When C-level types lay down five, six, even seven figures to scoop up shares, we listen.

After all, there is only one reason why executives buy their own stock. They believe the price is going up.

Insider buying is a great cue. But it is important for us to understand what “signal” buys look like.

Many executives have automatic buying programs, so like clockwork, we’ll see them snap up a few thousand shares at, say, the start of every quarter.

So what we really care about are sudden acquisitions across one or more insiders that fall well outside of their normal buying habits.

These are the kind of insider purchases I want to share today.

I have my eye on insider buys across four of Wall Street’s top dividend payers—companies throwing off anywhere between 5.4% and 9.9% on an annual basis. The simple fact that they’re intentionally buying is reason enough to take a closer look—but the fact that they’re doing it amid a lot of Wall Street uncertainty makes them extremely interesting right now.

Northern Oil & Gas (NOG)

Dividend Yield: 6.0%

Recent Noteworthy Buys:

- Chief Executive Officer Nicholas O’Grady: 1,500 shares ($42,885) on 3/3/25

- Director Stuart Lasher: 20,000 shares ($552,400) on 3/4/25

- Chairman of the Board Bahram Akradi: 40,000 shares ($1,121,200) on 3/4/25

- Chief Executive Officer Nicholas O’Grady: 1,000 shares ($27,480) on 3/7/25

Minnesota-based Northern Oil and Gas (NOG) is an energy exploration and production company that owns some 300,000 acres of land across the Williston, Permian, Uinta and Appalachia basins. And it relies upon more than 100 public and private operators to extract oil and natural gas from those properties.

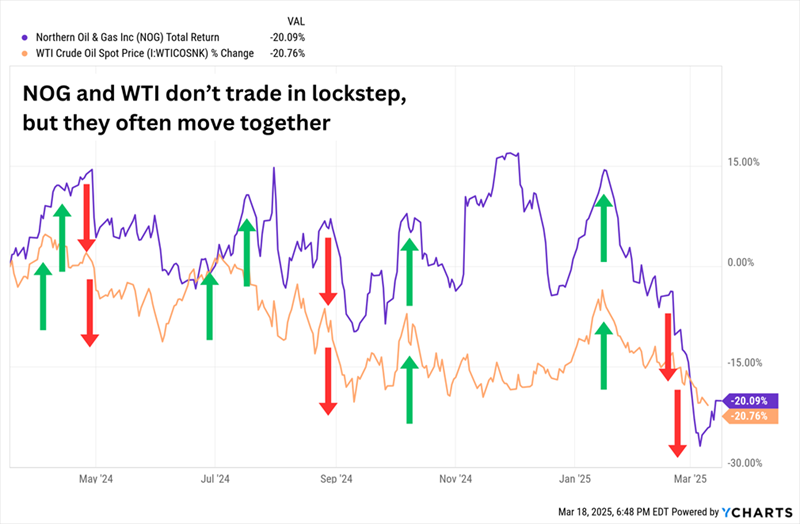

Northern Oil and Gas tends to be an exaggerated play on the energy sector—just look at the direction West Texas Intermediate (WTI) crude is heading, and chances are NOG is sprinting even faster in the same direction.

The Problem: Right Now, Northern Oil & Gas Is Sprinting Through a Slump

Still, the fact that NOG is off by nearly a third since early December seems a bit extreme given a lack of red-flag headlines. The company’s Q3 results, released in November, beat expectations—Q4, reported in March, didn’t, but shares have rebounded softly since then. Wall Street also didn’t flinch later in December amid reports that it was trying to acquire Granite Ridge Resources (GRNT).

It’s possible that investors have gone overboard in its selling, which might explain why several Northern Oil and Gas executives snapped up shares right around its early March earnings announcement. Bahram Akradi, NOG’s board chair, bought more than $1.1 million worth of shares, while another director spent more than half a million, and its CEO bought around $70,000 worth.

At the very least, they’re getting paid well to hold those shares. Northern Oil and Gas has a fairly young dividend program that started in 2021. It paid 3 cents a share then, and 45 cents today—for a comically tall 1,400% jump. That payout is still extremely well covered at roughly 40% of profits.

