I don’t know why you’d try to cobble together an income stream with miserly ETFs when there are plenty of closed-end funds (CEFs) trading at big discounts, even after the huge market rebound we’ve seen since March.

What’s more, many of these CEFs are throwing off life-changing 7%+ payouts!

Why are we seeing some great deals in CEFs now? Because the folks who invest in these funds tend to be slower to react to events than the jumpy crowd holding the typical S&P 500 stock. That lag gives us a nice opportunity to buy while these funds’ prices are still deeply discounted from the value of the assets in their portfolios (a figure known as the net asset value, or NAV).

These discounts are a quirk of CEFs, and they make our strategy simple: buy when discounts are particularly wide, then ride these markdowns higher as they evaporate—pulling the fund’s market price up with them.

Let’s go through two areas that should have a place in any income seeker’s portfolio: corporate bonds and municipal bonds. As we do, we’ll hit on two low-paying ETFs to avoid—and two discounted, high-paying CEFs that are much better options.

Corporate Bonds: CEFs Are a No-Brainer

You may have heard the old excuse for picking passive funds over actively managed ones: that few active managers beat their indexes, so why pay the extra fees?

To be honest, there’s a grain of truth here—but it mainly relates to stocks. In other corners of the market, human managers beat the algorithms on the regular.

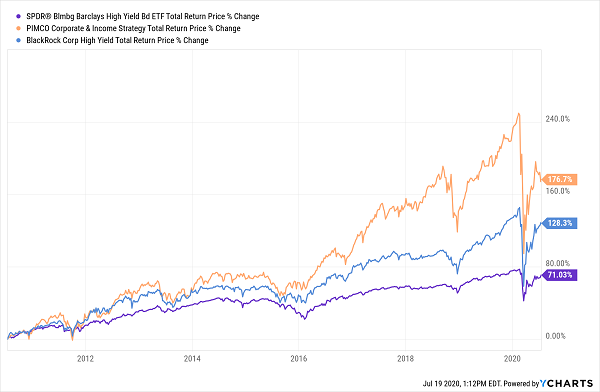

One place where this happens all the time is in corporate bonds. Consider the high-yield bond ETF most people know about: the SPDR Bloomberg Barclays High-Yield Bond ETF (JNK).

A simple screen reveals that JNK has been handily beaten by two other actively managed bond CEFs, the PIMCO Corporate & Income Strategy Fund (PCN)—in orange below—and the BlackRock Corporate High-Yield Fund (HYT), in blue, in the last decade:

CEFs: 1, ETFs: 0

Why? Because PCN and HYT are run by PIMCO and BlackRock, respectively, two giants of the investment world, managing $1.9 trillion and $7 trillion of assets.

That unthinkable amount of cash gets the kind of first-mover advantage you and I can only dream about: when companies issue new bonds, the first calls go to PIMCO and BlackRock. That’s a key difference from stocks, where IPOs are available to a much wider group.

What’s more, you’re getting most of your return in cash from these two CEFs, with both yielding around 9%, far higher than the 5.9% you’d get from JNK.

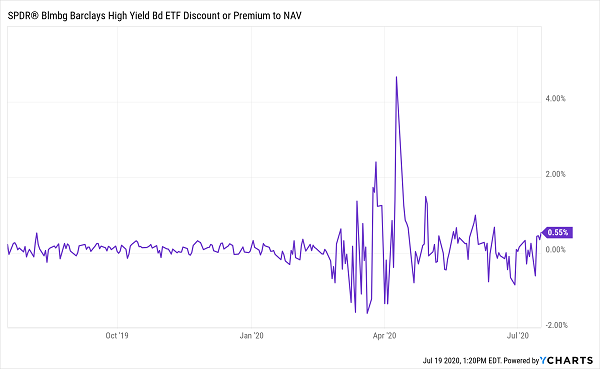

So which of these two bond CEFs is the better buy? Definitely HYT, due to its 6% discount to NAV. PCN, for its part, trades at a whopping 22% premium to NAV. (Big premiums are common for PIMCO funds, as the company is seen as a boutique brand among CEF investors—so much so that they’ll fork over $1.22 for every dollar of assets!)

JNK? It’s always priced to perfection—apart from a quick disconnect during the worst of the selloff, it’s always priced to within 1% of its portfolio value:

JNK: No Deal Here

Municipal Bonds: A “Stealth” Dividend With Upside

Another place the “active managers never beat the index” nonsense is disproven is with municipal bonds, or “munis.” If you got burned a few weeks ago, on Tax Day, you might consider “swapping out” some of your blue-chip dividends for muni-bond CEFs, as these funds’ dividends are tax-free for most Americans.

