Just three weeks ago, we discussed the likelihood that the stock market was going to be a mess this year.

It’s already a train wreck.

You’re probably wondering whether you should buy more shares of your favorite dividend. Well, if you’re sick of wondering, use this simple yet effective “market timing” technique.

Dollar cost averaging (DCA) probably helped you build your impressive retirement portfolio. And DCA is more than just an initial fortune builder. It can also build wealth and income streams during train wreck markets like these.

It was the regular weekly, monthly and/or yearly purchases throughout your earning years that helped you buy more shares of stock low (and buy fewer shares higher). This technique can still work today, even if you’re retired or nearing retirement. DCA ain’t just for building fortunes—it can provide sanity during manic moves.

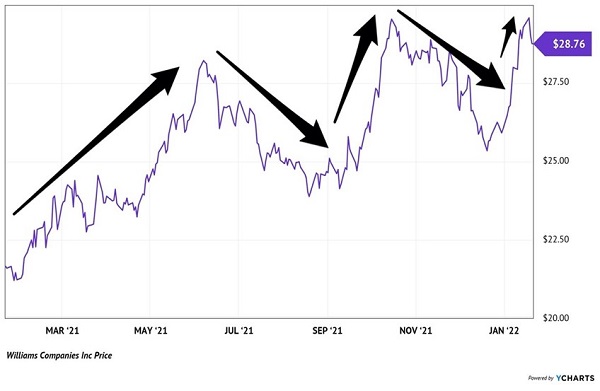

Let’s take The Williams Companies (WMB). WMB moves energy (mostly natural gas) from here to there with its network of pipelines. It’s the type of toll booth that we income investors like to own, because the stock usually yields 6% to 7% or more and its dividends are secured by good old-fashioned profits.

WMB has already built out its infrastructure. Management still invests some money in growth projects, but most of its cash flows are ours in the form of a regular (and growing!) dividend.

Surprisingly, this stock price moves more than you think. Natural gas goes up, and WMB pops. Natural gas eases off multiyear highs, and WMB slumps. Check out these wild price swings:

Big Swings for a Secure Dividend

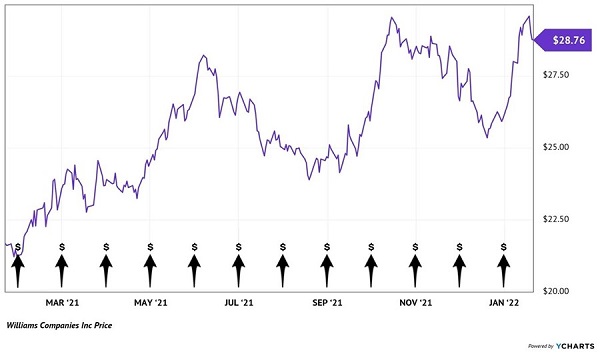

The big winners from this price volatility were the investors who DCA’d themselves WMB. Let’s take an investor, “Jane Income,” who bought $1,000 in WMB on the first of every month starting twelve months ago:

A DCA Dividend Approach

Last February, Jane was able to secure 46.9 shares for an average yield of 7.5%. Shares of WMB were low, so she was able to buy more shares—and dividends!—from her thousand dollars.

Fast forward to June, and natural gas prices were going on a “mini moonshot.” Jane made her purchase anyway, and only netted 37.2 shares for an average yield of 6%.

Jane didn’t have to think about market timing. Her methodical DCA approach kept her cool when prices were running hot.

They also kept her ahead of her neighbor’s son, “Degenerate Johnny.” Ah, poor DJ. Rather than buy dividend payers in 2021, DJ was busy buying crypto coins with dogs on the cover.

When the crypto market completely fell out of bed last Friday, DJ decided enough was enough. He sold his doggy coins and, in a moment of maturity, moved his remaining $12,000 over to reliable WMB.

DJ was able to buy 417 shares for an average yield of 5.7%. He might now finish 2022 all right, after all. His crypto coin has gone to money heaven but if he keeps this up, we may eventually upgrade his nickname to “Dividend Johnny.”

But he has more to learn from Jane. She invested the same amount of cash and has nearly 475 shares in WMB to show for it. She is also enjoying an average yield of 6.5%.

DJ is on the mend, but Jane is 14% richer with 14% more income coming from the exact same investment.

DCA can be a powerful strategy, especially in these manic markets. Don’t forget about it! After all, DCA is probably the reason you have enough capital to make articles like these worth reading.

Dynamic dividends like WMB are the lifeblood of my “No Withdrawal” Retirement Portfolio. With payouts like these, we can live on dividends alone and never have to sell any shares.

Most “basic” investors retire and immediately begin to reverse DCA their portfolio. They withdraw 4% per year or so for living expenses.

Why? This is the opposite of wealth building. By selling a set percentage every month or year, they are selling more shares when prices are low.

Don’t fall for a withdrawal rule. “No Withdrawal” is what got you here. Let it see you all the way through your retirement.

(For my favorite 7%+ No Withdrawal Dividends to buy today, please click here and I’ll share my full retirement research.)