Bond bargain alert! Three secure funds yielding 8% to 9% are for sale on the discount rack.

Thanks to a two-year run of rising interest rates, these bond-like investments are cheap. I don’t expect this to be the case for long, with rates ready to relax.

These hybrid vehicles are part-stock, part-bond. They prioritize yield over price gains, which is just fine for us income-focused investors.

These “preferred” stocks share some elements of common stocks (the normal shares of companies that most of us own). We buy preferreds on a stock exchange. They represent ownership in a company. And they can move higher and lower in price.

But they also share some characteristics with bonds. They don’t have voting rights. They deliver a fixed (and usually high) amount of regular income. And they trade around a par value—so while they can move higher and lower, they’re typically much more stable than common stocks.

Preferreds are the definition of “boring is beautiful” investments. But because they’re boring, we almost never hear financial media or analysts talk about them. They largely like to focus on narratives and potential growth, and for that, they need to talk about common stocks.

But if all we really want is a big stream of income, preferreds will keep our attention.

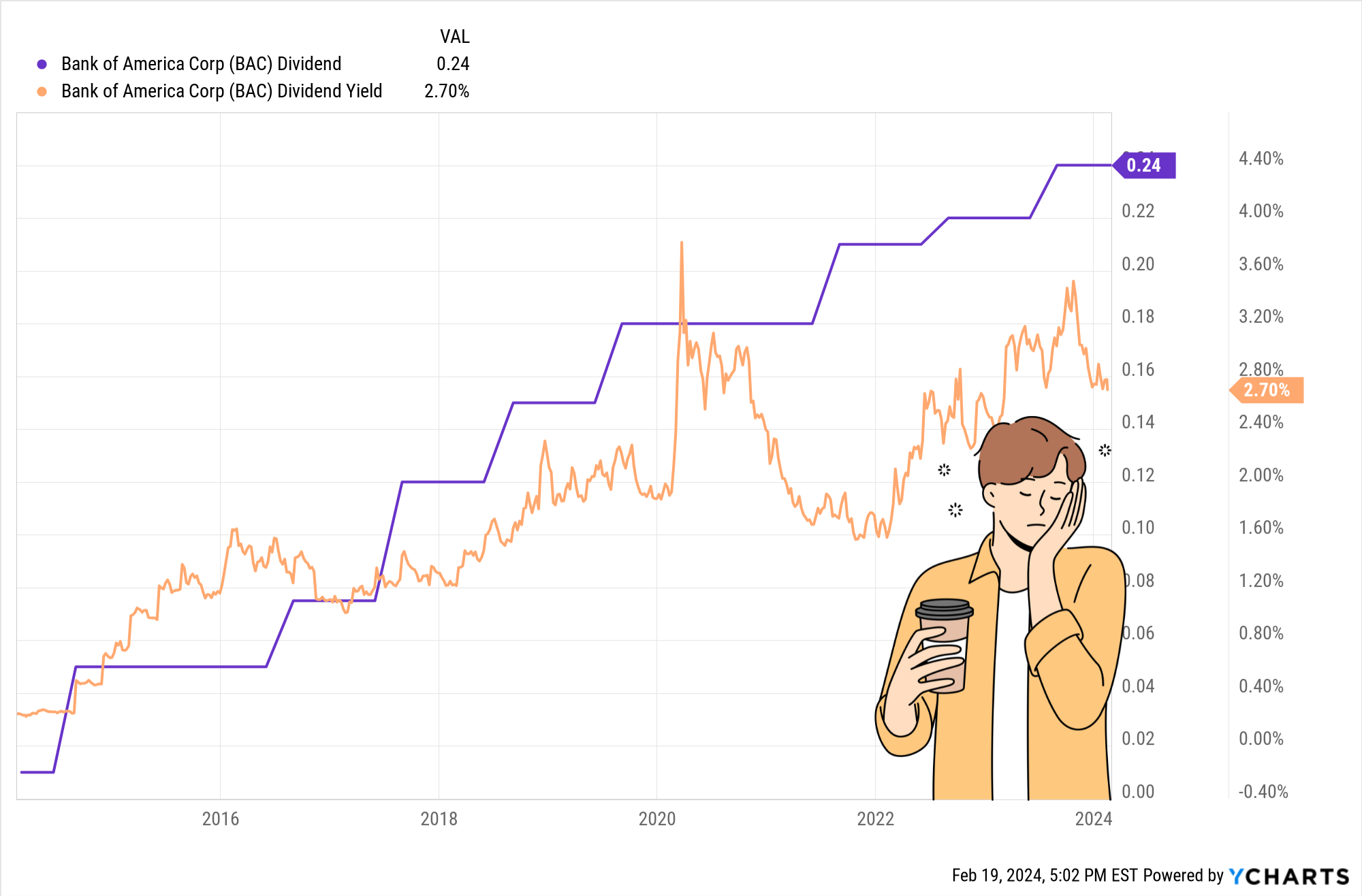

Bank of America (BAC) is a great example of how one company can provide two very different levels of income from its common and preferred shares.

