New Fed Chair Kevin Warsh’s hawkish debut has given us a “3-stage” plan for 12% dividends now—and strong gains later.

Here’s how I see that playing out, plus two tickers we can use to grab that reliable double-digit income stream.

3 Reasons Why My Falling-Rate Call Still Stands

First up, I haven’t budged on my call for lower rates. But these things rarely happen in a straight line. In fact, had the Iran conflict not occurred, we’d almost certainly be talking about rate cuts today.

But oil prices are falling as I write this, and the International Energy Agency just predicted a supply glut next year. And despite all the noise around the current deal to end the war, it will end. Neither side can afford any other outcome.

The drop in energy prices is the first, and most immediate, stage of our “falling rates” setup.

The second? Warsh himself, who Trump has charged with cutting rates. My take: He’ll start calling for cuts as soon as he can justify it. When push comes to shove, I expect Warsh will choose self-preservation.

Third (and more important) is AI, which provides a sweeping level of automation to white-collar work that is highly deflationary.

In the 1990s, the Internet acted as a similar “deflator” on prices. The move from snail mail to email and from fax machines to web browsers made businesses wildly more efficient, which kept a lid on consumer prices—and a floor under bond prices (hint!). They rallied throughout the entire decade.

For now, though, bonds are hated. Which is fine by us! We’re happy to take the opportunity to scoop up the best closed-end funds (CEFs) holding them while we can do so at some nice discounts.

If rate cuts happen sooner, great. The discount on a buy made today will snap shut, giving us price gains on top of our 12% payout. If it takes longer, fine. We’ll collect our 12% divvies in peace, confident we got in at a bargain.

CEF #1: The “Bond God’s” 12.2% Payout

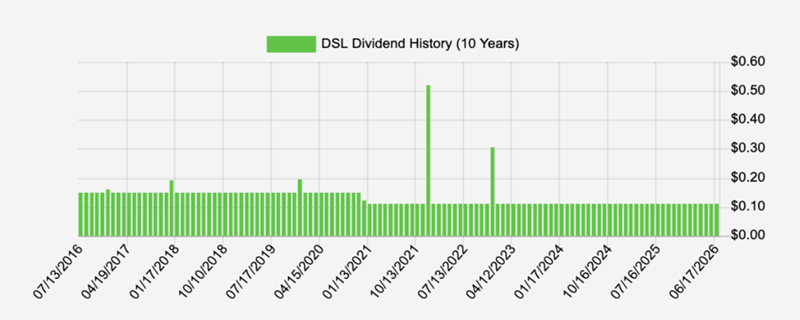

The 12.2%-paying DoubleLine Income Solutions Fund (DSL) is a holding of my Contrarian Income Report service that’s done exactly what we’ve wanted it to since we bought it in April 2016: deliver steady income.

On a total-return basis, it’s up 83.2% as I write this—solid in a volatile time for bonds (and everything else!). In that span, the massive payout has only moved lower once, in the pandemic-rattled market of 2021, when DSL had the chance to snap up bond bargains as rates plunged.

Since then, DSL’s manager, Jeffrey Gundlach (a.k.a. the “Bond God”) has kept the monthly divvies flowing, with two healthy special dividends, too:

