Insider buying can be a great indicator for us income investors to buy alongside management. After all, when the big bosses reach into their own pockets to purchase their own payout streams, it’s a signal that they are confident in more than just the next dividend.

They believe their stock has upside, too. Often this results in total returns (including dividends) up to 214%. I’ll show you some examples, and also break down some current “buy” signals, in a moment.

First, let me make sure we are not mixing up insider buying with insider trading. They are two different things. Insider trading is when someone uses private information that you and I don’t have. It’s illegal.

But insider buying is perfectly legal. It occurs when an officer (think CEO or CIO), someone on the board of directors or another employee on the “inside” buys shares in his or her own company. They make those trades based on already public information, which is fine. And naturally, when they make big purchases, that vote of confidence means a lot more than the average investor’s.

Let me show you a great example of how a big insider buy signaled 214% gains ahead for investors who were paying attention.

Ivan Kaufman is founder and long-time boss at Arbor Capital (ABR), a REIT that makes loans for commercial and multifamily properties (and yields a gaudy 9.5%).

Three years ago, Kaufman—owner of 740,000 Arbor shares—made a daring move for the then-tiny company, dishing out $250 million to buy a commercial-lending agency and its in-house technology platform.

Fast-forward to today, and the new and improved ABR is 3 times as valuable in terms of market cap!

“Skin in the Game” Triples ABR’s Value

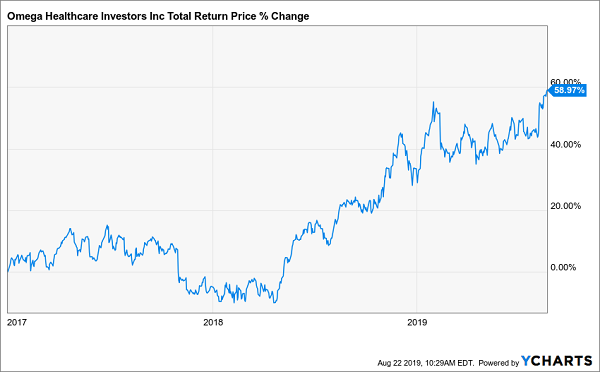

Meanwhile long-term care specialist Omega Healthcare (OHI) had a mostly middling 2017 that turned wretched in the final quarter. But during that final quarter, insiders bought $5.8 million worth of stock—Omega’s highest three-month value of insider buying in the 14 years of insider transaction data I mined.

It was nice timing for the big wigs, who banked fast 59% total returns (including dividends):

Omega’s Higher-Ups Bought the Dip and Banked 59%

Of course big insider stakes like these are rare. But given the big return potential, they are always worth searching for.

Management involvement is something I look for in our Contrarian Income Report premium service. I love seeing insider involvement in REITs, given the long-term nature of their property holdings.

It’s one thing for an insider in a tech company to buy more stock in anticipation of a brand-new product lifting the stock for a year or two. But with REITs, insiders aren’t just looking for a quick pop—they’re making calculated buys of their own cash cows. Big dividends plus 50% to 100%+ price gains is how you get rich investing in REITs.

Let’s review two more landlords, yielding 8% and 9.7%, with insiders buying hand over fist right now.

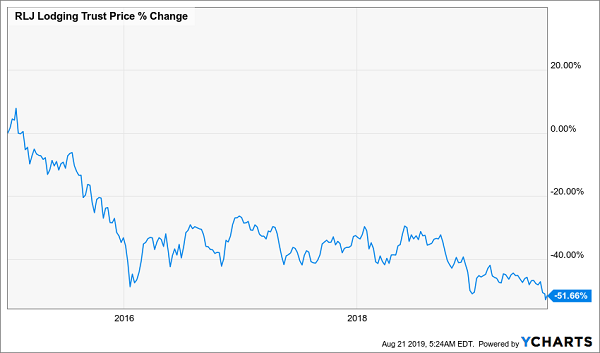

RLJ Lodging Trust

Dividend Yield: 8.0%

RLJ Lodging Trust (RLJ) is a hotel REIT that focuses on “premium-branded, focused service and compact full-service hotels.” It leases out to a wide variety of blends, including:

- Marriott International (MAR): Marriott, Residence Inn, Courtyard

- Hilton (HLT): Hilton, Hilton Garden Inn, Hampton Inn, Homewood Suites

- Choice Hotels (CHH): Sleep Inn

Recently, two insiders decided that now is the time to buy their own shares. A week ago, Director Patricia Gibson bought 10,000 shares worth $163,700, bringing her total holdings to 58,619 shares. Director Robert La Forgia bought half as much–5,000 shares worth $78,500–on Aug. 15, which comes after another 5,000-share buy on June 3 at a cost of about $85,250.

They see value in RLJ’s recent dip:

12% Off This Hotel REIT

The problem? This isn’t just some recent dip. The past three months is just a microcosm of the company’s longer-term trend.

When a Stock Splits the “Wrong Way”

Problem is, RLJ’s brands are largely in the middle and upper-middle areas of the economic spectrum. That’s not where you want to be. I recently wrote that, with few exceptions, the smart money is chasing premium customers. A couple REITs are making hay in the middle and even carving out a down-market niche. But nothing really sets RLJ apart, and it shows.

I have other issues, too. SunTrust analysts recently downgraded RLJ from Hold to Sell on general worries about burgeoning labor costs weighing on hotel REIT margins. RLJ’s dividend hasn’t budged since 2015, which is another black mark. So is roughly $700 million in cash versus $2.2 billion in debt.

