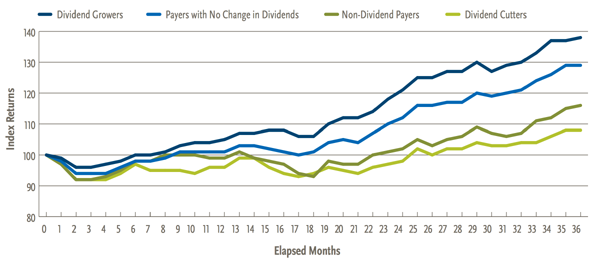

As interest rates rise, the best defense will be a good offense. Research from Nuveen and Ned Davis confirms what we already knew – that dividend growth stocks outperform everyone else in the 36 months after a Fed rate increase:

Stock Returns After Fed Increases

That’s no surprise either, because payout growers always outpace their counterparts.

Everyone loves dividends, but dividend hikes are underappreciated. Not only do they increase the yield on your initial capital, but they often are reflected in a price increase for the stock.

For example, if a stock pays a 3% current yield and then hikes its payout by 10%, it’s unlikely that its stock price will stagnate for long. Investors will see the new 3.3% yield, and buy more shares. They’ll drive the price up, and the yield back down – eventually towards 3%. This is why your favorite dividend aristocrat never pays a high current yield – its stock price rises too fast!

But what if you need more income than 3%?

6 Payout Unicorns: 6% Dividends With Big Upside

Only 200 or so of some 10,000 U.S. equities pay 3% current yields, with meaningful dividend growth to boot. Double your yield requirement to 6%, and we’re down to only about 35 names.

Now this short list has the potential to form the perfect retirement portfolio. Think about it – a million dollars invested in these names will net you at least $60,000 in annual income.

Plus, thanks to payout growth, you’ll receive healthy annual raises – so that you’ll never have to worry about selling any shares to raise money. Your dividends, along with the annual raises you receive, will fund your retirement entirely.

Of the 35 names I uncovered, here are six that look great on paper. Though we’ll eliminate one, leaving five worthy of future consideration.

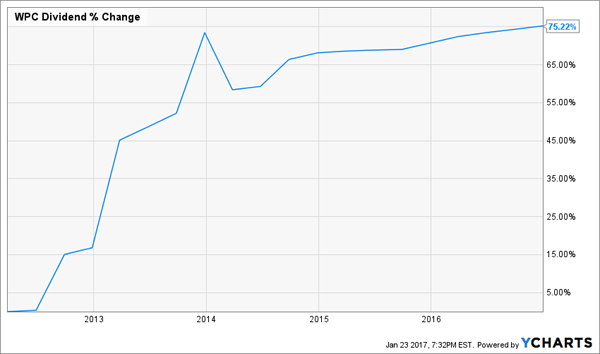

W.P. Carey (WPC) owns and manages commercial real estate, a market that is quietly booming. While blue chip counterpart Realty Income (O) pays just 4.2%, WPC boasts a generous 6.5% yield – showing once again why the best deals in real estate are often found with “B-List” REITs.

About 99% of WPC’s leases have rent increases “baked in.” And when they raise the rent, their investors pocket the increase:

A 75% Dividend Increase Over 5 Years

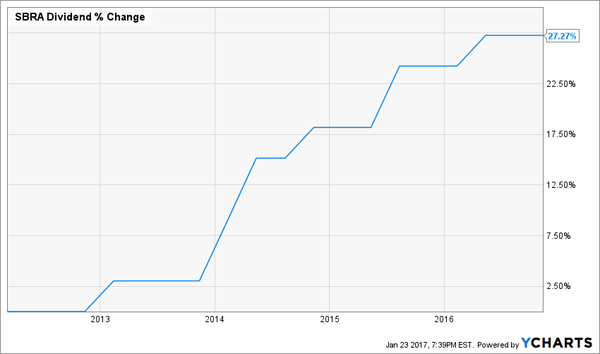

Sabra Health Care (SBRA) invests in skilled nursing and senior housing facilities – and it’s benefiting from the aging of America. The firm has steadily increased its funds from operations (FFO) each of the past five years. This is a key metric for REITs like Sabra because higher FFO drives higher dividends – like these:

Higher Rents, Higher FFO and Higher Dividends

Shares pay 6.5% today.

