No two ways about it: This stock market is getting twitchy, and it’s (frankly beyond) time for all investors to take it seriously.

Trade wars. The possibility of spiking inflation. The Fed’s “will they or won’t they” act around rate cuts. And then there’s the ongoing doubt about whether AI will deliver on its big profit promises.

Our 3-Step Volatility Plan: Boost Income, Cut Taxes—and Go Beyond Stocks

We’re all feeling it: The market heads higher, and every day it does, the voice in our head telling us that a fall is around the corner grows just a little bit louder.

So what are we going to do? We’re certainly not going to abandon stocks—or the stock focused closed-end funds (CEFs) in our CEF Insider portfolio.

Because over the long run, stocks are still the No. 1 way to build wealth for pretty well all investors (and of course, we do not want to reduce our income stream from our stock holdings). But we are going to take the prudent step of bolstering our stock holdings with CEFs holding another asset that gives us reliable income, low volatility and a valuable tax shelter, too.

I’m talking about municipal bonds, which state and local governments issue to pay for infrastructure projects. As I’ll show you below, these so-called “boring” investments are anything but. Plus we get a package of “extra” benefits when we buy our “munis” through 7.5%-yielding CEFs.

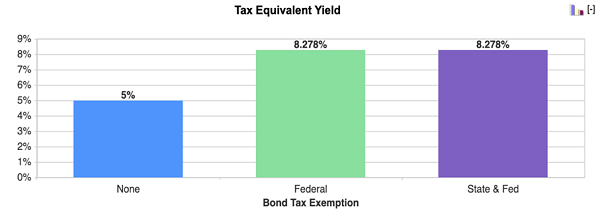

Munis Transform a 5% Yield Into 8.3%

Munis have long been a go-to for conservative income investors. They provide tax-free income, low default rates and a loyal investor base that tends to buy their munis and hang on to them forever, helping further reduce volatility.

Further helping reduce volatility is the fact that there are strict rules in place to ensure municipalities only borrow as much as they can afford. This lets us collect munis’ high yields with less stress than we might have with taxable bonds and stocks.

Since many munis’ dividends are federally tax-free (and some are even exempt from state and local taxes), they tend to appeal to wealthy investors, as well. Look at this:

Source: Bankrate.com

As the chart above shows, if you’re in the highest tax bracket, a 5% yield from a muni bond (or a CEF holding munis) is equal to 8.3% from a taxable bond or stock (and the three muni-bond CEFs we’ll look at below yield a lot more than that!).

2025 Uncertainty Opens Our “Muni Buy Window”

Muni-bond yields are higher than they’ve been in years, thanks to the Federal Reserve’s rate hikes, which allowed muni-bond CEFs to buy higher-yielding bonds. Now that rates are falling more slowly than originally expected, there’s still a large pool of higher-yielding munis available for our CEFs to buy.

And when the Fed goes back to cutting rates, likely later this year, those bonds should see price gains—particularly intermediate- and long-duration bonds—as they’ll have more appeal than newly issued bonds that yield less.

Moreover, with 2025 likely to show lower stock returns than 2023 and 2024, more stock investors should be looking to pick up munis, as well, adding to our buy case here.

3 Cheap Muni-Bond CEFs (Yielding 12.5% on a Taxable-Equivalent Basis)

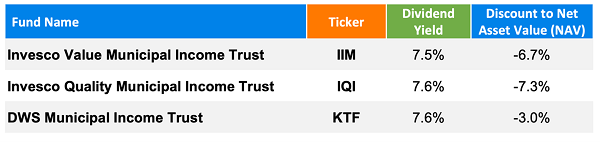

With all that said, let’s look at three high-yielding muni-bond CEFs with attractive discounts: With over 7.6% dividends on average, these funds produce an incredible income stream equal to a 12.5% taxable yield.

IIM: A Muni Fund With Long-Term, Durable Income

Let’s start with the Invesco Value Municipal Income Trust (IIM). This fund, like all three of our muni-bond CEFs, focuses on undervalued muni bonds from across the US, which limits its geographic risk. As you can see above, it trades at a 6.7% discount to net asset value (NAV, or the value of its underlying portfolio), which means we’re buying its holdings for a little over 93 cents on the dollar.

