If you’re like me, you’re starting to collect your tax documents with a certain sense of dread.

It’s understandable as another April draws nearer. But there is a ray of light in the tax-season gloom for us—it comes in the form of municipal bonds, which can boost our income and minimize our future tax burden, too.

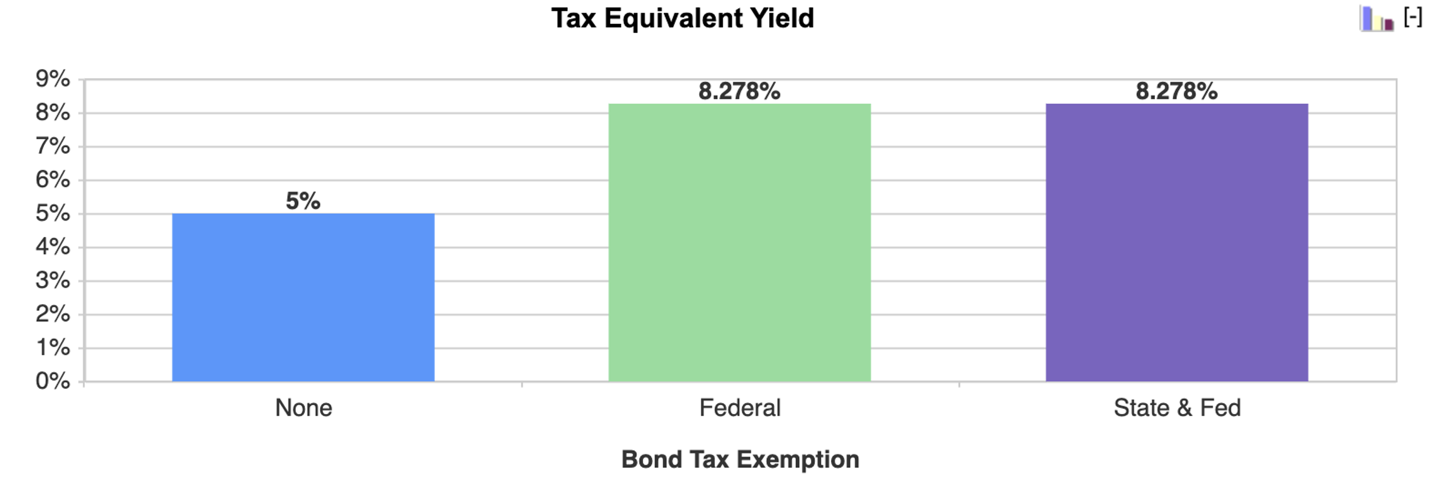

“Muni” bonds offer big yields these days, thanks to the Fed’s interest-rate hikes over the last couple years. That’s doubly valuable now because these yields are federally tax-free for almost all American investors.

That means if you’re in the highest tax bracket, you could buy 5%-yielding muni bonds and end up with the equivalent of an 8.3% yield from taxable assets like stocks or corporate bonds.

Source: Bankrate.com

Of course, there are some issues with this. For one, buying just one municipal bond isn’t easy, nor is it particularly wise: municipalities have special relationships with certain underwriters who hand over the best bonds to their best customers.

Trust me, those customers do not include individual investors like you and me! They’re big banks and investment firms like Nuveen, Putnam and PIMCO—firms with trillions of dollars under management between them and who regularly buy hundreds of muni bonds a year.

Fortunately we can join forces with those companies, thanks to the closed-end funds (CEFs) they offer. But while there are hundreds of muni-bond CEFs out there, not all are great investments.

So to help separate strong muni plays from the pretenders, we’re going to look at three “must haves” when buying munis and see how three individual muni-bond CEFs stack up to these yardsticks.

Muni-Bond CEF “Must Have” #1: A Historically Sustainable Dividend

One great thing about muni-bond CEFs is that their income doesn’t tend to fall hard in bad times. But that doesn’t mean their payouts are always consistent, either.