NOG has done a good job of growing both organically and through acquisitions, which has resulted in substantial outperformance over the past few years. The recent swoon, while painful for current shareholders, has driven the headline yield up to 6% and has driven valuations down—NOG trades for 7 times earnings estimates and at a low price/earnings-to-growth (PEG) ratio of 0.56 (anything below 1 is considered to be undervalued).

Sinclair (SBGI)

Dividend Yield: 6.3%

Recent Noteworthy Buys:

- Executive Chairman, Former CEO David Smith: 38,410 shares ($538,124) on 3/3/25

- Executive Chairman, Former CEO David Smith: 53,126 shares ($729,419) on 3/4/25

- Executive Chairman, Former CEO David Smith: 30,296 shares ($426,870) on 3/5/25

- Executive Chairman, Former CEO David Smith: 22,752 shares ($324,898) on 3/6/25

- Executive Chairman, Former CEO David Smith: 67,131 shares ($937,148) on 3/10/25

- Executive Chairman, Former CEO David Smith: 39,896 shares ($556,150) on 3/11/25

- Executive Chairman, Former CEO David Smith: 42,595 shares ($599,737) on 3/12/25

Sinclair (SBGI), better known to some as Sinclair Broadcast Group, owns 185 owned or operated TV stations in 86 markets, as well as the Tennis Channel cable network.

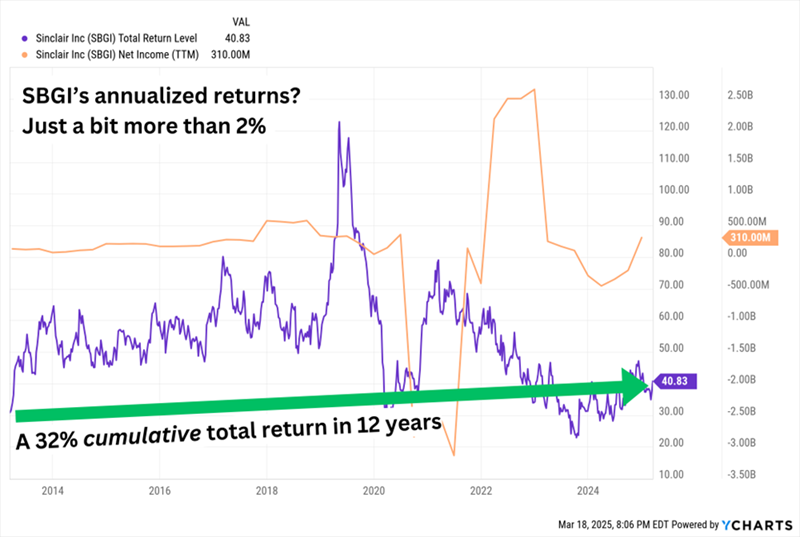

Sinclair has been dead money for more than a decade, with the exception of one short-lived pop in 2019. No surprise there. Americans are increasingly moving away from traditional television and toward streaming services, which leaves local TV on the outside looking in. Tennis viewership in the U.S. has been in a multi-decade decline, as well—the 2025 Australian Open, for instance, saw an 11% decline year-over-year despite American Madison Keys’ run to the title.

Despite a Generous Dividend, SBGI Shares Aren’t Even Keeping Up With Inflation

None of that has stopped current Executive Chairman and former CEO David Smith from buying with both hands. In March, he spent more than $4 million adding to his pile of SBGI shares, which grew by about 50% in number—he now owns 900,000 shares worth $14.4 million.

Smith bought into a short-term dip that has SBGI shares throwing off more than 6% in yield. Past that, though, it’s hard to see the appeal. The company’s top and bottom lines are expected to retreat in 2025 following heavy campaign-ad spending last year. The stock isn’t particularly cheap, at 22 times earnings estimates. And there are few catalysts on the horizon.

