I had to laugh when I saw this Barron’s headline last week:

“REITs Are Sending a Powerful Buy Signal”

My response? Of course they are! They have been for a while now!

If you’ve been following my articles on Contrarian Outlook, you know I’m a big fan of real estate investment trusts, with their outsized dividends (and dividend growth) and upside potential.

And now the press is finally paying attention.

It is satisfying when the pundits finally catch up to us. But the bad news is that it also means our shot at the biggest gains (and dividends) is likely on borrowed time as the headline-driven herd piles in.

That’s why I’m publishing this article today (including 3 REIT sectors set to rebound, along with 4 individual REITs and REIT funds yielding 6.1% on average and ripe for buying now. See below for more on that).

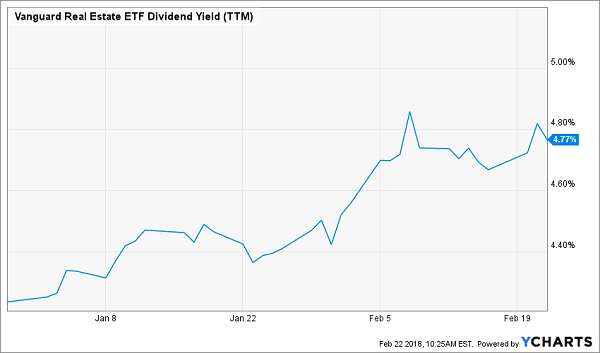

I can sum up today’s REIT buying opportunity in one chart:

REIT Blowout Sale: Everything Must Go!

The double-digit price drop in the Vanguard Real Estate ETF (VNQ) since January 1 has inflated its dividend yield to 4.8% (because yields rise as share prices fall).

Surging Yield Grabs the Spotlight

And you can do way better than that with just a bit of research—zeroing in on trusts with solid 6%+ dividends and/or outsized dividend growth, just like the 4 names I’ll reveal in just a few more seconds.

But you know what makes the big drop in REIT prices even more ridiculous?

As Barron’s says, REITs’ adjusted funds from operations (AFFO, a better measure of REIT performance than earnings per share) are healthy and set to soar, with one analyst calling for a 5.5% rise in 2018, then a 6.5% jump next year.

And for that, the market whacks REITs with an 11% drop!

You and I both know a dead-giveaway like that—cash flow up, prices down—is our “bat signal” to dive into REITs, especially as most of the herd hasn’t caught on yet.

They’re still sitting in cash, terrified that rising interest rates will: a) boost REITs’ interest costs and b) boost the yield on the 10-year Treasury Note, helping so-called “safe” investments like Treasuries steal investors from yield plays like REITs.

Of course, they will overcome this silly fear, and that Barron’s article I just mentioned is the canary in the coal mine.

If you need more proof, this is exactly how things played out from May 2003 to late June 2006, when the yield on the 10-Year surged from 3.4% to 5.25%—a 56% jump!

How did REITs do?

Going by the iShares Real Estate ETF (IYR)—which I’m using in this example because VNQ didn’t launch till September 2004—pretty well!

Rates Rise—REITs Explode

Take a close look at that chart. Notice how IYR (in orange) mostly matches or lags the rise in the 10-Year Treasury yield (blue) and the gain of the SPDR S&P 500 ETF (SPY), in red, until July 2004 before breaking out?

That’s the exact moment we’re in now.

So you’re ready when the REIT wave crests, here are 3 REIT sectors to buy into now (ranked from worst to first), plus a standout REIT from each (I’m leaving out retail REITs; Amazon.com (AMZN) is eating their tenants alive).

I’ve also included a REIT closed-end fund (CEF; click here if you’re unfamiliar with these often-ignored income plays) throwing off a gaudy 8.2% dividend yield now!

REIT Sector #3: Self-Storage

As I wrote on January 16, self-storage is a great play on the booming economy and downsizing baby boomers.

But it also has a low barrier to entry (once you’ve built a facility, you really only have to hand out keys and collect the rent). That’s triggered a boom in self-storage construction, leading to predictable oversupply in some cities.