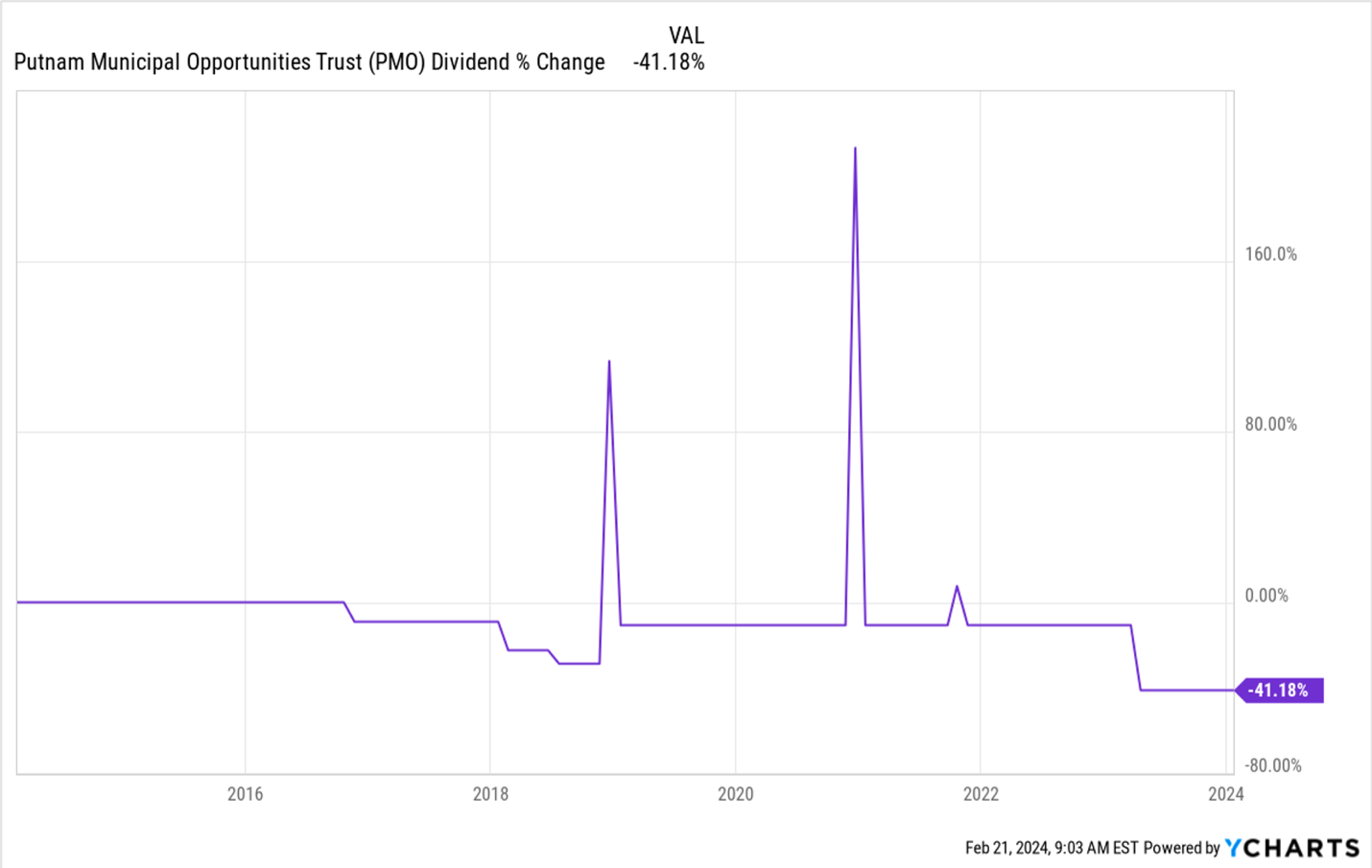

Take the Putnam Municipal Credit Opportunities Trust (PMO), a muni-bond CEF that has cut its payout several times over the last decade.

