When you invest for the long haul, dividend stocks and exchange-traded funds (ETFs) are going to be the bedrock of your portfolio.

The idea is simple: The slow crawl higher of the market over time, plus a few percentage points of return each year in income, will be enough to push your nest egg to that magic number you need to enjoy a comfortable retirement.

Just a couple of problems with that, though.

The age-old adage is that you can expect about 7% annual returns from the stock market, and when investors plan for the future, that’s the number they plug into their calculations. But Bill Gross and other experts predicting lower-than normal returns of 3%-4% for bonds and 4%-5% for stocks. Barry Ritholtz observes that individual investors typically underperform to the tune of 3.7% because they tend to chase alpha.

And yes, you might think a 3% yield in perpetuity is just fine, but do you remember our old friend, inflation? You might not, considering annual U.S. inflation has been below 2% since 2012, but even that cuts into the reality of your returns.

That, my friends, is why dividend growth is just as important as dividend yield – and why you’re shooting yourself in the foot if you’re not examining dividend growth any time you pull the trigger on an income investment.

With that in mind, we’re going to look at three great dividend growth ETFs focused on companies that regularly write bigger checks out to investors, and thus give you an edge as you make your way to retirement.

Vanguard Does Everything Low-Cost – Even Dividend Growth!

The Vanguard Dividend Appreciation ETF (VIG) is the exchange-traded version of its popular Vanguard Dividend Appreciation Index Fund (VDIAX), and focuses on high-quality dividend stocks that increase their payouts on a regular basis.

The VIG tracks the Nasdaq US Dividend Achievers Select Index, which is comprised of companies that have increased their dividends on an annual basis for at least 10 straight years. This includes popular Dividend Aristocrats (25-plus years of growth) like Johnson & Johnson (JNJ) and PepsiCo (PEP), but because of the lower 10-year bar, also “newer” dividend payers like spry tech titan Microsoft (MSFT).

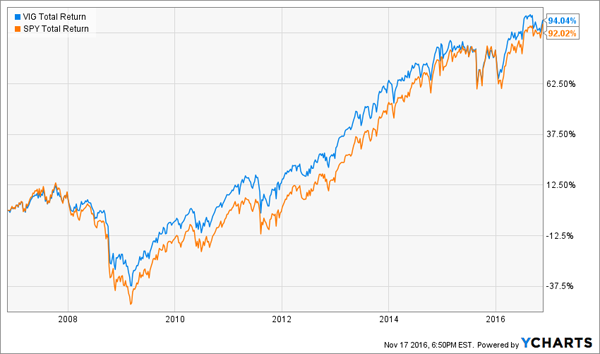

Vanguard Dividend Appreciation’s yield wouldn’t even impress a bond investor right now; at 2.1%, it’s only basis points better than the S&P 500. But the important thing to remember about VIG or any dividend growth investment is yield on cost. The idea is that over time, as the dividend payments of VIG’s holdings go up, so will VIG’s overall payments, and thus the yield on your original purchase.

Here’s an example. Let’s say you bought into VIG at the start of 2007 at around $54. Based on the 72.58 cents it paid out, you enjoyed a yield of just 1.3% that year. However, in 2015, you would be sitting on a yield of well more than double that – 3.4% — based on its $1.85 in annual dividends. (Not to mention about 56% in capital gains since then.)

The result?

Yes, even then, 3.4% isn’t a screamingly high yield. But through its focus on companies with bulletproof financials, VIG since inception has done something a lot of funds can’t say over time – it has beaten the market. And at a mere 0.09% in annual expenses, it’s almost as cheap as buying “the market.”

Dividend Growth … And Growth Growth!

The WisdomTree U.S. Quality Dividend Growth Fund (DGRW) is another way to skin the dividend growth cat, putting emphasis not just on a track record of improving payouts, but also actual growth characteristics to boot.

In short, DGRW wants you to have your cake and eat it, too – and it does so by throwing convention out the window.

Rather than look at any history of consecutive dividend increases, DGRW instead looks at other factors to determine what stocks will be most capable of significant dividend (and price) growth. So its screens include long-term earnings growth expectations, as well as three-year average return on assets and return on equity.

The result is exactly what you’d expect – a portfolio that looks a little younger and growth-oriented … at least compared to most other dividend growth ETFs. Apple (AAPL), for instance, is a top-five holding, and even biotech Amgen (AMGN) is part of the portfolio.

DGRW is much younger than VIG, with an inception date of May 22, 2013, but so far, it too is beating the S&P 500 on a total-return basis. And fees are modest at 0.28%.

Don’t Forget International Dividends

No portfolio would be complete without exposure outside of the U.S., which is why investors should consider giving the fresh-faced iShares International Dividend Growth ETF (IGRO) a ride.

IGRO was brought to market only a few months ago, on May 17, 2016, so there’s little performance data to evaluate. So for this one, we’ll just look at the innards.

IGRO is in the same vein as its U.S.-based brother, iShares Core Dividend Growth ETF (DGRO), which focuses on financial health and, of course, increasing dividends. DGRO selects non-real estate investment trust securities that are outside of the U.S. and pass a number of quality screens, including five years of consecutive annual dividend growth, a payout ratio of less than 75% and a positive consensus earnings forecast.

That results in a portfolio that puts about a quarter of its weight in financials, 17% in consumer staples, 14% in healthcare and double-digit exposure in consumer discretionary and industrials, too. Top holdings are a mishmash of no-doubt blue chips like French pharma outfit Sanofi SA (SNY) and Swiss foods multinational Nestle SA (NSRGY), as well as big dividend-paying financials like Australia’s Westpac Banking Corp (WBK).

It’s the same recipe that other dividend growth ETFs use to achieve success, so I expect nothing less out of IGRO.

What I like about each of these ETFs is they give you a great chance of matching – if not beating – the market. And the dividend growth potential itself is good.

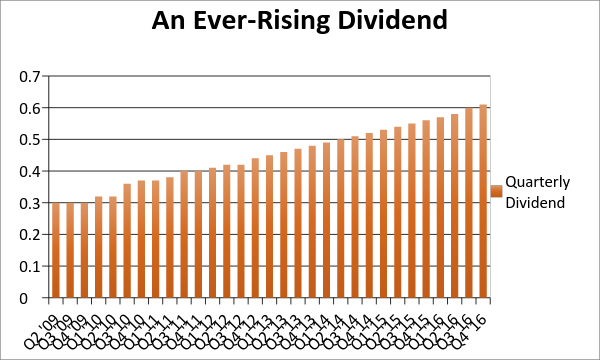

Or, Bank This 8.5% Yield With 20% Upside

My favorite dividend grower today pays an amazing 8.5% current yield, and it raises its dividend every single quarter:

Add in this annual dividend growth of 8-9%, and you’re looking at 17% total returns from this recession-proof business. With about half of that coming as cash in your pocket.

Secure 8%+ income streams like these will help you stretch a nest egg as modest as $500,000 and make it last forever. Every half-million bucks should generate $40,000 or better annually, with some price upside as discount windows close.

Of course you’ll need to diversify your nest egg into other rate-hike and recession proof income streams. You won’t read about these vehicles often in the mainstream financial media, because most financial advisors and even money managers don’t know about them.

But I specialize in uncovering contrarian 8%+ income opportunities like these. Click here and I’ll explain more about my strategy and my favorite stocks and funds to buy for a secure retirement on $500,000.