Today, we’re going to highlight the four best retirement funds Vanguard has to offer. Since my favorite retirement fund closed its doors to new investors, I had to find more high quality, high income and low cost options for readers like you to consider.

The Vanguard Group is the top mutual fund provider by assets under management, boasting nearly $3 trillion across more than 125 mutual funds. And almost all of that is locked up in long-term assets — a statement about Vanguard’s elite standing among buy-and-hold retirement investors.

Vanguard doesn’t do leverage, it doesn’t do inverse. With very few exceptions, Vanguard’s funds aren’t trading instruments. Instead, they’re for investors looking for a low-cost way to grow their nest eggs for the long haul.

Still, some funds are better for retirement than others. Many Vanguard mutual funds, while extremely useful, are better suited for tactical investments that span just a couple of years. Other Vanguard funds are little more than glorified parking lots for cash.

But a few gems stick out like a sapphire thumb.

Here’s our look at four Vanguard retirement funds that are top choices for any retirement portfolio, and no-brainer buys if you’re lucky enough to have them on offer in your company’s 401(k) plan.

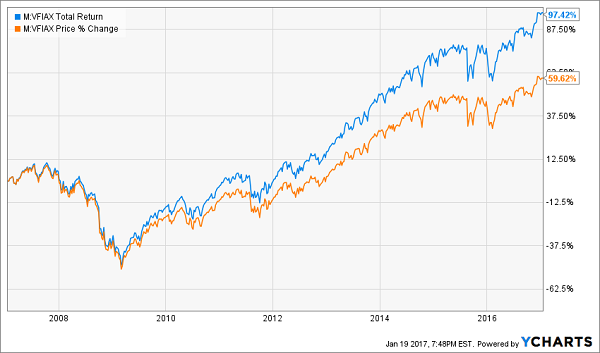

Vanguard 500 Index Fund (VFINX, VFIAX)

Type: Large-cap stock (index)

Expenses (VFINX Investor Shares, Minimum Investment of $3,000): 0.16%

Expenses (VFIAX Admiral Shares, Minimum Investment of $10,000): 0.05%

Yield: 2.1%

Beating “the market” is no small task, especially if you try to do it using only large, blue-chip stocks. Many hedge fund managers can’t do it. Many mutual fund managers can’t do it. And the vast majority of individual investors fall far short.

Thus, one of the best things you can do to give yourself a fighting chance in retirement is simply match the market … by investing in it. And there are few better ways to do so than the Vanguard 500 Index Fund (VFINX).

Vanguard 500 Index Fund is one of many mutual funds that allow investors to track the S&P 500, providing exposure to 500 blue-chip companies including Apple (AAPL), Microsoft (MSFT) and Alphabet (GOOGL). But Vanguard stands above just about all competitors because of its dirt-cheap expenses. While the Investor-class shares are still very inexpensive compared to other S&P 500 trackers, Admiral-class shares allow you to buy the S&P 500 for just $5 annually on every $10,000 you invest. And the $10,000 minimum buy-in is one of the lowest thresholds Vanguard offers for its lower-cost Admiral shares.

Vanguard 500 Index Fund: An Easy Path to Solid Total Returns

Including dividends, VFIAX has returned 7% on an annualized basis over the past decade. That won’t set the world on fire, but it’s a solid anchor for most portfolios.

Vanguard 500 also is available in ETF form as the Vanguard S&P 500 ETF (VOO), which charges 0.05% in expenses.

Vanguard High Dividend Yield Index Fund (VHDYX)

Type: Large-cap dividend stock (index)

Expenses (VHDYX Investor Shares, Minimum Investment of $3,000): 0.16%

Yield: 3%

We’ve pointed out before that while Vanguard does offer quality dividend funds, it’s not really a source for eye-popping yield. That’s why any investor interested in Vanguard High Dividend Yield Index Fund (VHDYX) should temper their expectations.

Because Vanguard High Dividend Yield doesn’t really offer high dividend yield.

It does offer quality dividend yield, however. VHDYX invests in 420 stocks with a median market cap of $108 billion. In other words, this is another blue-chip-focused fund – it just puts a bit more emphasis on higher-yielding holdings. Thus, Vanguard 500 holdings like Alphabet, Amazon.com (AMZN) and Facebook (FB) get the boot, and High Dividend instead focuses more on the likes of Microsoft, Exxon Mobil (XOM) and Johnson & Johnson (JNJ).

Vanguard High Dividend Index Fund: Slower Growth, More Cash

But for its differences in holdings, the performance in VHDYX is almost identical to VFIAX, with 7% annual returns over the past decade. The biggest difference is that more of High Dividend’s returns came in the form of cash payouts.

Vanguard High Dividend Yield also is available in ETF form as the Vanguard High Dividend Yield ETF (VYM), which charges 0.09% in expenses.

