Real estate investment trusts (REITs) are great potential fits for any modern retirement portfolio. With interest rates ticking down from 2% to 1% and, perhaps, eventually 0%, these generous dividend payers are benefitting big time.

REIT stocks tend to yield twice as much as regular ol’ stocks. They collect rent and pay it directly to their investors as dividends. This “capital light” approach gives them cash cow status. It’s a big reason why REITs outperform the broader market over any length of time.

So should we just buy the biggest, most successful REITs and enjoy their dividends and the growth of their payouts.

In a word… no.

Some REITs are seriously overpriced. If we buy them when they are expensive, we can lose 10%, 20% or even 30% or more of our capital. It’s the same risk here as buying a regular stock trading for a high price-to-earnings (P/E) ratio.

I recently showed you why you can’t rely on screeners in real estate. Instead, we have to dig into “funds from operations,” or FFO, which is a metric unique to REITs that explains their profitability far better than straight-up net income can.

When a REIT’s price-to-FFO ratio gets out of whack with its fundamentals, or with those of its rivals, you should take a closer look. If the number jumps too far too fast, or is just too high to begin with, it could be time to make an exit.

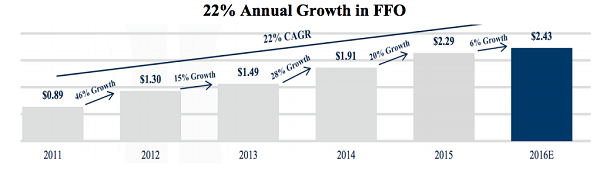

Consider Chatham Lodging Trust (CLDT). In 2016, it traded at a bargain 8.4 times FFO. (This means that the REIT was generating enough cash flow to pay us back in just 8.4 years. Anything under 10 is quite cheap, as it infers an “FFO yield” above 10%.)

Why was Chatham so cheap? Investors fretted needlessly that the firm’s hotels would be overrun by the likes of Airbnb. These worries knocked the REIT far below what it was truly worth. Once you looked under the hood, you realized this was a longstanding growth story that was ignoring these headline headwinds.

Source: Chatham Lodging Trust

That incredible 22% average yearly growth was driving a surging dividend, up 57% in just three years! Best of all, this stock was yielding 6.8%–its highest level ever.

I actually issued a buy call for CLDT in my December 2016 Contrarian Income Report. After all, it ticked all our boxes: High yield. Fast dividend growth. Cheap valuation.

The good news? The REIT surged. But after about two years, in September 2018, Chatham’s price-to-FFO ratio became a little too plump. The cat clearly was out of the bag, so we contrarians checked out with a 26% total return.

The pricey stock had no where to go but sideways. Here’s how it did since we rang the register:

Chatham Plunges Since Our Sell Call

Of course price-to-FFO isn’t the only number to consider when buying a REIT. Its movement compared to a REIT’s history and FFO growth—and the ratios of similar REITs—can give you a strong hint of whether it’s time to buy (or sell).

Here are three REITs that are quietly quite expensive. Investors are buying them for their dividends and ignoring the risk that may come if their price-to-FFO ratios contract. (And the higher the multiple, the greater the chance that this will happen.

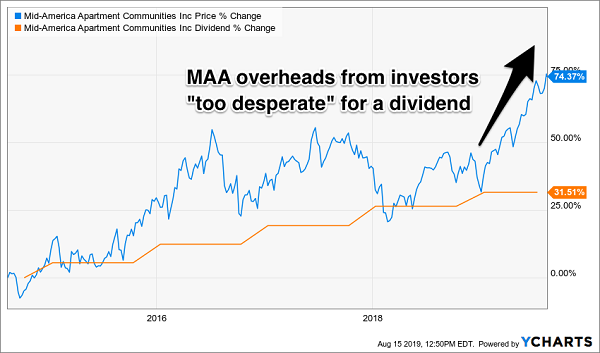

Mid-America Apartment Communities

Dividend Yield: 3.1%

A growing number of companies are starting to understand the road to riches is serving the rich. Whether it’s Vail Resorts (MTN) and its upscale ski properties, Host Hotels & Resorts (HST) and its Ritz-Carltons and luxury resorts, or Ferrari NV (RACE) with its world-class cars, it’s clear there’s money to be made by catering to the well-to-do.

