The 2022 edition of the stock market is probably going to be a mess. With the Federal Reserve pausing its money printing, we are likely to see “flights to safety” that will feature—believe it or not—our favorite dividend stocks.

Yes, it’s all fun and games in the tech-and-crypto casino when the Fed is pumping billions into the bond market every month. Its purchases, of course, were funded by money that the Fed itself printed out of thin air. This capital flowed into speculative assets like the NASDAQ in 2020 and coins with dog faces in 2021.

The trendy stocks of 2022 are likely to be our style. As vanilla investors leave the betting tables, some of the more sober participants are likely to focus on quality and cash flows, of all things.

What a nice contrast it will be for us contrarian income investors! The reliable retirement investments we’ve been buying all along are likely to become quite popular.

Of course, the basic types will talk about dividend stocks as if they are all created equal. They are not. As with any equity, the economic backdrop and business model matter.

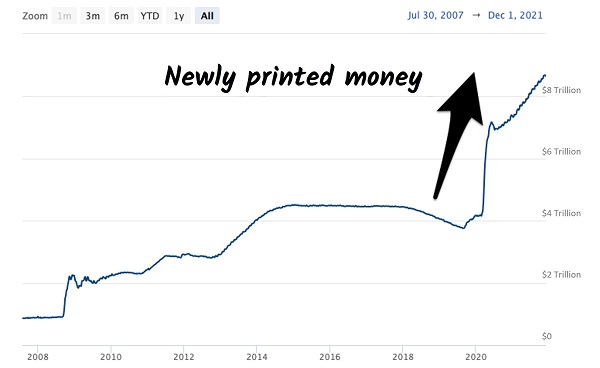

This time last year, the Fed was “buying” $120 billion in bonds every month. (Again “bond buying” is a polite way of saying “money creation.” Chairman Jay Powell has been a prolific printer of greenbacks .)

We can see this reflected on the Fed’s ballooning balance sheet. Chairman Jay Powell piled the central bank’s balance sheet higher by a cool $4.5 trillion—more than a 100% increase since the start of 2020:

Trillions in New Money

Source: FederalReserve.gov

While Powell was literally minting money, he likewise had short-term interest rates glued to the floor. He pledged to keep them there through 2021. Which he did. Powell also helped prop up the economy with massive liquidity while engineering higher inflation (which meant higher long-term rates).

Meanwhile, by keeping short-term rates low, firms that “borrow short” saw their bottom lines boom as the spread between their borrowing costs and lending profits popped.

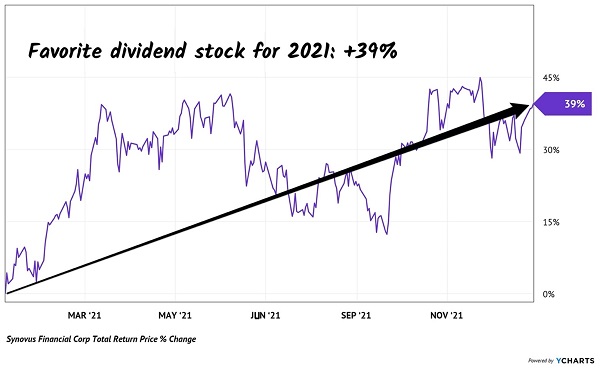

In relative terms, it was a huge windfall. Which is why, in this exact column one year ago, we discussed Synovus Financial (SNV) as my favorite dividend stock for 2021. Since that column, SNV soared 39% (including dividends):

Synovus Soared 39% in 2021

Congratulations if you saw the upside in SNV and enjoyed these 39% gains. And very well done if you bought SNV even earlier—say on our April 2020 recommendation in Contrarian Income Report. If so, you are sitting on 178% total returns (and counting).

But can we count on another rocket ride from SNV in 2022? I’m not so sure. The general bank backdrop looks quite a bit different now than it did 12 months ago:

- The Fed is being forced to kick its money-printing habit.

- Short-term rates are likely to rise in ’22.

- Long-term rates, meanwhile, have stalled.

The potential implications here are compressed profits for banks like SNV. Now don’t get me wrong, I’m not worried about its dividend. But we need to recognize that a repeat of SNV’s 2021 and late 2020 moonshots is unlikely.

Number three above—the upside of long-term rates—is the potential wildcard and the reason we’re not bailing on our bank positions yet. Powell has been buying bonds with other people’s money (specifically ours), so he didn’t care about the price he was paying (or interest rate he was receiving).

The Chairman is the reason the 10-year Treasury yield ended 2021 impossibly low given the high level of inflation, around just 1.5%. But now that he is fleeing the market, new buyers must step in.

These new bond shoppers will care more about prices and yields than Powell did. Their discretion may put pressure on the “long end” of the yield curve and protect bank spreads.

Bank stocks aren’t the layup they were this time last year. Fortunately, I have the perfect income ideas for 2022. They are set to soar even if we see another wave of the virus, crash of the market or another lockdown. I’m talking about boosting your investment income by 400% or more in 2022, with much less risk than the broader stock market.