PMO Shareholders’ Income Takes a Hit

Those cuts are worrisome, especially as they follow two special payouts (the big spikes above). Should we worry that the fund’s payouts will be cut again? Possibly. But it’s also worth noting that PMO’s 4% yield is more sustainable than it’s been since the pandemic, for one important reason: market pricing.

Which leads us to …

Muni-Bond CEF “Must Have” #2: A Discount!

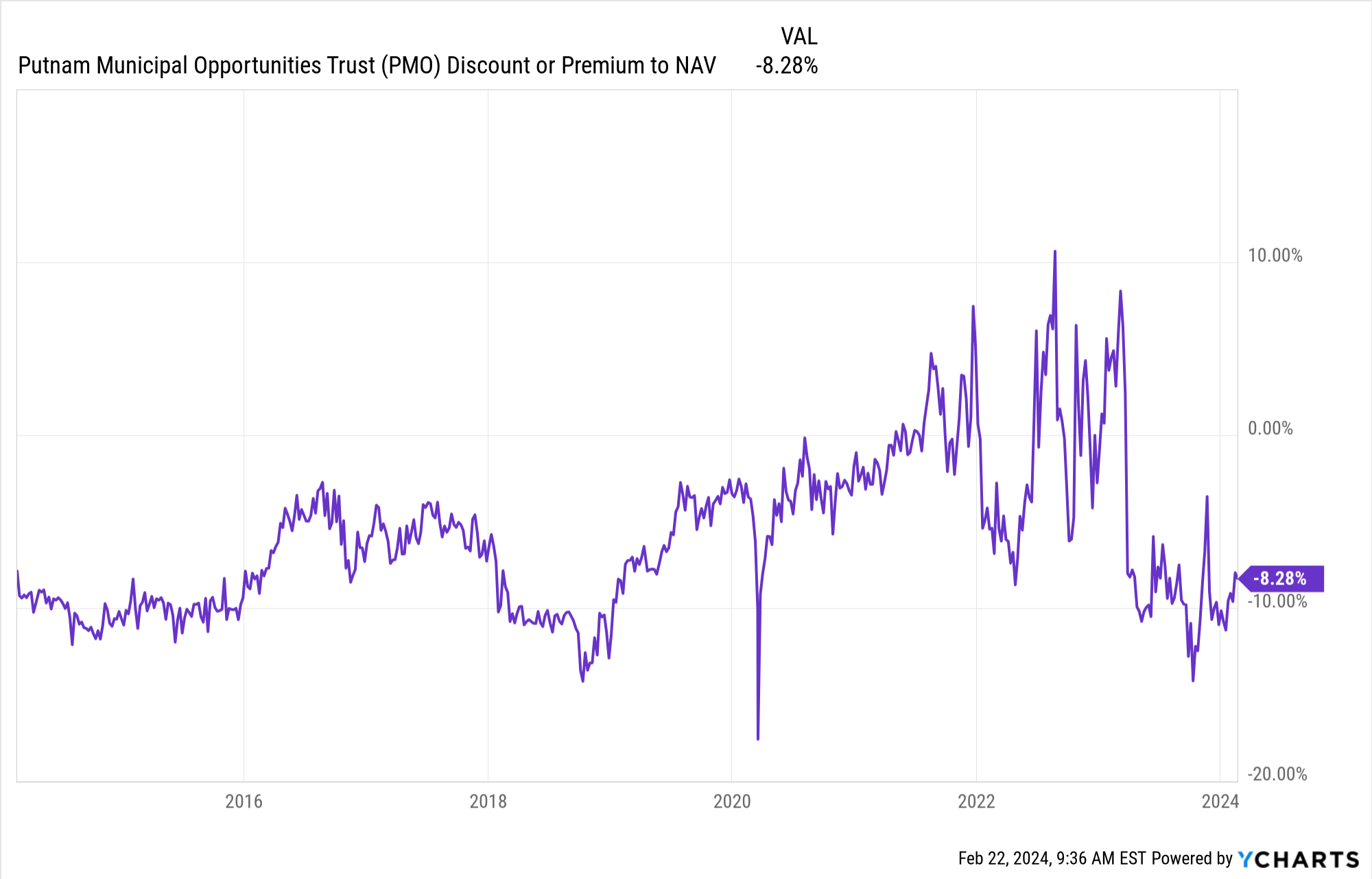

Unlike mutual funds, which are priced at net asset value (NAV, or the value of their portfolios) daily, and unlike ETFs, which always trade close to their NAV, CEFs routinely trade at discounts (or premiums). And PMO has definitely shown more value lately:

PMO Goes on Sale

Following the pandemic, PMO traded at a small discount and briefly at big premiums. But now that it trades at an unusually wide 8.3% discount, there’s reason to believe we’re getting a deal today.