CorEnergy Infrastructure (CORR) saw two big tenants go bankrupt during the energy slide of 2015. It paid $3.00 in dividends that year but only generated $0.79 in FFO – and that disparity caused the stock to sell off.

Since then, CORR has been able to right the ship, with $3.67 per share in FFO over the past twelve months. Shares pay a generous 8.3% yield today, and management projects a long-term return of 8-10% thanks to rent increases and acquisitions.

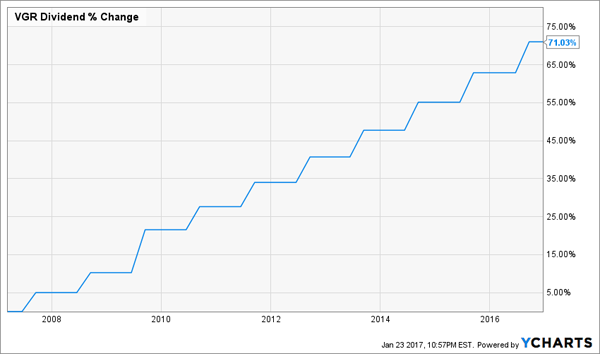

Vector Group (VGR) is a tobacco and real estate conglomerate (yes, you read that right). Its tobacco side is a cash cow, requiring very little reinvestment – just $6 million per year on $268 million in profits.

Vector pays a 7% dividend today, and the company raises its payout like clockwork every year:

Vector’s Steady Dividend Staircase

The company is also funneling its tobacco profits into its real estate business, which is growing faster and now make up 40% of revenues.

Blackstone Mortgage Trust (BXMT) funds commercial real estate development. Thanks to onerous bank regulations that restrict commercial loans, the need for commercial financing is, rather quietly, booming.

BXMT makes floating rate loans, so its portfolio should continue to perform well as rates rise. The stock pays 8% today.

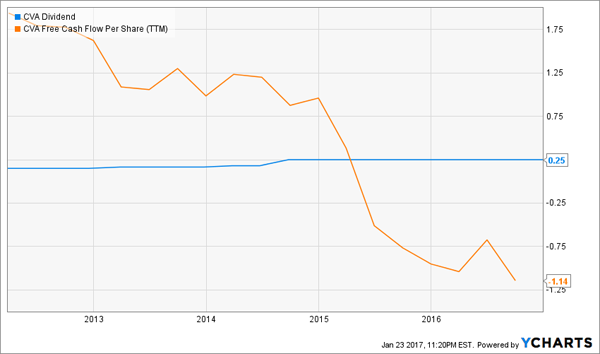

Finally Covanta Holding (CVA) literally turns waste into energy. It’s a feel good story, with four dividend hikes in the last five years and a generous 6.3% current yield.

Problem is, the firm’s free cash flow (FCF) has deteriorated into its own pile of waste:

Negative FCF Weights on the Dividend

Falling FCF (and FFO) rarely coincides with dividend hikes. In fact, they’re more likely to cause a payout cut – making Covanta a stay away.

3 More Retirement Plays Paying 7%+ (With 38% Upside)

Thanks to the current hysteria regarding interest rates, President Trump and inflation – good old fashioned headline-driven insanity, in other words – there are once again pockets of value that pay meaningful dividends of 7% or better.

And my favorites have 38% price upside to boot!

These top 7% payers for 2017 all have something in common – they ended 2016 out of the eye of the mainstream investing world. And thanks to their relative obscurity, these stocks are cheap with yields that are high.

There’s no reason for these retirement plays to be so inexpensive other than the fact that few investors are on this income beat. But I expect that to change soon – which means the best time to buy these 7% dividends is right now.