Ready Capital (RC)

Dividend Yield: 9.9%

Recent Noteworthy Buys:

- President Jack Ross: 5,000 shares ($24,250) on 3/5/25

- Chief Executive Officer Thomas Capasse: 10,000 shares ($48,000) on 3/5/25

- Chief Executive Officer Thomas Capasse: 90,000 shares ($449,100) on 3/6/25

- Chief Credit Officer Adam Zausmer: 10,000 shares ($54,200) on 3/7/25

- Chief Operating Officer Gary Taylor: 10,000 shares ($52,300) on 3/10/25

- Director Nathan Gilbert: 5,000 shares ($25,600) on 3/10/25

- Chief Financial Officer Andrew Ahlborn: 10,000 shares ($50,400) on 3/12/25

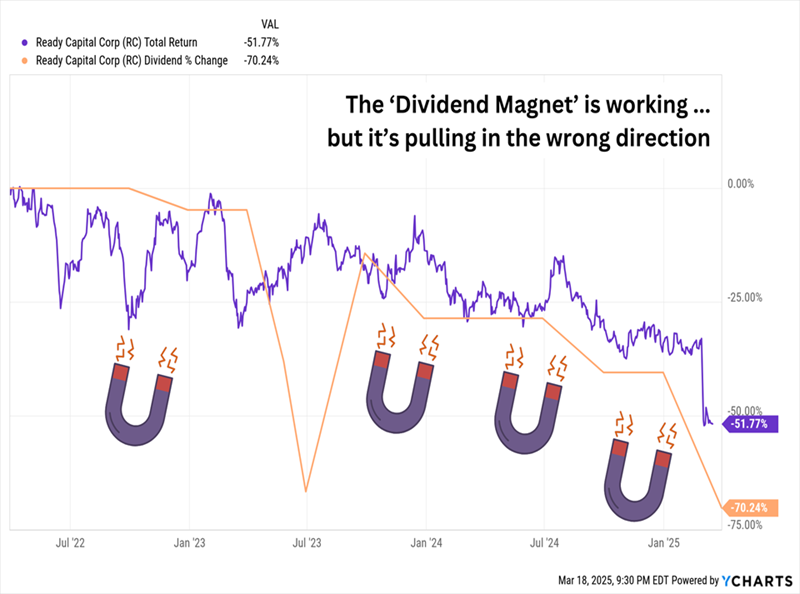

Speaking of dip-buying, a whole squad of Ready Capital (RC) C-suiters has pounced on the stock’s recent post-earnings dive.

Ready Capital is a mortgage real estate investment trust (mREIT) that originates, acquires, finances and services small- and medium-sized balance commercial loans. A little more than 60% of its distributable earnings come from lower-middle-market loans, which includes construction, bridge, fixed-rate commercial mortgage-backed securities (CMBSs) and Freddie Mac loans; the rest comes from government-backed small business and USDA loans.

I mentioned a few months ago that the company had been cycling out of underperforming loans and into higher-yielding opportunities, and dumping its mortgage-servicing-rights (MSR) business while leaning into its small business lending platform—but that “an eventual rebound could take some time.”

Well, it might need a bit longer.

RC Falls Off a Cliff After Another Dividend Cut

Why did shares fall off a cliff? In early March, Ready Capital announced downright dreadful Q4 results. The pros were looking for 19 cents in distributable earnings; RC lost 3 cents. Book value declined by nearly 16%. Portfolio credit quality improved but still remains worse than several peers. And RC announced it would cut the dividend in half, marking a 70% decline in payouts over the past three years.

Management swooped in to support the stock, with six different executives combining to spend more than $700,000 on shares within about a week of Ready’s disappointing report. And they’ll collect nearly 10% annually even after the massive gut-shot to the dividend.

But at least for right now, that might be RC’s only appeal.

