchising. WINA finds entrepreneurs that want to operate one of its businesses, outline rules of operation, train these franchisees, and sign them up for agreements that can be renewed after 10 years—which, in 2022, 100% of them did. Royalties from these franchisees make up 85% of the business, and franchise fees another 2%.

It’s not a red-hot growth business, but it does grow—and that has allowed Winmark to boost its base quarterly payout by an average of 47% annually since 2019.

I stress base, because the quarterly dividend doesn’t tell the whole story.

Winmark Is a Special Dividend Payer

Winmark did have a hiccup: It briefly cut its dividend, from 25 cents to 5 cents, for a quarter in 2020. But it not only restored it quickly—the same year, it started what is now a multiyear streak of delivering special payouts, similar to the fixed-and-variable programs of many energy stocks. Even with those special payouts, WINA’s yield is less than 2% (the regular dividend comes out to less than 1%), so it’s certainly not a solution for investors who need major current income right this second.

Will Winmark follow up on last year’s 56% increase with something equally as impressive in mid-April? The odds are low just given the size of the last increase. But given that the regular payout accounts for just 22% of profits, we could still expect a hefty rise.

It’s Not Too Late: Lock In the “Recession-Resistant Portfolio” Now!

One last trait Winmark boasts is a vital one as we march right into the mouth of a likely recession: recession-resistance.

While every major market index was dead money last year, and while most of the darlings of the stock market have been getting crushed in 2023, a small, overlooked basket of recession-resistant stocks haven’t just been surviving—they’ve been setting up to thrive.

And now, they look like they could be the market’s best protective plays heading into a turbulent 2023.

To the uninformed investor, these stocks will seem downright boring. In fact, I’m betting that you haven’t heard of any of these—after all, the mainstream media rarely covers some of them, and it outright ignores others.

But these “Hidden Yield stocks” offer savvy investors the potential to double their money roughly every five years, regardless of what the wider market does.

How can they do this when even idiot-proof blue chips can’t?

It all boils down to what I call “The Three Pillars”:

Pillar #1: Consistent Dividend Hikes

Pillar #2: Lagging Stock Price

Pillar #3: Stock Buybacks

Selecting companies with a proven track of increasing their dividend payments is the safest, most reliable way to get rich in the stock market. And I want to show you how it’s done. Click here to learn how to get my exclusive report, 5 Recession-Resistant Dividend Stocks With 100% Upside, including full analyses of each pick … along with a few other bonuses, too!