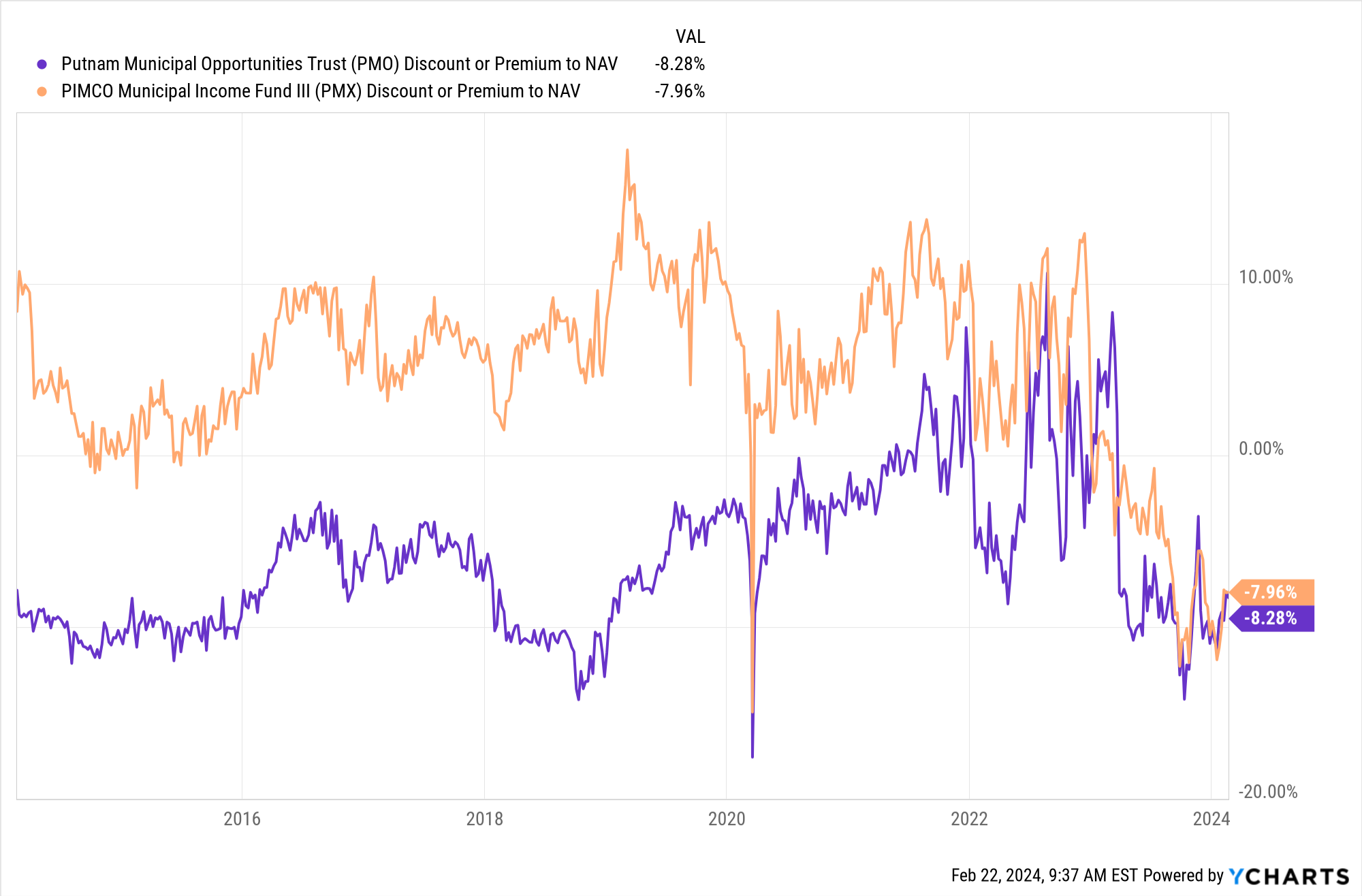

That doesn’t mean PMO is the best fund in that regard. Check out the PIMCO Municipal Income Fund III (PMX), in orange below, which trades at a similar discount:

PMX’s Sudden Sale

PIMCO, based in California, has a lot of cache with wealthy Californians looking for tax-free income, which is why PMX usually traded at a premium before the Fed aggressively cut rates. Now it’s trading at an unusually big discount, giving us a better opportunity to sell at a profit in the future than we may have with PMO.

What’s more, that discount also means PMX’s 5.3% yield (based on the fund’s discounted market price) is more like 4.8% when calculated based on NAV. That’s another way of saying it’s easier for management to maintain payouts than in the past.

On that note, PMO’s 4% yield is more like 3.7% and therefore even more likely to sustain itself, despite what you’d expect given that fund’s recent cuts.

Muni-Bond CEF “Must Have” #3: Management Quality

Why did these two funds trade for more than their assets were intrinsically worth? One reason is management: better managers produce better returns, which fetches premium pricing as more people spot that sterling performance history and invest.