Mid-America Apartment Communities (MAA) walks a different path.

This apartment REIT doesn’t follow peer such as UDR Inc. (UDR) and Essex Property Trust (ESS) into the more lucrative residential markets of the East and West coasts. Instead, Mid-America services metro areas such as Dallas-Fort Worth-Washington (Texas), Phoenix-Mesa-Chandler (Arizona) and Savannah (Georgia) in the Southwest, Southwest and Mid-Atlantic.

This is a growing company that I’ve lauded this year, and as far back as 2016, for both its ability to squeeze growing FFO out of these less appreciated markets, and the fact that it funnels these funds back into its expanding dividend.

Income Investors Overdoing It

But this stock is due for a break. It’s now trading for more than 22-times FFO!

This REIT is priced for perfection. Anything less will mean disappointment for buyers at this price.

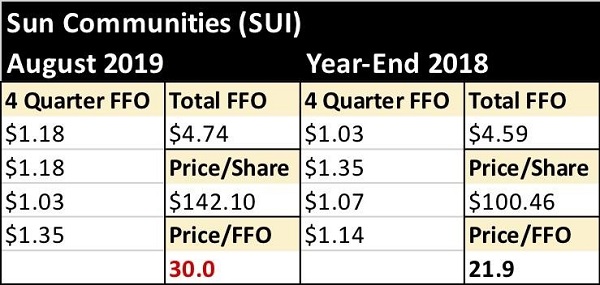

Sun Communities (SUI)

Dividend Yield: 2.1%

Sun Communities (SUI) owns and/or operates more than 380 manufactured-housing and recreational-vehicle communities across 31 states and Ontario, Canada. It also offers a wide option of solutions for residents: You can actually buy manufactured homes from Sun, or rent one, or take your own home and plop it on one of their home sites.

And then there are its “RV resorts,” which will knock the stereotypical trailer-park image right out of your head.

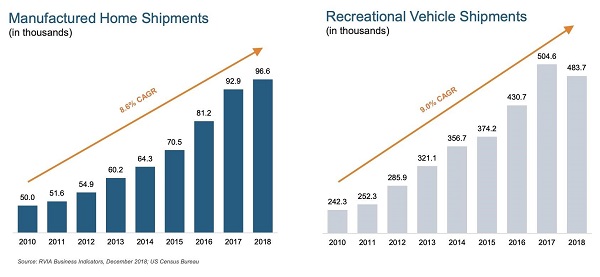

Sun is riding a mostly growing trend of both manufactured-home and recreational-vehicle shipments that have driven operational funds ever higher for years.

A Bull Market in Sun’s Shipments

Source: Sun Communities June 2019 Investor Presentation

That in turn has helped a 161% run since 2014, including a sizzling 40% rally year-to-date. But SUI’s rise hasn’t been wholly driven by profit growth—investors have been increasingly willing to overpay, driving the valuation to a cringeworthy 30 times FFO at current prices.

I like what this “blue-collar” REIT is accomplishing. But it’s usually not a good idea to pay 30-times FFO for a landlord.

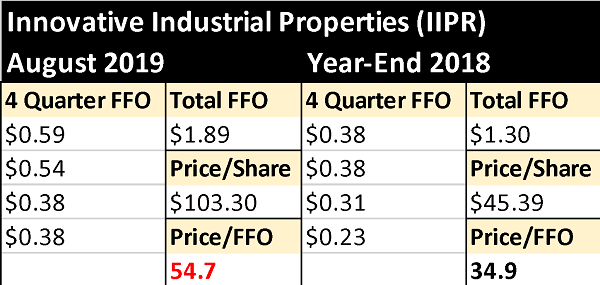

Innovative Industrial Properties (IIPR)

Dividend Yield: 2.2%

An interesting backdoor play on the pot sector is landlord Innovative Industrial Properties (IIPR). Remember, while many states have legalized pot, it remains illegal under federal law. Cash is king and financing is challenging for weed peddlers, so many are selling their properties to IIPR to raise cash and become tenants.

