Every now and then, something happens that shines a light on the value of our favorite income investments—our 8%+ paying closed-end funds (CEFs).

These stout income plays are so valuable, in fact, that some activists are willing to go all the way to the Supreme Court to gain more influence over them.

Let me explain.

A couple weeks ago, the nation’s top court released a decision that meant a lot for CEFs, including those in the portfolio of our CEF Insider service, which yields 8.7% on average as I write this.

Let me set the scene, starting with the activist in the spotlight.

That would be Saba Capital, a hedge fund that’s been agitating for change among CEFs for years. As is the case with all activists, some of Saba’s suggestions are good, some less so. In this case, Saba’s proposal was so strong it prompted the CEF industry to fight back, starting the matter on the road to the top court.

In short, Saba wanted the power to void CEF bylaws that restrict activist shareholders’ voting power. To understand this, remember that a CEF is technically a company, and as such, it has its own bylaws that state what investors, managers and other attached parties can and cannot do to the CEF.

One such bylaw in many (but not all) CEFs is a restriction on how much voting power an activist fund can have, even if they own a large portion of the fund.

Saba wanted more than just greater voting power: They effectively wanted power to sue CEF managers if they were still unable to get their proposals enacted. This would allow activists (like Saba) to effectively void bylaws in the CEF.

In other words, if an activist were to own part of a CEF, and that activist felt a bylaw was against their interest, this move would have given them the power to sue in a bid to force the CEF’s managers to change it.

After several court victories for Saba, CEF managers asked the Supreme Court to hear the case. They did, and the justices decided against Saba’s plan.

The managers of these CEFs are no doubt happy with this outcome. But what’s best for CEF managers isn’t always best for investors, so is this victory really good for us?

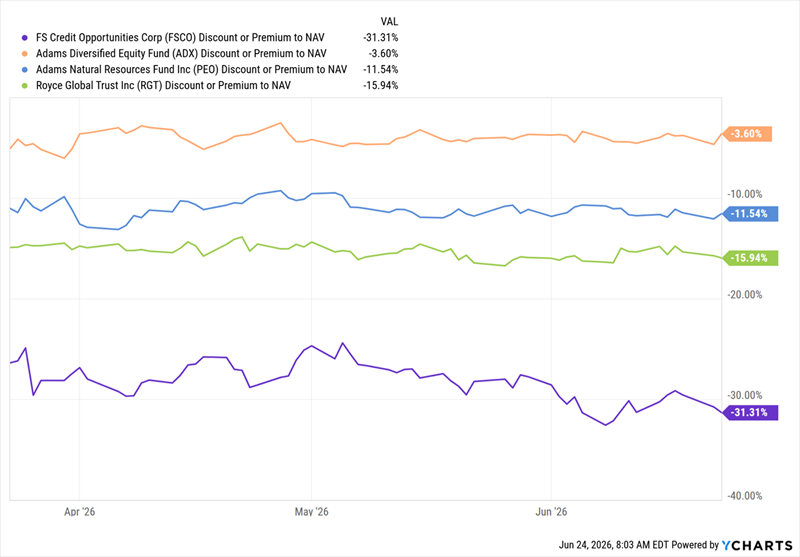

One way to get a sense of that is to look at the movements in the discounts to net asset value (NAV, or the value of a CEF’s underlying portfolio) on the funds mentioned in the above-linked CNBC story.

Those funds are FS Credit Opportunities Corp. (FSCO), the Adams Diversified Equity Fund (ADX), the Adams Natural Resources Fund (PEO) and Royce Global Trust (RGT). If these funds’ discounts have widened since the news in any major way, it would be a sign that investors see this development as a negative for CEF buyers.

Activist Case Loses, CEF Investors Shrug

As you can see, these funds’ discounts have been largely static for the last few months, with only FSCO’s already wide 30% discount growing larger, but only a bit.

This makes sense, as the case was unlikely to go in Saba’s favor. The Supreme Court’s decision was 6-3 against, with the votes splitting along partisan lines. The market expected that outcome.

The bottom line here is that yes, this move is a win for CEF investors, in large part because of this decision’s effect on these funds’ costs. There are two effects Saba’s proposal could’ve had on CEFs, had it won.

First, it could’ve led to constant changes to CEF mandates and strategies, making it harder to manage the funds and introducing uncertainty. Markets, of course, hate uncertainty, so CEFs’ average discounts would likely have widened by quite a bit.

Second, CEFs could have faced a wave of lawsuits from activists, costing time and money. Lawsuits, of course, are far from cheap, especially corporate lawsuits, so we could expect CEF fees to rise.

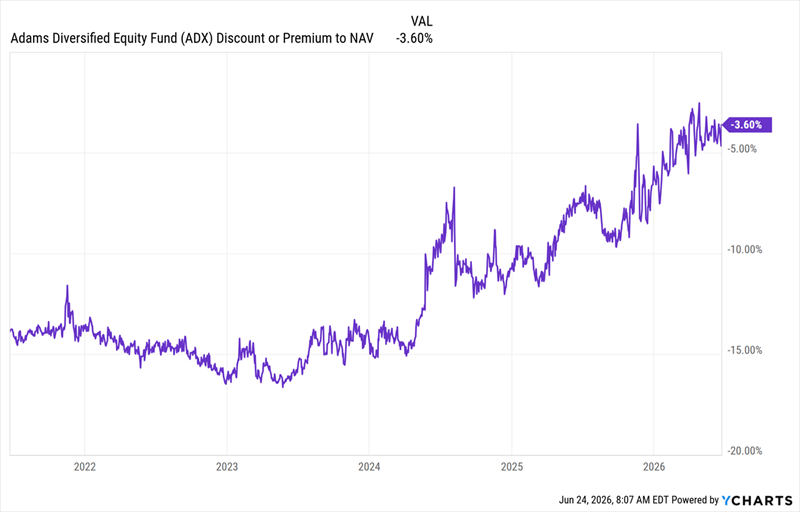

This, by the way, is not a condemnation of Saba—far from it. The firm has done a good job of forcing some CEFs to improve, such as ADX, which Saba pressured to increase its regular dividend in 2024. The fund’s discount has nearly disappeared since then.

Saba’s Pressure Narrowed ADX’s Discount

This was a direct benefit for CEF Insider readers, since ADX has been in our portfolio since July 2017 and has returned 317% for us since, as of this writing. But this latest proposal went too far. We’re happy with the court’s decision.

Supreme Court Decision Makes These (Cheap) 10% Dividends Even Better

The Supreme Court’s decision also protects 4 other CEFs I’m pounding the table on now. I’ve handpicked all 4 to profit from 4 “hidden” booms triggered by the AI revolution.

These 4 funds have all been left behind in the market run-up, making them oversold bargains now—and driving up their yields to an outsized 10% on average.

And now, thanks to the Saba decision, they’re even safer, with the risk of an activist ever placing their interests above ours now essentially nonexistent.

I’ve assembled these 4 funds in a “mini-portfolio” all their own. The time to buy them is now, before the media attention around CEFs prompts the mainstream crowd to buy in.