RLJ’s insiders might indeed get some long-term value out of their recent buys, but I’m not ready to step in just yet.

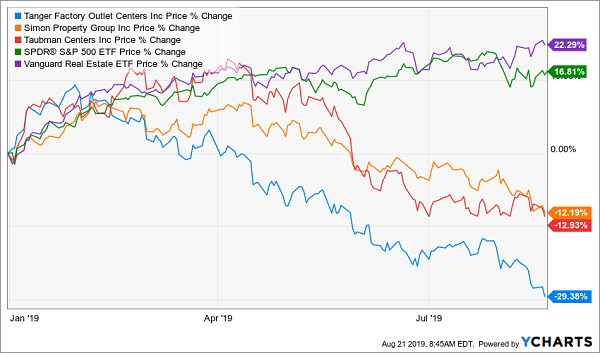

Tanger Factory Outlet Centers (SKT)

Dividend Yield: 9.7%

Stop me if you’ve heard this already, but the retail business is a little difficult right now.

Gymboree. Charlotte Russe. Things Remembered. Payless ShoeSource. Diesel. Barneys New York. These are just a few of the major retail bankruptcies announced in 2019–and we still have several months to go. Retail REITs are unsurprisingly taking it on the chin, with Simon Property Group (SPG) and Taubman Centers (TCO) off about 12%-13% during a rocky but still booming year for the broader markets.

But Tanger Factory Outlet Centers (SKT)—off 29% year-to-date—is perhaps the biggest disappointment in the group.

The Market Has Left Retail REITs Behind

It wasn’t supposed to be this way.

Tanger isn’t a traditional mall REIT. It specializes (as the name indicates) in outlet malls, which are open and not nearly as expensive to operate and maintain as regular malls. They typically don’t have gigantic “anchor” stores a la Macy’s (M) and JCPenney (JCP) that are difficult to fill when the tenant moves out. They’re a destination. People go out of their way to shop there, making them seemingly more resistant to Amazon.com (AMZN) and the march of e-commerce.

Two insiders seem to be buying a hopeful bottom. Steven Tanger–CEO and son of founder Stanley Tanger–recently bought 10,000 shares worth $144,760 to bring his stake up to 1,188,888. Director Thomas Reddin made a six-digit purchase as well, snapping up 7,000 shares worth $102,340. And it’s hard to fault them: They bought in at a nearly 10% yield and just 6 times adjusted funds from operations (AFFO).

But those cash flows are shrinking. Trailing 12-month AFFO is off 3% year-over-year. The company is guiding for an 8% decline in full-year AFFO. Portfolio occupancy actually grew in Q2, from 95.4% to 96.0%, but at the midpoint of full-year guidance, Tanger expects that to shrink to 95%.

Tanger isn’t necessarily disaster in waiting. AFFO easily takes care of the dividend, interest coverage is much higher than necessary. SKT could be a sneaky bargain waiting in the wings. But it has to show investors clearer signs of a longer-term recovery before I can consider this struggling outlet chain a dependable retirement buy.

Urgent REIT Alert: 2 Picks for 100%+ Gains and 8.9% Yields

Real estate investment trusts (REITs) are such a powerful dividend tool that they can make the difference between just getting by in retirement … and breezing by.

Retirees that have a healthy allocation to REITs clip vacation pictures for their photo albums.

Retirees that don’t? They greet you at Walmart.

But the need to buy REITs for your retirement portfolio has gone from “pressing” to “urgent.” Because my Triple-Digit Profit System just did something it hasn’t done since 2015: It tripped its final indicator for us to dive into a totally ignored corner of the market.

The last time all five of my indicators flashed green (like they are this very minute), the group of stocks I want to show you in my brand new REIT Playbook—where cash dividends of 6%, 7% and even 8% are commonplace—started red-hot rallies that resulted in triple-digit profits.

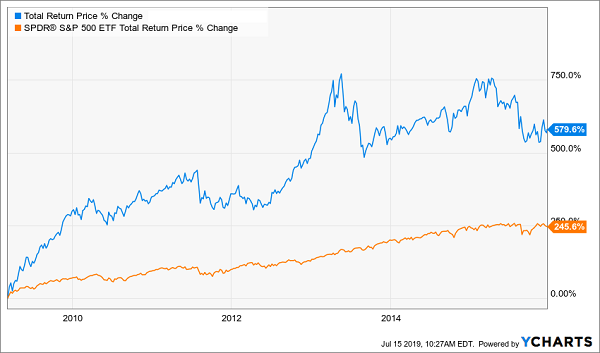

One member of this snubbed group of stocks—a rock-steady “landlord” spinning off a 7%-plus cash dividend—did something that income plays just aren’t supposed to do:

It soared for a market-crushing 580% return.

Doubling the Market With Real Estate Sounds Crazy, But …

It wasn’t alone. Another one of these overlooked cash machines produced a total return of 379% in little more than six years. You’re lucky to get 100% out of the market in that amount of time.

And because this stock had such a large dividend, a big slice of those returns were in cold, hard cash.

That was four years ago. Fast-forward to today, and the Federal Reserve has put its hand on the easy-money spigot, triggering the last of my five buy signals. And now, I have another pair of urgent REIT buys—boasting triple-digit price potential and yields of nearly 9%—that I want to email to you now.

The payouts are simply “going parabolic,” but it’s important that you add these stocks to your retirement portfolio now. Because when their prices go out, you won’t just miss out on their triple-digit gains—but those dividends will shrink on new buyers by the day.