Like most CEFs, the fund uses leverage to boost returns—in the case of IIM, it has borrowed against about 32% of its portfolio. That’s reasonable for low-volatility assets like munis. Moreover, Invesco can borrow for much less than you and me—and its borrowing costs will fall as interest rates do.

Perhaps the best thing about IIM, though, is that the weighted average maturity of its portfolio is 18.8 years, incredibly long for a bond fund. This means IIM has locked in high yields that can be relied on for nearly two decades.

If interest rates start to fall fast, expect investors to pivot to funds like IIM to secure a higher income stream for longer, while bond CEFs with short durations will have to buy newer bonds that yield less.

IQI: Our Friend When Markets Get Rough

The Invesco Quality Municipal Income Trust (IQI), for its part, locks in its portfolio’s income stream for even longer, with a weighted average maturity of 19.28 years. On top of that, its focus on higher-rated bonds (that’s what the “quality” in the name refers to) means it has a bit of extra insulation in a major selloff, while offering roughly the same yield as its sister fund, IIM.

IQI uses roughly the same amount of leverage as IIM, at 31.5%. But here again, it benefits from Invesco’s low borrowing costs (which, again, are likely to fall with rates).

KTF’s Long History Offsets Its Narrow Discount

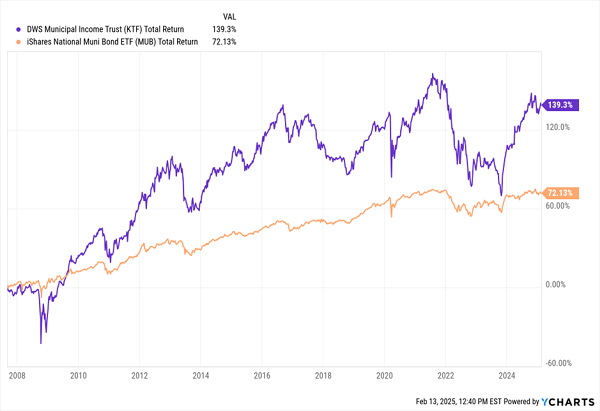

Finally, the DWS Municipal Income Fund (KTF) provides safety in a different way: It has the longest history of our three muni-bond funds, having been launched back in 1988. Since then, it’s piled on a 678% total return, showing why it’s a strong long-term muni-bond holding for just about any investor’s portfolio.

In fact, KTF has been around so long that it predates the iShares National Muni Bond ETF (MUB), the benchmark for the muni-bond space, which was launched nearly 20 years after KTF, in 2007.

Since then, it’s nearly doubled MUB’s total return.

KTF Takes on All Munis, Wins Easily

KTF yields 7.6%, roughly the same as the other two funds here. It also sports an effective maturity of 17.4 years, giving us extra assurance around the dividend. The fund’s 3.2% discount is lower than those of the other two, but still reasonable in light of its long history of outperformance.

That history comes down to its management team, which has shown it knows how to adjust the fund’s portfolio as interest rates shift.

Muni-Bond CEFs: The Ultimate Diversification Play

These three funds offer strong yields and compelling discounts, making them attractive buys for any income investor or, really, anyone looking to diversify beyond stocks.

They’re just the beginning: There are over 100 publicly traded muni-bond CEFs, and many are better deals than these three. That lets us swing into (and out of) the best ones for the market moment, giving us high, stable yields and a level of safety we can’t get by investing in stocks alone.

Buy These 5 Other “Hidden” 9%+ Dividends Now (While They’re Still Cheap!)

Muni-bond funds are just the start. I’ve got 5 other “hidden” CEFs waiting for you that yield a rich 9.4% on average as I write this. And they’re bargains now, which gives us extra protection in the months ahead—and a shot at market-beating upside if stocks unexpectedly jump from here.

Either way, we’ll collect their rich 9.4% payouts.

These 5 payers are “must-owns” as we move into the back half of the 2020s. You do NOT want to miss this rare opportunity to get them cheap. Click here to learn more about these five 9.4% payers and get a free Special Report revealing their names and tickers.