Vanguard High-Yield Corporate Fund (VWEHX, VWEAX)

Type: Investment-grade bonds (actively managed)

Expenses (VWEHX Investor Shares, Minimum Investment of $3,000): 0.23%

Expenses (VWEAX Admiral Shares, Minimum Investment of $50,000): 0.13%

Yield: 4.8%

Naturally, retirement investors are going to be awfully interested in collecting income in retirement, and while you can do that via dividend equity funds, it’s smart to diversify into bonds as you near the finish line.

And on that front, Vanguard High-Yield Corporate Fund (VWEAX) might be the best that Vanguard has to offer.

VWEAX invests in junk-rated corporate debt – basically, medium- to low-quality bonds that yield more thanks to their additional risk. However, while VWEAX yields nearly 5% — nothing to sneeze at – much of its debt, while junk-rated, falls on the upper end of the junk spectrum, so investors aren’t loading up on completely garbage bonds.

Moreover, this is an actively managed fund, but it’s not priced like one. Instead, you’re getting an experienced hand in the debt world – Michael L. Hong, CFA, who has managed VWEAX since 2008 – for the price of an index fund.

Vanguard High-Yield Corporate Fund Offers Big Income for a Song

While VWEAX hasn’t matched Vanguard 500 or High Dividend in performance over the past decade, it’s awfully close at about 6.5% returns annually. More importantly, High-Yield Corporate has bested the average high-yield bond fund over the trailing three-, five- and 10-year periods.

Vanguard Wellesley Income Fund (VWINX, VWIAX)

Type: Balanced fund (actively managed)

Expenses (VWINX Investor Shares, Minimum Investment of $3,000): 0.23%

Expenses (VFIAX Admiral Shares, Minimum Investment of $50,000): 0.16%

Yield: 2.9%

If your goal is solid portfolio performance in the simplest way possible, Vanguard Wellesley Income Fund (VWIAX) is an all-in-one tool kit that isn’t just effective, but frugal, too.

The VWIAX is a so-called “balanced” fund, though in reality, that simply means it holds some bonds and some stocks. But it’s not perfectly balanced – Wellesley Income is actually heavily tilted toward bonds, with 61% of the portfolio invested in varying shades of investment-grade debt, and the rest dedicated to big, blue-chip stocks.

The income part of the portfolio is heavily weighted in industrial (36%) and financial (26%) sector corporate debt, though Treasuries (16%) also make up a significant chunk. Meanwhile, the equity part of the portfolio is well-balanced, with six sectors earning double-digit allocations. Top holdings here include Microsoft, JPMorgan Chase (JPM) and Wells Fargo (WFC).

Vanguard Wellesley Income Fund Offers the Best of Both Worlds

For a one-stop shop, Wellesley Income has been extremely competitive. The fund has produced 6.8% in annual total returns over the past decade, with much of that coming under the advisory of John C. Keogh and W. Michael Reckmeyer, III, who have advised the fund since 2008 and 2007, respectively.

You could do a lot worse than getting nearly 7% a year out of what’s essentially a simple diversified portfolio in a single fund.

3 Can’t-Miss Funds Paying 8% in Dividends

These Vanguard funds are some of the lowest-risk offerings for retirement investors, and they’re among the very best options you could ask for if they’re available in your 401(k).

But 3%-5% yields with little risk is about the best income solution you could ask for, right?

Wrong. Oh so wrong.

I want to introduce you to my 8% “no withdrawal” retirement strategy, which features a number of generous AND secure dividend payers that will allow you to rely entirely on dividends … while growing your principal!

That’s right. This isn’t nest egg protection – it’s nest egg growth. Not only will this strategy offer 8% yields, but it will also help your principle balloon to 110% after year 1, 120% after year 2, and so on.

The key to this strategy is a collection of super-stocks and can’t-miss funds that …

- Pay 8% or better.

- Have well-funded dividends.

- Trade at meaningful discounts to their intrinsic values.

- Know how to make their shareholders money.

I’ve been buried in research for weeks, grilling management because online tools simply don’t provide enough information. I also track insider buying, because I want to make sure corporate leadership has skin in the game. After all, if insiders own a ton of shares … well, they’ll want to return a lot of corporate wealth to shareholders like themselves!

I’m particularly excited about this trio of “blue-chip” funds because they not only provide retirement diversification, but they boast outstanding income and value! These are funds that yield 8% to 10% and trade at 10% to 15% discounts to their net asset value (NAV)! What more could you ask for?

These funds are perfect for the current market environment, too, because they can absorb volatility and still pay out fat dividends while you wait for the chaos to clear.

Do you want to be able to live off dividends for life and never worry about your nest egg? Then these are the perfect holdings for you. Click here and I’ll explain more about my no withdrawal approach – plus I’ll share the names, tickers and buy prices of my three favorite closed-end funds for 8.2%, 9.9% and 10.1% yields.