Fee-obsessed investors continue to pile into exchange-traded funds (ETFs).

Don’t follow them.

Because there’s another—much less popular—group of funds that will hand you much better returns (and double the dividend payouts). And swapping your ETFs for them is easy.

I’m talking about closed-end funds (CEFs). (If you’re not familiar with CEFs, click here to check out a primer I recently wrote on them.)

Now even though I just said CEFs are less popular than ETFs, that doesn’t mean they’re totally ignored. The truth is, they’re getting more attention from investors of late, for reasons I’ll dive into in just a moment.

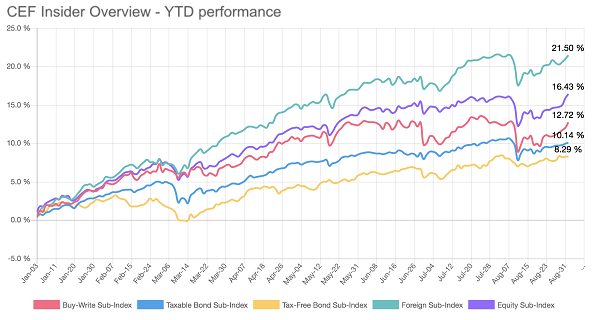

First, let’s look at how the five main sectors of the CEF market, which I track in my CEF Insider service, are performing this year:

With average gains of 13.8%, there’s no doubt CEFs are soaring.

And they’re doing it with incredible diversification—almost all CEFs hold more than 100 investments, including stocks, bonds and even real estate. That gives them more protection from a market downturn than you get with ETFs, which partly explains why investors are taking notice.

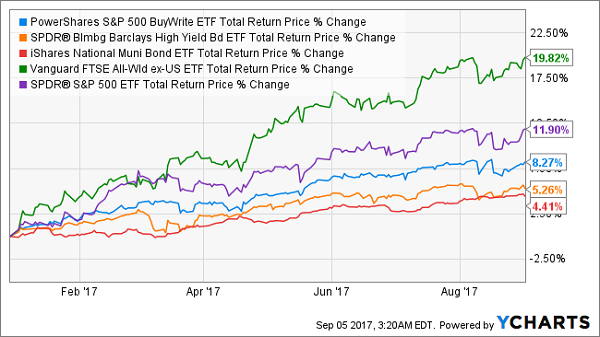

But the real reason CEFs are moving into the limelight is simpler than that: they’re destroying their ETF cousins. Compare five ETFs investing in similar asset classes as the 5 indexes above:

ETFs Are Doing Okay—But Not Great

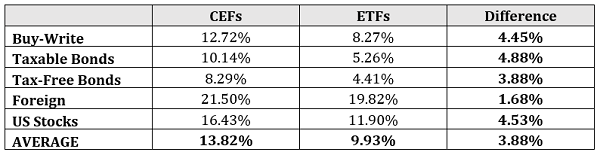

With average returns of 9.9%, these funds are falling well short of their CEF counterparts. To give you a better sense, I’ve placed the CEF indexes and the comparable ETFs side by side in this table:

The Income Factor

Superior returns aren’t the only reason investors should prefer CEFs, however.

Let’s talk about dividends.

The average yield of the 5 ETFs above is just 3.13%; buy $500,000 of these funds and you’ll end up with $1,304 per month in income. Meanwhile, the average yield of the 500+ CEFs actively tracked by CEF Insider is 6.32%—more than double what these ETFs are paying!

Plus, some of the best CEFs (like the 4 I’ll tell you about at the very end of this article) are paying even higher dividends of 7.4% or more. In other words, $500,000 in these CEFs gets you $3,125 in monthly income (or $37,000+ annually). Instead of a below-poverty dividend stream from ETFs, we’re talking about serious cash retirees can live on!

Superior returns and higher dividend yields are two big reasons why CEFs are getting attention these days, but there’s more to the story. Much more.

Unbeatable Discounts

ETFs almost always trade at a price that’s pretty close to their net asset value (NAV, or the value of their underlying assets). For instance, take a look at the market price and NAV SPDR S&P 500 ETF (SPY) over the last year:

Where’s the Blue Line?

You can’t even see the blue line here because the two are virtually identical! As I write, SPY’s discount to its NAV is 0.05%—so pretty much nothing.

Now let’s compare that to the Liberty All-Star Equity Fund (USA), which invests in a variety of mid-cap and large-cap stocks, most of which are S&P 500 names:

There’s the Blue Line!

There are two important points here.

First, when the market price is lower than the NAV, we’re getting these stocks at a discount. It’s like buying $10,000 worth of Apple (AAPL) and Microsoft (MSFT) for $8,780. With ETFs, it’s impossible—with CEFs, it’s easy to do.

Second, notice how that blue line goes above the orange one every once in a while? That’s the beauty of CEFs—while you’re collecting a huge income stream (USA pays a 9.1% dividend), you can also sit back until the fund gets overbought (meaning the discount snaps shut, or better, turns into a premium), then sell for a tidy profit.

Again, impossible with ETFs.

Easy Come, Easy Go

Just like ETFs, CEFs trade during normal market hours, just like stocks, and the growing demand for CEFs means they’ve become much more liquid.

That’s a big advantage when you invest in a CEF that buys municipal bonds, high-yield corporate bonds or other investments—the kinds of assets that you couldn’t easily buy and sell without dealing with an expensive broker.

And because these individual investments generally see less trading volume than most stocks, buying them on your own means you could wait a long time for your cash when you want to sell (unless you lower your price). A highly liquid CEF solves that problem.

Experienced—and Connected—Management

One of the big issues with non-stock ETFs, especially those that trade in areas like junk bonds or foreign debt, is that it’s tough for regular investors to find the highest-quality assets on the market.

For instance, consider the SPDR Barclays High-Yield Bond ETF (JNK). During the 2014 oil crash, defaults among small cap energy companies skyrocketed—but JNK couldn’t sell junk bonds issued by those companies because it’s an index fund. Avoiding those bonds would be active management, against the rules of the fund!

CEFs, however, could stay away. That’s why high-yield CEFs like the Dreyfus High Yield Strategies Fund (DHF) have beaten the performance of JNK from the start of the oil crash till now, even though they invest in the same kinds of bonds:

The Power of Having a Pro at the Helm

Keep in mind DHF isn’t the best high-yield CEF—others out there have doubled JNK’s performance over the last 5 years!

Of course, avoiding oil was just part of that superior return. Many CEFs have very highly qualified management and are run by fund companies with deep connections to the companies whose debt their funds hold. That means they often get “first look” access to newly issued debts before any of us mere mortals get a chance. You simply can’t get that kind of inside knowledge with ETFs.

4 Quick CEF Buys for 7.4% Dividends and 20% Upside

As I mentioned earlier, I’ve found 4 CEFs that will hand you a steady 7.4% average dividend yield—starting today!

PLUS they’re trading at completely ridiculous discounts to NAV, too.

The upshot?

Throw these 4 dividend studs together in their own “mini-portfolio” and get ready for retirement-ready income NOW (I’m talking an easy $37,000 a year on a $500,000 nest egg) AND 20% price upside in the next 12 months!

Why 20%?

Because all 4 of these funds are trading at absurd discounts to NAV, and as I just showed you, there’s no better indicator of big gains ahead. But with the increased attention CEFs are getting these days, I don’t expect these screaming deals to last long. You must make your move now!

To make sure you get in before these ridiculous discounts start to close, I’ve rushed out a new FREE report that gives you all the details on these 4 dividend powerhouses.

Your copy is waiting for you. All you have to do is CLICK HERE to get immediate access and discover all the details on these 4 income wonders.