That tax-free edge is why I often refer to muni bonds as “stealth dividends.” Look up any muni-bond CEF on a fund screener and you’ll likely see a yield in the 4% neighborhood, but that could easily translate to 7% or more for you, depending on your tax bracket.

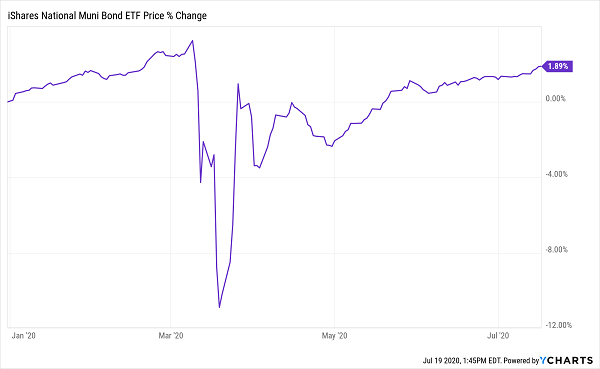

Before we go further, let’s stop and address a worry you might have about muni bonds—that they’ll default as the coronavirus hits city and state tax revenues.

That was a big concern in March, when the “muni” benchmark iShares National Muni Bond ETF (MUB) plunged 14% in just 10 days. That’s a massive dive for steady assets like munis:

Munis Crumble—Then Get an Assist From the Fed

As you can see above, munis then bounced back fast—even faster than stocks. That’s because the Fed rode to the rescue, pledging to buy munis and keep the market liquid no matter what.

That’s about the strongest insurance you can get against another pullback—and with munis still off their March highs, you’ve got a shot at some upside here, too.

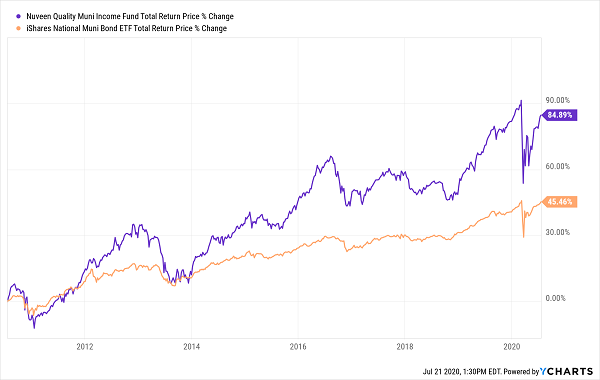

This is where our CEF option comes in, because many of the top muni CEFs crush MUB. That includes the Nuveen Quality Municipal Income Fund (NAD), which holds 1,184 different municipal bonds, including issues used to fund infrastructure in Denver, Ohio and Salt Lake City. NAD has nearly doubled up the benchmark ETF’s return in the last decade:

NAD Easily Outruns the Index

The fund’s dividend also doubles that of the benchmark, yielding 4.6% (without accounting for its tax advantages), compared to MUB’s 2.2%. There’s more upside ahead, too, thanks to the nice discount we get on NAD: 9.2% as I write this.

5 “Pullback-Proof” Dividends Paying Up to 13% (Buy Now)

In a levitating market like this one, my best advice is this: buy the 5 “pullback-proof” stocks I’m recommending now.

These 5 are trading at even more attractive discounts than the CEFs I just mentioned, and they yield an incredible 9.4%, on average. The highest payer of the bunch throws off a massive 13% payout!

Think about that: with nearly 13% of your initial buy boomeranging back to you every year in dividend cash, this pick gives you a built-in “shock absorber” to protect you in a downturn.

If you hold on for just 6 years, you’ll have recouped all of your investment in dividend income alone. At that point, you can ignore the stock price because everything you bring in—in price gains or dividends—is gravy!

That’s the very definition of safety, and I can’t wait to share these 5 cash-rich dividend-payers with you, along with my complete strategy for surviving—and thriving—in a market storm.

Don’t deny yourself the peace of mind (and high income) you need in these uncertain times. Click here and I’ll give you my full safe-investing plan and everything I have on these 5 “pullback-proof” dividends: names, tickers, buy-under prices, dividend histories and a full rundown of their downturn-resistant businesses.