Money market accounts still offer 5%, but these rates won’t last. Short-term yields are dropping, fast.

With the “safe 5% party” ending, you and I should skedaddle to the “11% yield afterparty” now. Fear not, my fellow contrarian—I have an extra dividend VIP pass for you.

Fed Chair Jay Powell’s tenure is in the homestretch. Whether or not ol’ Jay makes it to the finish or gets hauled off prematurely, the Chair is a lame duck as far as the markets are concerned.

Traders are pricing in two Fed cuts over the next nine months. Meanwhile, the industry projects money market rates to plummet to 3.8% by year end, with the 2-year Treasury yield also trending down, currently at 3.9%.

Given President Trump’s preference for lower rates, aggressive rate cuts are around the corner. Fed independence? Nah. Trump’s appointed chair will cut, cut and cut.

Defensive plays like short-term bonds are out. Offensive-minded yields take the field.

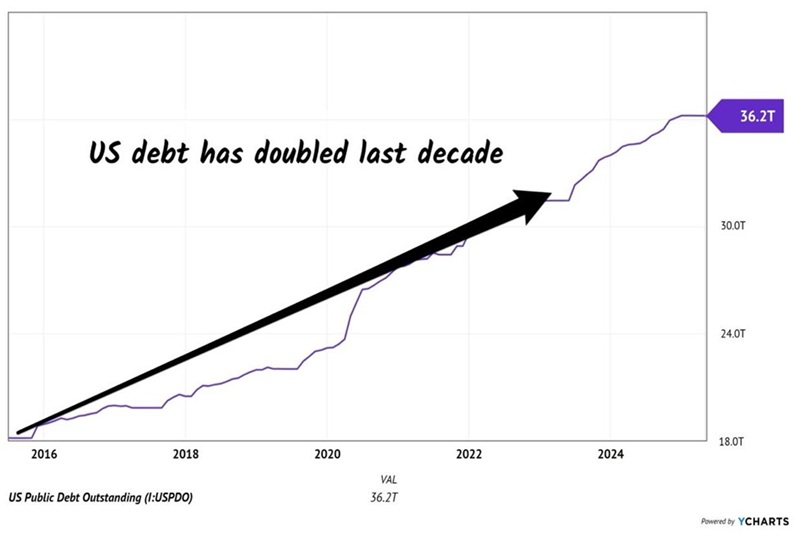

They will shine as the US national debt tab comes due. Uncle Sam has racked up a $36.2 trillion bill, which has doubled in the last decade! Quite the spending bender, not yet including the “One Big Beautiful Bill Act” (OBBBA), which may add an extra $3.8 trillion!

US Debt: An Unstoppable Uptrend

What does a huge debt load and Trump hating Powell have to do with each other? Everything. Treasury Secretary Scott Bessent is issuing 80% of debt on the short end of the yield curve. A lower Fed rate will save the US billions of dollars in interest payments. In fact, US interest payments are already down year-over-year despite a ballooning debt load!

Plus, the administration will not have to “answer” to the bond market, which determines long-term rates. The 10-year yield won’t really matter if the US is issuing 2-year bonds! This will free up policymakers to pursue their true passions like spending money and printing it.

This “short instead of long” issuing practice was unheard of only a few years ago. Treasury debt was traditionally issued at the long end of the curve, such as 10 and 30 years, and purchased by pension funds and sovereigns.

Janet Yellen started the practice and Bessent, while critical, has continued it. Hence their motivation to send Powell out to pasture—save billions in interest payments and take control of the bond market.

By issuing more short-term debt, the US needn’t rely on the “kindness” of strangers (sovereigns) and funds to bankroll its deficit. Banks can permanently stash more (cheaper!) short-term debt on their balance sheets where they can lend against it. Recent legislative changes will let banks effectively lend against this debt, indirectly contributing to monetary expansion.

This monetary environment has already kicked the US dollar down nearly 10% this year.

Is a gashed greenback bad for stocks? Anything but! Bearish dollar trends tend to be wildly bullish for stocks, which happen to be priced in dollars. Plus, American corporations typically get an international sales boost when the buck is low (because our products are cheaper abroad).

Here are four examples of weak dollar periods over the last four decades. All resulted in higher stock prices:

One “pro move” dividend in this environment is Nuveen Nasdaq 100 Dynamic Overwrite Fund (QQQX). QQQX purchases the Nasdaq-100’s tech-driven growth stocks and then sells (“writes”) covered calls on them for additional income.

Tech stocks are particularly attractive for call writing. They are volatile so they command high option premiums—which is profitable for sellers (“writers”) of these options. Plus, the underlying shares have an underappreciated tailwind from shrinking payrolls due to AI!

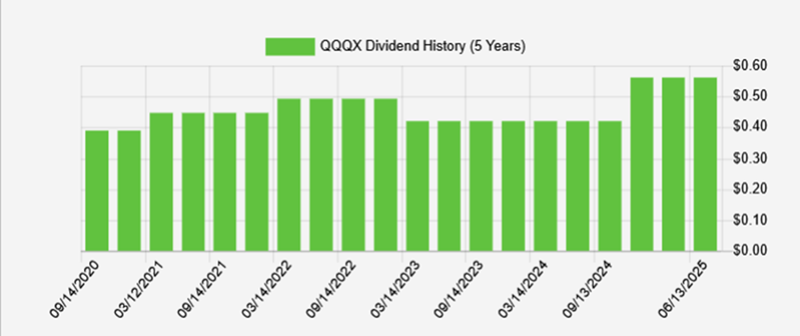

QQQX manufactures a reliable quarterly dividend that annualizes to 8.5% per share:

QQQX’s Reliable Quarterly Dividend

Thanks to April’s aftermath of the late winter almost-crash, the fund still trades at a 7% discount to its net asset value (NAV, or price of the stocks it holds). Which means we can buy the Nasdaq 100 for just 93 cents on the dollar. QQQX is poised for a potential moonshot as tech firms report earnings and articulate to Wall Street what we already know—these cash cows are really going to produce in the quarters ahead thanks to the “rise of the machines” and, therefore, reduced expenses.

How about a bond-like play with stock-like upside for our Fed cut afterparty? Let’s hat tip our friends at FS Credit who gave us another 5.1% dividend raise. Our FS Credit Opportunities (FSCO) now yields 11.3%, paid monthly!

We discussed FSCO as a favorite CEF for 2025, and it has not disappointed. Back in December, FS Investments’ Joseph Montelione shared with us that his firm was preparing for a pickup in M&A under Trump 2.0.

As a business development company in a “CEF wrapper,” FSCO presented us with the best of all possible worlds—a reliable income strategy derived from value-based lending, a fat dividend and a generous discount!

We were “early adopters” into FSCO in my Contrarian Income Report, and we have been rewarded with 25% annualized gains. Now our initial 10% discount to its net asset value (NAV) at purchase has almost disappeared, making future 26% gains unlikely, but hey, it is tough to argue with a secure 11.3% dividend paid monthly.

Safe 5% yields may be as dead as the 4% rule, but that is perfectly fine to contrarians like us. We know where to look for perfectly secure “afterparty” yields up to 11.3%. In fact, I also like three incredible monthly payers that are dishing out dividends up to 10%—click here for the details.