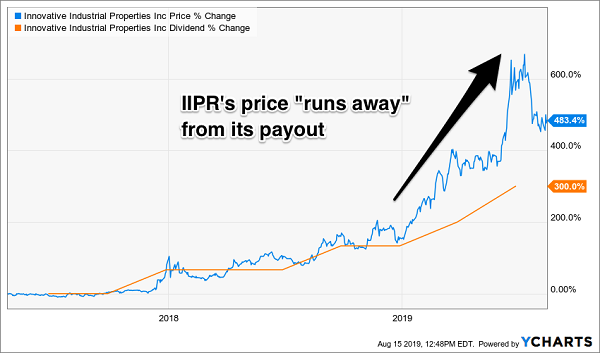

Why IIPR? It’s the only real estate investment trust (REIT) that works with weed growers. As a publicly traded company, it gets to borrow money at much lower rates than it collects from its cannabis clients. As a REIT, IIPR is obligated to dish most of its profits back to its shareholders as dividends. The result is a good old-fashioned payout boom, a 200% increase in less than two years:

The Landlord’s High

The only “problem” with the chart above is that, if you don’t yet own IIRP, it is now quite expensive to do so. Its price line has run away from its payout line, which is a sign that shares are dangerously overvalued. The stock now pays just 2.1% and trades for an extremely rich 54-times its annual cash flow.

Sure, you may be able to buy IIRP “high” and sell it higher. But that’s a different dividend drug altogether.

A better bet? Two reasonably priced REITs that pay triple the dividends of these too-popular names…

2 REITs That Can Double Your Money, Pay 8.9% Yields

Even though I’m avoiding IIPR for now, that’s not because I think you can’t ride REITs to rip-roaring returns. You can–if you do it the right way.

And I can show you how.

Real estate investment trusts are such a powerful dividend tool that they can make the difference between just getting by in retirement… and breezing by.

Retirees that have a healthy allocation to REITs clip vacation pictures for their photo albums.

Retirees that don’t? They greet you at Walmart.

But the need to buy REITs for your retirement portfolio has gone from “pressing” to “urgent.” Because my Triple-Digit Profit System just did something it hasn’t done since 2015: It tripped its final indicator for us to dive into a totally ignored corner of the market.

The last time all five of my indicators flashed green (like they are this very minute), the group of stocks I want to show you in my brand new REIT Playbook—where cash dividends of 6%, 7% and even 8% are commonplace—started red-hot rallies that resulted in triple-digit profits.

One member of this snubbed group of stocks—a rock-steady “landlord” spinning off a 7%-plus cash dividend—did something that income plays just aren’t supposed to do:

It soared for a market-crushing 580% return.

Double Your Dividends and Returns with These REITs

It wasn’t alone. Another one of these overlooked cash machines produced a total return (so, including dividends) of 379% in just more than six years. You’re lucky to get 100% out of the market in that amount of time.

And because this stock had such a large dividend, a big slice of those returns were in cold, hard cash.

That was four years ago. Fast-forward to today, and the Federal Reserve has put its hand on the easy-money spigot, triggering the last of my five buy signals. And now, I have another pair of urgent REIT buys—boasting triple-digit price potential and yields of nearly 9%—that I want to email to you now.

The payouts are simply “going parabolic,” but it’s important that you add these stocks to your retirement portfolio now. Because when their prices go out, you won’t just miss out on their triple-digit gains—but those dividends will shrink on new buyers by the day.