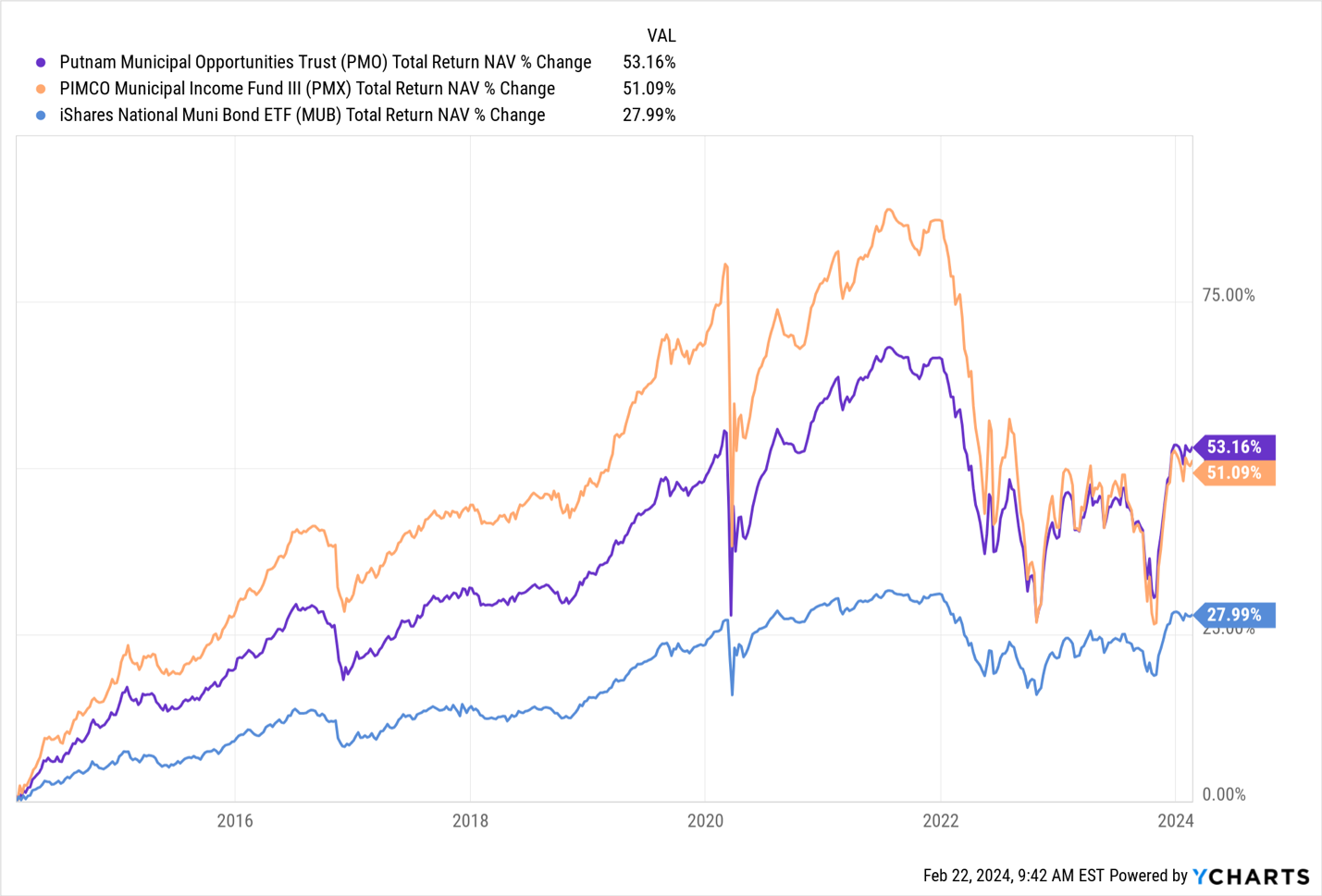

PMO and PMX Post Market-Crushing Portfolio Returns

When we look at total NAV return, which measures the profits the fund’s management generated on their portfolios, we see that both exceeded the benchmark municipal-bond index fund iShares National Muni Bond ETF (MUB) by almost double, and that outperformance has remained for a decade.

