The Supreme Court just ruled on our closed-end funds (CEFs).

Wait. What? Our beloved dividend machines, the lightly driven passenger payout cars we ride to comfy retirements? Our CEFs?

Yes, the third branch of the US government just spent its time deliberating a legal question about our humble, underfollowed CEFs. Why do the courts care about our underowned and unappreciated funds?

We love ‘em because they’re obscure. Underfollowed. And, best of all, inefficient.

Wall Street whales can’t jump into our profitable CEF pond. Most of these funds are $2 billion in market cap or less. If a whale cannonballed in, the entire sector would pop and the value would instantly disappear. No whale can stake a meaningful position.

A billion here or there in market cap is plenty liquid for us. So, we take advantage of generous CEF dividends (high single digits or better) and their dynamic discounts (5%, 10%, sometimes more)—which mean these funds regularly trade for 90 to 95 cents on the dollar.

It’s a contrarian value party for us! Thanks to these fish that are simply too small for the suits to fry.

But one player recently created a legal stir in CEF Land. And wouldn’t you know it, the case climbed all the way to the Supreme Court! It’s FS Credit, a purveyor of CEFs, versus Saba, an “industry activist.”

Saba—the activist—wanted more leverage over the funds. You may have run across Saba if you invest in CEFs. They pretend to ride to the rescue when a fund sells at a big discount.

Saba buys big stakes in CEFs when they’re trading at big discounts. It then uses the votes that come with its ownership stake to force the fund to buy back shares or even liquidate at full NAV. In other words, Saba buys shares big time so it can throw around its weight, close the discount quickly, and cash itself out.

The funds in the court case carry bylaws that strip the voting power of any holder above a 10% stake. These funds are specifically built to block that move. So Saba went to the courts—and the case was elevated all the way to the Supreme Court to rule on it. Saba sued, arguing that these bylaws break the Investment Company Act, a one-share, one-vote rule. On June 11, the court sided with the funds. It ruled, six to three, that Saba had no private right to sue here. Only the SEC can enforce the law—so Saba can’t use the courts for its own purposes to crack the funds’ defenses.

Now, note that the court didn’t explicitly bless the bylaws. It just told Saba it wasn’t allowed to raise the issue itself. What does this mean? Well, for us, these funds keep their protection—so Saba and other activist copycats lose their main lever: buying up stakes large enough to force whatever they want on these funds. This keeps the discounted CEF pond intact for us to fish for payouts and deals.

When Saba does pull off a full liquidation, it’s good for them but usually too bad for us dividend investors. We’re here for the payout, not the bonus pennies on the dollar that the activist may extract! Saba will move on to the next deal, like a house flipper. We income investors just want a reliable payout pillow we can rest our heads on! When the fund liquidates, the dividend dwelling is gone.

With each CEF that leaves the market via liquidation, we have fewer options when we shop for dividend deals. So, the SCOTUS ruling that limits Saba’s leverage over CEFs—its shortcut to liquidation—is a nice development for us.

Plus, there’s some irony! Saba masquerades like a CEF crusader whose mission is to eliminate any and every CEF discount. So let’s turn our attention to

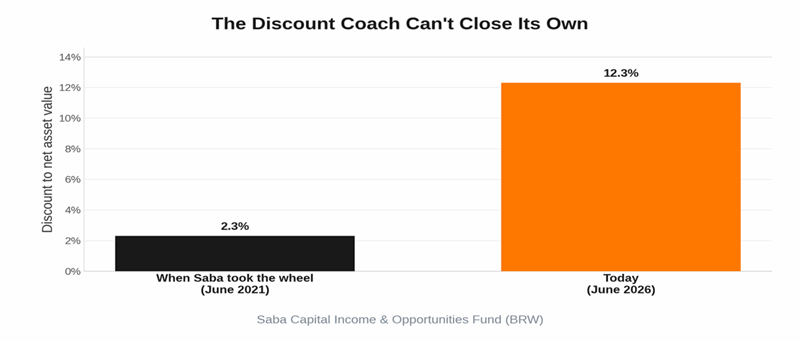

the Saba Capital Income & Opportunities Fund (BRW), a CEF that always trades at a discount.

