One of the biggest risks you’ll face as an investor is the temptation to listen to people at the extremes.

In income investing, these so-called “gurus” break down into two camps. The first are the indexers, who argue that all you need to do is buy a fund like the Vanguard S&P 500 ETF (VOO), which, as the name suggests, simply tracks the S&P 500. Sure, the yield is a crummy 1.5%, but you need to stick with it, work for 40 years, save as much as you can, and live off the low payout.

Unfortunately, if you follow this “advice,” you’ll have to save north of $4 million if you want a $50,000 dividend stream to live on without selling down your holdings. Let’s be honest: almost none of us will be able to save that much, no matter how long we work.

Then there’s the other camp, which points to ultra-high-yielding stocks and bonds with dividends of 14%+. At that rate, you need just $360,000 to get $50,000 of dividend income.

The trap most followers of this approach fall into is that they simply spot a big yield and plunge in, forgetting that the double-digit-yield space boasts many payouts that are unsustainable. And when those payouts are cut, investors vote with their feet, clobbering the stock, and the value of your investment, as your payout shrinks.

The good news is that you can play straight down the middle, with investments yielding 7% to 8% and boasting payouts (and share prices) that grow. That means $650,000 in savings is enough to get a reliable $50,000 dividend stream.

The Trouble With Investing on Yield Alone

The reason why so many investors fall for dividend traps is that they simply look at the yield and then stop there.

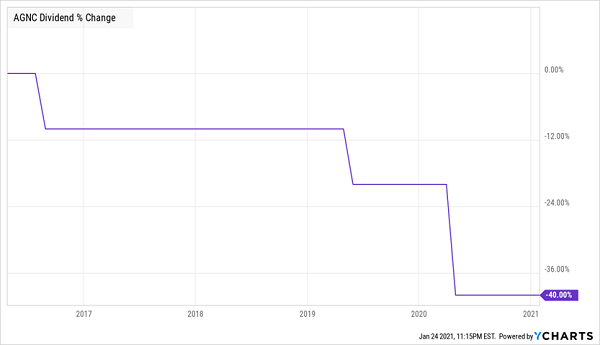

A good example is AGNC Investment Corp. (AGNC), a mortgage REIT that uses aggressive leverage to invest in exotic debt-backed derivatives. My colleague Brett Owens warned about this company back in 2016, when it was attracting plenty of investors with its 13% yield.

Anyone who failed to heed that warning ran into trouble.

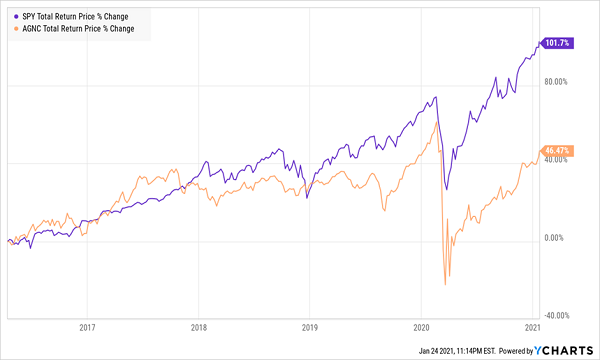

Underperformance Is the Least of AGNC’s Downsides

First up, while AGNC didn’t lose money, it underperformed an index fund by a huge margin, meaning buyers left a lot of money on the table. And that’s not the worst part. This is:

High Yield Masks a Shrinking Payout

AGNC has cut its dividend four times in the last five years, and an investor who bought five years ago is now getting an 8.3% yield on their original buy. That’s the exact opposite direction we want our yield to go in over time!

The pain isn’t over for AGNC holders: more payout cuts are likely, and when you combine those with its history of market underperformance, it’s clear that this big yield was—and is—a mirage.

Getting That Goldilocks Yield

That brings us to the heart of the matter: the investment vehicle that can get you a strong, consistent price return and beat the pathetic 1.5% the index fund pays.

Those would be closed-end funds (CEFs), many of which invest in the S&P 500 and have returns similar to, or better than, an index fund while also boasting big yields. And some of those rich CEF dividends are growing, too!

Take, for example, the Liberty All-Star Growth Fund (ASG), which holds a mix of large- and midcap stocks: names ranging from Microsoft (MSFT) and Amazon.com (AMZN) to property manager FirstService (FSV).

I brought ASG to readers’ attention in a 2019 article on Contrarian Outlook. Back then, the fund yielded 7.7%, and its price (in orange below) has taken off since:

ASG Soars Past the Market

Bear in mind that this gain doesn’t include ASG’s rich dividend! It’s based on price alone. But let’s talk about that dividend, because it’s done something remarkable for a yield this high.

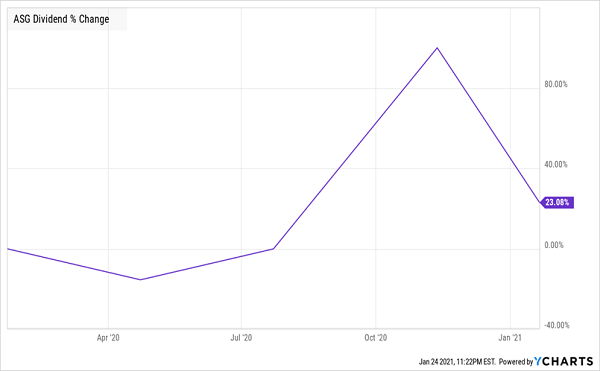

A Monster Dividend and Dividend Growth

Not only did ASG raise its dividend by 14% at the start of 2021, it also paid out a huge special dividend at the end of last year. As a result, investors who bought based on my 2019 article are now sitting on a 10.1% yield on their original investment. And their yield on cost keeps going up, as our poor AGNC holders watch their yield on cost go down.

The best part? ASG holders who want $50,000 in passive income only needed to put $500,000 in as recently as 2019. That’s the power of finding the goldilocks dividend payer while ignoring the indexers and pushers of unsustainable big yields.

5 MORE Goldilocks Dividends (Up to 9%) to Buy Now

Terrific as ASG is, there’s just one problem with buying it now: it trades at an 8% premium to its net asset value (NAV).

That’s another way of saying that the horse is out of the barn on this one—so much so that investors are willing to pay $1.08 for every dollar of assets ASG holds.

There’s no doubt this is a great fund, but a valuation that rich will limit its upside from here.

So let’s put ASG on our watch list for now and turn our attention to my 5 favorite CEFs to BUY today. This 5-pack yields 8%, on average, and these dividends are reliable. What’s more, these funds trade at big discounts to NAV—so much so that I’m calling for 20% price upside from them in the next 12 months.

And that’s in addition to the solid 8% dividends we’ll collect.

Full details on these 5 proven wealth generators are waiting for you now: Click here and I’ll share everything I have on them, including names, tickers, complete dividend histories, my unvarnished take on management and much more.