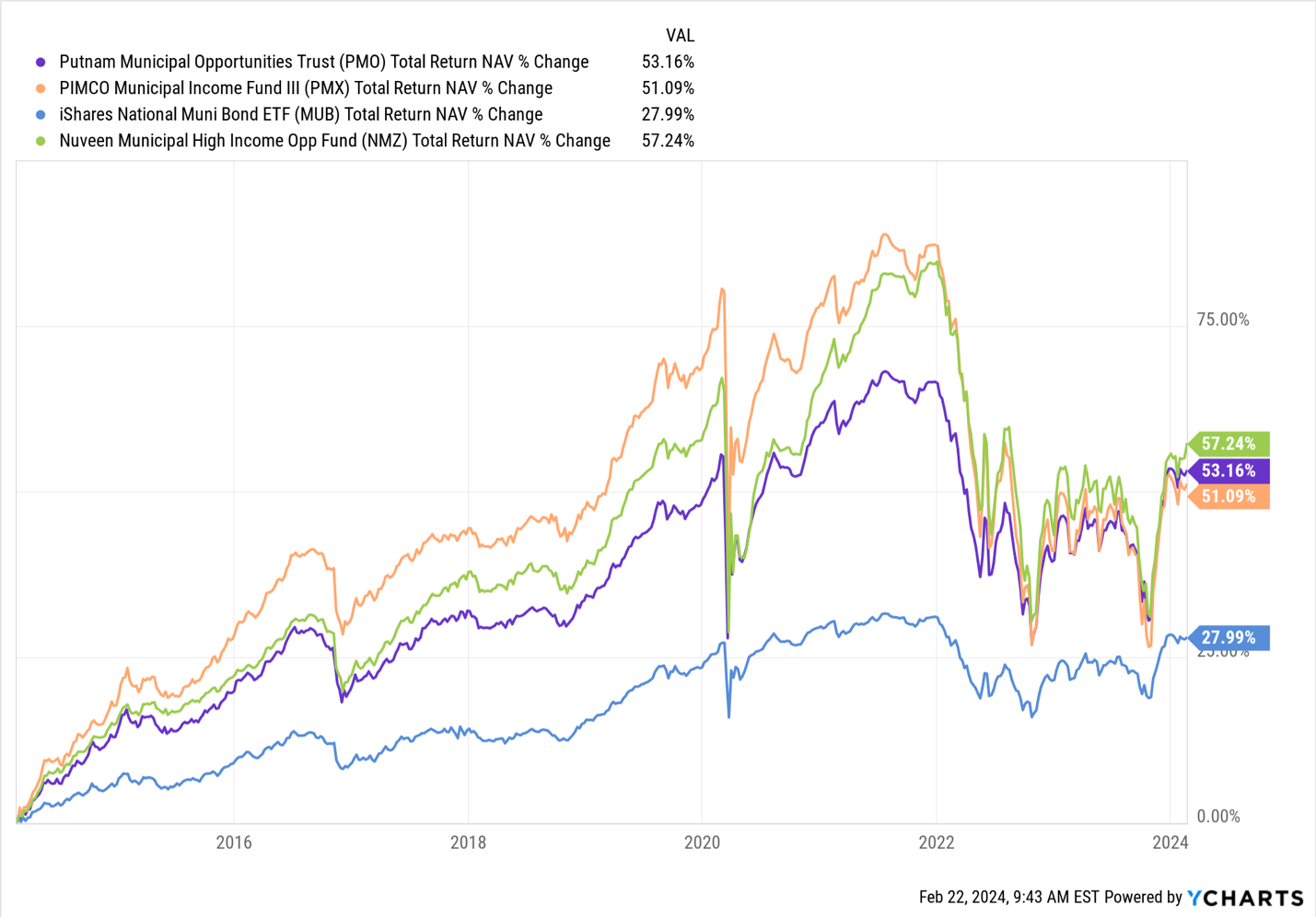

On that front, there’s an even better fund to consider: the Nuveen Municipal High Income Opportunity Fund (NMZ) with an impressive 5% yield and an even more impressive history, outperforming the index and these other funds (see the green line below) on a total-NAV-return basis.

NMZ the Long-Term Winner

Is NMZ the winner on dividend and discount fronts, too? Almost, but not quite. At 7.8%, NMZ’s discount is near the widest it’s been in the last decade.

However, that’s after several dividend cuts in 2022 and 2023 as interest rates went up—although history doesn’t always matter, and NMZ’s 4.6% yield on NAV is pretty sustainable given higher interest rates these days.

Then there are the tax benefits on the fund’s 5% yield (on market price) to factor in, too. So even if NMZ does see another small payout cut in the next few months (which I find unlikely), we’d still be left with a big income stream that’s hard to compete with.

And if you wait for the long term, history says you’ll vastly outperform the index fund while collecting a yield much bigger than its weak 2.7% payout, too.

4 CEFs With Dividends so Big (10.2% Yields) You Won’t Care About the Tax

We all love tax-free dividends, of course. But I’ve found 4 other CEFs that pay much more than these three muni-bond funds. They don’t enjoy the same tax benefits, but with yields like these (10.2% as I write this!), we don’t care about the taxes on them!

Even after tax, that 10.2% payout still works out to a massive income stream for just about any investor. Plus, these 4 funds trade at such deep discounts I’m calling for 20%+ in price gains alone in the next 12 months.

I’ve prepared a special investor bulletin that’ll give you the whole profitable story. Click here to read it and download your copy of a FREE Special Report naming these 4 bargain-priced 10.2%-paying CEFs.