NETSTREIT (NTST)

Dividend Yield: 5.4%

Recent Noteworthy Buys:

- Chief Financial Officer Daniel Donlan: 1,000 shares ($15,000) on 3/3/25

- Chief Executive Officer Mark Manheimer: 3,616 shares ($54,818) on 3/7/25

- Chief Financial Officer Daniel Donlan: 1,000 shares ($15,270) on 3/10/25

- Chief Executive Officer Mark Manheimer: 6,384 shares ($97,419) on 3/10/25

- Chief Executive Officer Mark Manheimer: 2,500 shares ($37,175) on 3/11/25

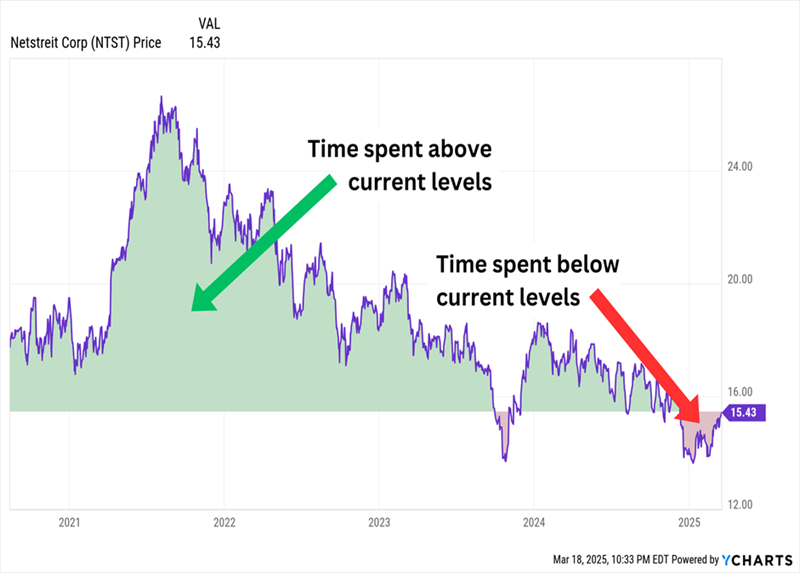

It’s hard not to swell with confidence when we see insiders buying an upswing in their stock.

That’s what we’ve seen at NETSTREIT (NTST), a retail REIT that specializes in single-tenant net-lease deals. NTST breaks its retail properties into four categories, three of which involve heavily defensive tenants (percentages shown are % of annualized base rent):

Source: NETSTREIT February 2025 Investor Presentation

What the above doesn’t show is that NETSTREIT is working on “right-sizing” exposure to some of its most outsized tenants, including Walgreens (WBA), Dollar General (DG), CVS (CVS), and Dollar Tree (DLTR). Specifically, it’s trying to get all tenants to below 5% of ABR by the end of 2025.

Meanwhile, net investment activity guidance was on the light side, and adjusted funds from operations (AFFO) guidance implies low-single-digit growth. In short: 2025 isn’t setting up as a boom year, but instead a “get our ducks in a row year”—hopefully one it can eventually build upon.

NETSTREIT’S CEO and CFO took turns buying in March while shares were rapidly bouncing off the bottom. Given that the stock still trades near the lower end of its five-year range, they might very well be buying a relative low.

From a Pure Price Perspective, NTST Is Rarely This Cheap

The 5%-plus yield isn’t as glamorous as the other names mentioned here, but it’s exceedingly well-covered, at just 65% of AFFO guidance.

This 11% Dividend Is an URGENT Trump 2.0 Buy

As far as high yields go, I’m keeping one eye on these insider buys … but my other eye is fixated on a massive income opportunity.

Our target: A closed-end fund (CEF)—this one kicking out a monster 11% dividend yield that’s double what you can get from NETSTREIT.

This isn’t some vanilla index fund. This CEF is actively run by a manager who’s at the top of the bond world. He has been named Fixed Income Manager of the Year by Morningstar, and he has been inducted into the Fixed Income Analysts Society Hall of Fame!

And if that’s not enticing enough, this overlooked income giant pays its distributions each and every month.

My “buy window” for this fund is closing, however, so the time to act is now. Click here to learn more about this monster 11% dividend and get on the list to receive its next payout, which is just weeks away.