When Saba took over the fund in June 2021, BRW traded at a 2.3% discount to its net asset value. That’s 97.7 cents on the dollar. Today? The fund’s discount has ballooned to 12.3%. The discount coach can’t close its own window. HA!

And the real kicker? Saba doesn’t need to take anything over. It already runs BRW as the fund’s manager! Saba could easily close the discount window with a buyback, but it hasn’t bought back a single share.

Perhaps the Supreme Court ruling saved Saba from itself?

Anyway, what does this mean for us? Well, when we buy a CEF at a discount, we’re not waiting for the white knight Saba to ride in and close the window for us.

We buy funds where we don’t much care if the discount ever closes. We’re satisfied with the payouts we’re collecting, and we treat the discount as a margin of safety. Why pay a dollar for a dollar of assets when we can pay 95 cents? Or 90? Heck—sometimes we grab them for 88 cents on the dollar or better.

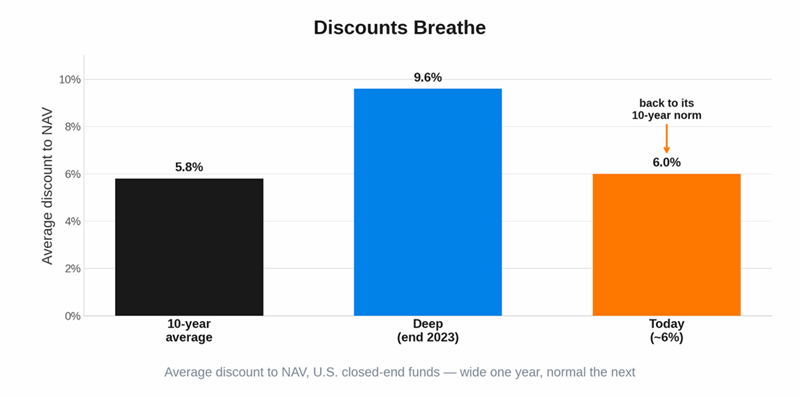

Right now, discounts in CEF Land are about normal. The average discount is 6%, or 94 cents on the dollar. Which, again, beats paying $1 for $1.

So, the bargains aren’t everywhere, but there are well-run funds trading at bigger discounts than the pack.

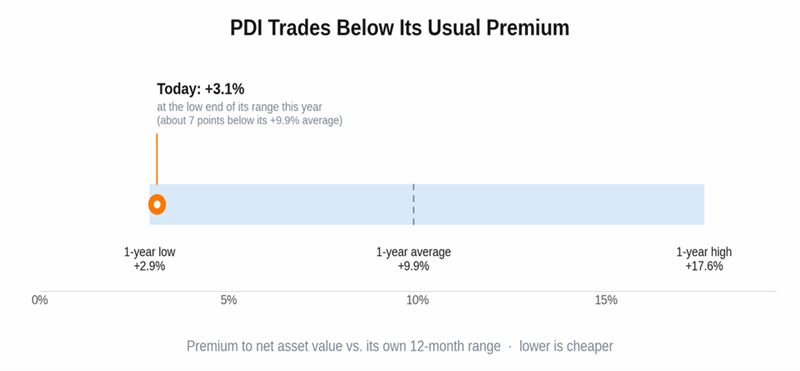

Our job is to find well-run funds trading below their historical averages. Sometimes, this means buying a fund at a premium when it’s a great fund and less than its “average premium!”

Counterintuitive, I know. But that’s what we contrarians live for. We walked through exactly that last week with 16.3% payer PDI (yes, you read right!) trading at a premium that is cheaper than usual:

Bottom line, we’ll keep doing our CEF homework and finding our own bargains. Six out of nine justices confirmed our strategy.

And the “cheat sheet” for the CEF homework assignment is a subscription to my Contrarian Income Report service. Most of the funds we cover pay monthly, not quarterly—so your income lands like a paycheck, twelve times a year. If you’d like to build a retirement around that kind of steady monthly cash, here’s where to start.