Source: Income Calendar

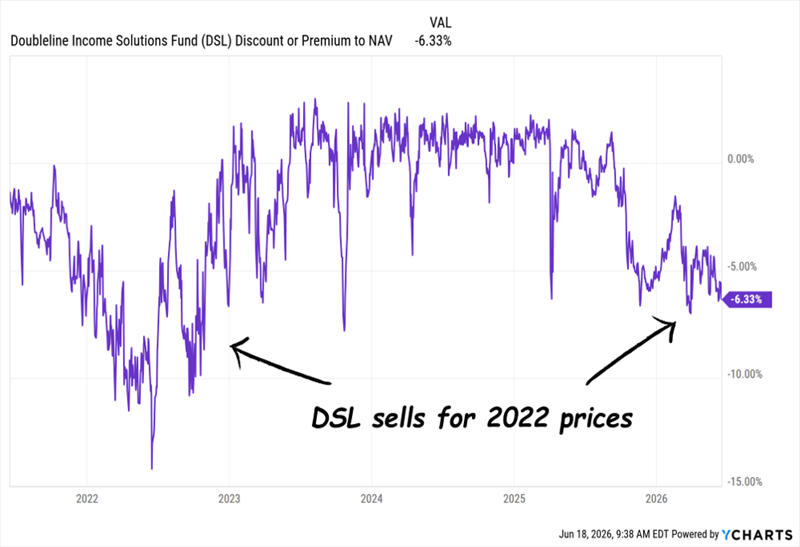

Fast-forward to today and overwrought inflation worries have given us another sweet buy window on this smartly run fund.

As I write this, DSL trades at a 6.5% discount to net asset value (NAV, or the value of its underlying portfolio). That’s a level we haven’t seen this consistently since the last days of 2022, a year in which inflation hit 8%!

Of course, the CPI is less than half that now, and back then, we didn’t have AI, and its deflationary impact, on the radar:

Warsh Drops DSL’s Discount …

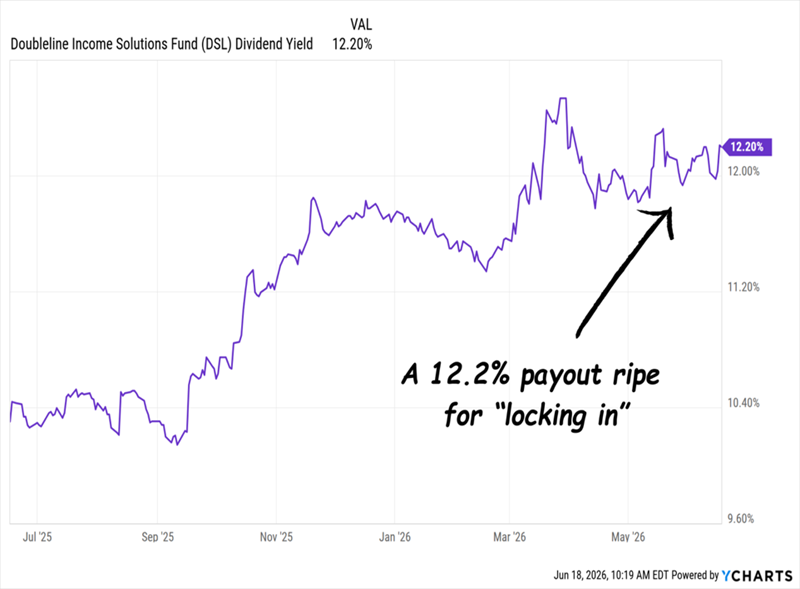

That’s way too cheap for a fund run by a proven manager like Gundlach, who’s got a wide mandate to scour the credit market on our behalf. The discount’s widening has also pushed the yield up to that sweet 12.2%.

… and Gives Its 12% Yield Another Kick

DSL is a textbook contrarian play on today’s overdone rate worries. We’re happy to take the opportunity to grab this steady 12% payer at 2022 prices.

CEF No. 2: A Discount Disguised as a Premium (With Another 12% Payout)