In fact, according to Life Storage (LSI), owner of 700 facilities in 28 states, there are 89 square miles of self-storage in the US. That’s nearly triple the size of Manhattan!

But LSI is still worth your attention because it does a great job of tapping neglected markets: occupancy ticked up 70 basis points in the fourth quarter from a year ago, to 91.6%; revenue gained 3.4%; and adjusted FFO edged up 2.3%. Those are steady gains for LSI, which yields 5.1% and has doubled its payout since 2013.

The kicker? Thanks to the REIT selloff and its competitors’ antics, you can buy it for 14.7 times the midpoint of management’s forecast 2018 FFO. Cheap!

REIT Sector #2: Lodging

Lodging REITs have a lot in common with self-storage: they’re benefiting from the surging economy (with an assist from tax reform). But some operators have had a tough time keeping themselves from overbuilding. Then there’s disruption from the likes of Airbnb.

So where should we turn here?

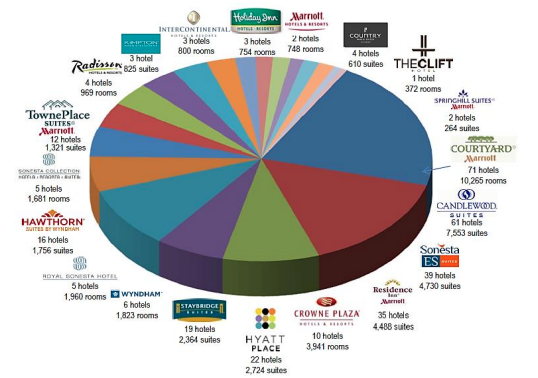

To a “do-everything” REIT like Hospitality Properties Trust (HPT). It’s fighting off Airbnb with 20 hotel brands anchored by instantly recognizable names like Radisson, Holiday Inn and Marriott. Better still, it focuses on business travel, a market Airbnb mostly ignores.

The Entire Hotel Business in 1 Buy

But these aren’t even the best reasons to like HPT.

This is: it boasts 199 Petro and TA travel centers along key interstates, and these humble pit stops will cash in as 3.4% more freight zooms down American highways every year through 2023 (according to the American Trucking Association).

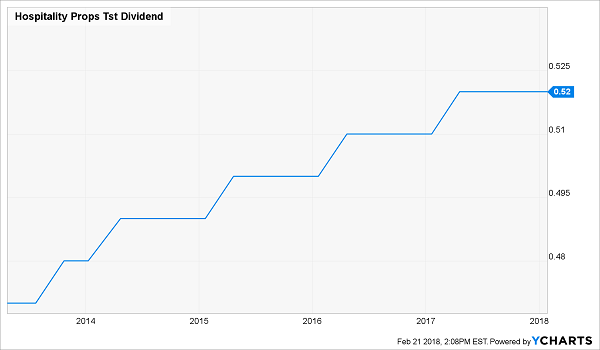

That’s all translating into an incredible 7.9% dividend and payout growth:

The Best of Both Worlds

Two more things: the dividend is easily covered by HPT’s FFO, eating up just 57% over the last 12 months. And the stock trades at 7.4 times FFO—a ridiculous multiple that just can’t last.

REIT Sector #1: Warehouses

Imagine being Amazon’s landlord—sitting back and collecting rent as the e-commerce giant spreads across the world … filling up your warehouses as it does.

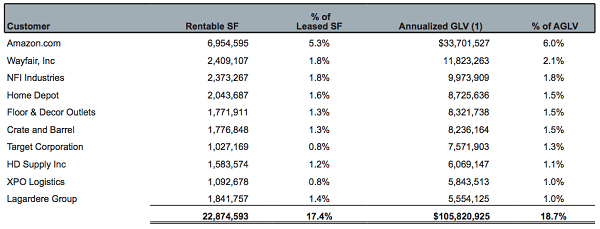

Imagine no more, because you can start (indirectly) collecting those checks from Jeff Bezos’s company through Duke Realty (DRE), owner of 492 warehouses in 21 major markets. Amazon is its No. 1 tenant:

A Strong E-Commerce Play

Source: Duke Realty Q4 investor presentation

Rising warehouse demand is feeding into stronger sales: Q4 revenue jumped 19%, while occupancy at Duke’s operating warehouses held steady at a high 95.7%.