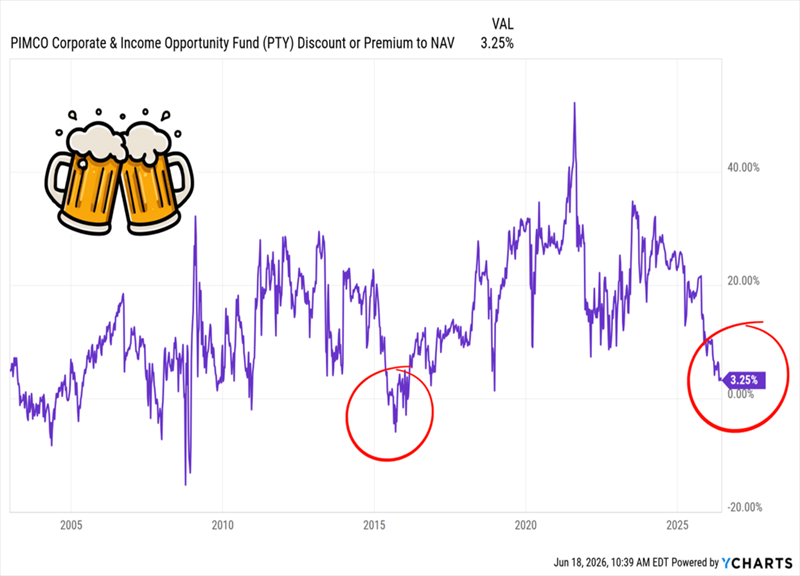

Many first-level investors ignore the PIMCO Corporate & Income Opportunity Fund (PTY) because they think it’s expensive. And to be fair, it does appear so: As I write this, this 12.1%-payer trades at a 3.25% premium to NAV.

But they’re missing the point.

You see, PTY is a PIMCO fund, and that firm, founded by legendary bond investor Bill Gross, holds a stable of CEFs that always trade at premiums, and usually much wider ones than this.

That includes PTY, whose premium has averaged 12.1% in the last year and 20.7% (!) in the last five. Today’s 3.25% premium is also the lowest it’s been, in any kind of sustained way, in the last eight years.

Think DSL Is Cheap? PTY Says “Hold My Beer”

One reason why the fund’s premium has shrunk is likely because of the long effective maturity on its credit assets: 8.5 years. That’s important because longer-duration bonds fall when rates rise and do better when rates fall. But even if rates do rise a bit from here, I think this once-in-eight-year valuation has more than priced that in.

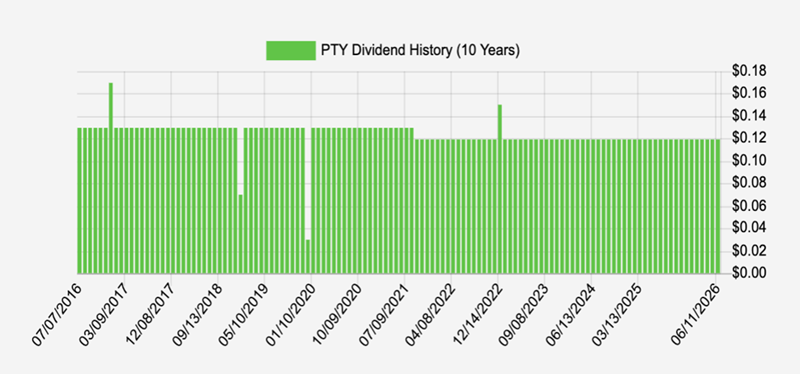

What’s more, the crowd is ignoring PTY’s effective leverage-adjusted duration of 4.3 years. That positions it for gains on lower rates without adding too much risk if rates rise. And PTY, like DSL, delivers a rock-solid monthly payout:

Source: Income Calendar

PTY’s payout, also like that of DSL, saw a slight cut during COVID, but it’s otherwise held steady for years, with regular special dividends (the spikes and dips above) that have more than rewarded investors for sticking around.

So where does all this leave us? As the prospect of lower rates comes into view, PTY’s premium looks set to pop back to its usual double-digit level.

DSL, too, will be in for a repricing, with its discount narrowing from today’s depths. That sets up both funds for gains, and investors to collect their rich dividends as their oversold valuations correct—and beyond.

The 1 Way to Retire on Dividends Alone (Without Investing a Fortune)

These two funds show us what’s possible when you zero in on the right high-yield investments—particularly those that pay you every single month.

To cut to the chase, they give you what I consider the “retirement holy grail”: the ability to clock out on dividends alone—without having to invest in the seven figures to do it!

The above funds are just the opening act on that “dividends-only” retirement. The headliner? My complete 11% monthly dividend portfolio. It gives you a diversified collection of stocks and funds that:

- Pay 11% yields, with payouts you can count on.

- Pay you every single month, right in line with your bills.

- Offer attractive discounts, putting serious upside on the table.

As with DSL and PTY, though, these discounts are likely to compress as the crowd comes around on falling rates.

I don’t want you to miss any of the gains (or monthly dividends) on the table here, so I urge you to make your move now. Click here and I’ll lay everything out for you and give you a free report telling you exactly which stocks and funds to buy.