You are only getting a 3.2% dividend here, lower than our other picks, but management has been inching up the payout in recent years and just handed shareholders a nice $0.85 special dividend after unloading its medical office business.

That sale gives DRE more upside as management focuses on the growing warehouse segment. Plus, the REIT’s payout only occupies 62% of core FFO, so it has lots of room to do more there too.

Finally, DRE trades at 19.5 times the midpoint of management’s 2018 FFO forecast, more than reasonable in light of its growth potential.

An “All-in-One” REIT Play With an 8.2% Dividend

Finally, let’s add some international zip with a REIT closed-end fund (CEF), the CBRE Clarion Global Real Estate Fund (IGR).

Two numbers stand out here: 8.2%, the fund’s incredible dividend yield, and 11.8%, IGR’s discount to net asset value (NAV).

We don’t have to get into the weeds with that last figure. It basically means IGR trades 11.8% below the market value of the assets it owns. That’s way below its five-year average of 7.4%, so there’s some nice “snapback” potential here.

Another great thing about IGR? The diversification you get in one quick buy:

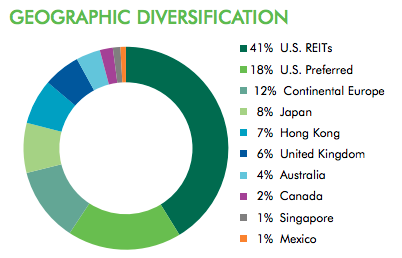

Source: CBRE Clarion Global Real Estate Income Fund December 2017 fact sheet

IGR’s diversification has paid off for investors during the REIT rout: they’ve pocketed a nice gain (including dividends) compared to folks who simply bought VNQ a year ago—and promptly went underwater, even with dividends!

Diversification Keeps Your Nest Egg Safe

One last thing: if you’ve heard about CEFs and worry about leverage, don’t bother: Clarion has only borrowed against 14% of the portfolio. That’s way below the 27% our in-house CEF expert, Michael Foster, sees as a safe level for your average equity CEF.

Just Released: 8 Life-Changing 8%+ Dividends Paid Monthly

Buying the 3 REITs (and 1 REIT CEF) I just showed you gets you in on an incredible number of assets—everything from preferred shares (which are held in IGR) to self-storage REITs and even hotel operators!

The only drawback?

Taken together, these stocks and funds “only” yield 6.1%, on average.

Don’t get me wrong here—that’s a terrific payout in anyone’s book. It’s 3 times more than you’d get from the average S&P 500 stock!

But we can do better. AND we can get our dividend payouts every single month (instead of quarterly), to boot!

The key?

My 8% “Monthly Dividend” portfolio, which I first shared with a select few investors a couple weeks ago. I’ll show it to you now—FREE—when you click right here.

This powerful set of stocks hands you 2 HUGE advantages that will help you retire rich on a lot less than the so-called “experts” say you need:

- A life-changing 8% dividend yield—enough for you let loose a $40,000-a-year income stream on a $500,000 nest egg.

- Dividends paid monthly, so you don’t have to struggle to manage a cash flow that comes in quarterly while your bills come in every month!

PLUS if you’re not leaning on your portfolio for income, you can parlay these gaudy 8% payouts back into these “elite 8” stocks even faster, growing your nest egg and your dividend stream in the process. It really is a set-it-and-forget-it wealth-building machine!

Don’t be left out while other investors lock in their golden years with this powerful new portfolio. Simply CLICK HERE and I’ll give you all 8 of these stocks’ names, tickers, buy-under prices and more right now!