BofA joined most other U.S. bank stocks by slashing its dividend during the Great Financial Crisis. BAC went from a 64-cent-per-share quarterly dividend in 2008 to a nominal penny-per-share in 2009, and didn’t meaningfully start building the payout back up until 2014. Today, Bank of America shares only pay about a third of what they did before the GFC. Still, investors have largely enjoyed a yield of between 2% and 3% for the past few years.

BofA: A Sleepy Yield We Can Get Just About Anywhere

So, that’s one way to invest in Bank of America: Buy its common shares (which have largely underperformed the sector in recent history) and get a little less than 3% in yield right now.

Or, we could buy its Series L Convertible Preferreds and get more than 6% in annual dividends. And they’re not nearly so volatile.

Preferreds aren’t bulletproof. The past two years have more than shown that—but we can thank a period of rapidly rising Fed interest-rate hikes that, like bonds, beat preferreds’ prices into the ground.

But while rate cuts might not start as early as everyone would like, the future direction of the Fed fund rates arrow is decidedly down. Preferred prices have already enjoyed a small tailwind in recent months, and they could do much, much better once the central bank starts easing.

Let’s do ourselves a favor, though: Look to preferred funds, not individual preferred stocks. Individual preferreds are rarely covered, so there’s little information to go on. Preferred funds, on the other hand, lets the manager (or index) do the picking for us, and they spread our risk out across hundreds or even thousands of stocks.

My choice would be preferred closed-end funds (CEFs) over exchange-traded funds (ETFs). CEFs allow us to tap the brains of active managers who specialize in this kind of asset, and they sometimes allow us to buy preferreds at cheaper prices than had we bought them individually.

Let me show you three of the most popular preferred ETFs on the market, which have collectively hoarded billions of dollars of “dumb money” assets—and then I’ll introduce three “replacement” CEFs that yield between 8% and 9% instead.

VANILLA ETF: Global X U.S. Preferred ETF (PFFD)

Yield: 6.3%

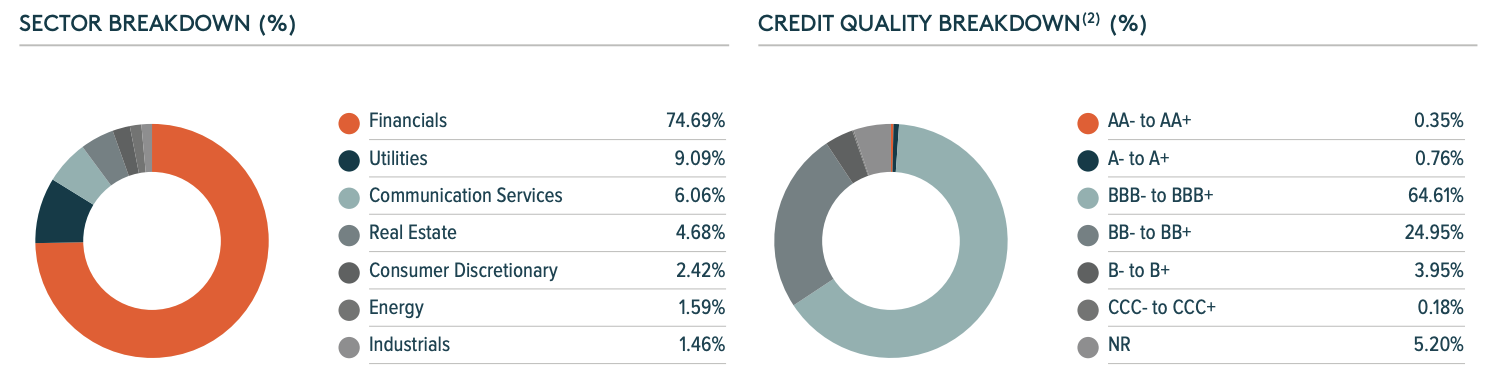

The Global X U.S. Preferred ETF (PFFD) is a $2.4 billion preferred-stock index ETF that’s pretty typical in construction. Its U.S.-centric preferred portfolio is three-quarters invested in financial stocks, with much lighter exposure to preferreds in utilities (9%), communications (6%) and a handful of other sectors.

Among the most outstanding characteristics of PFFD is its credit quality. Its nearly 65% exposure to investment-grade preferreds makes its portfolio one of the highest-rated we can find—in either ETFs or CEFs.

Source: Global X

CONTRARIAN PLAY: JH Premium Dividend Fund (PDT)

Yield: 9.0%

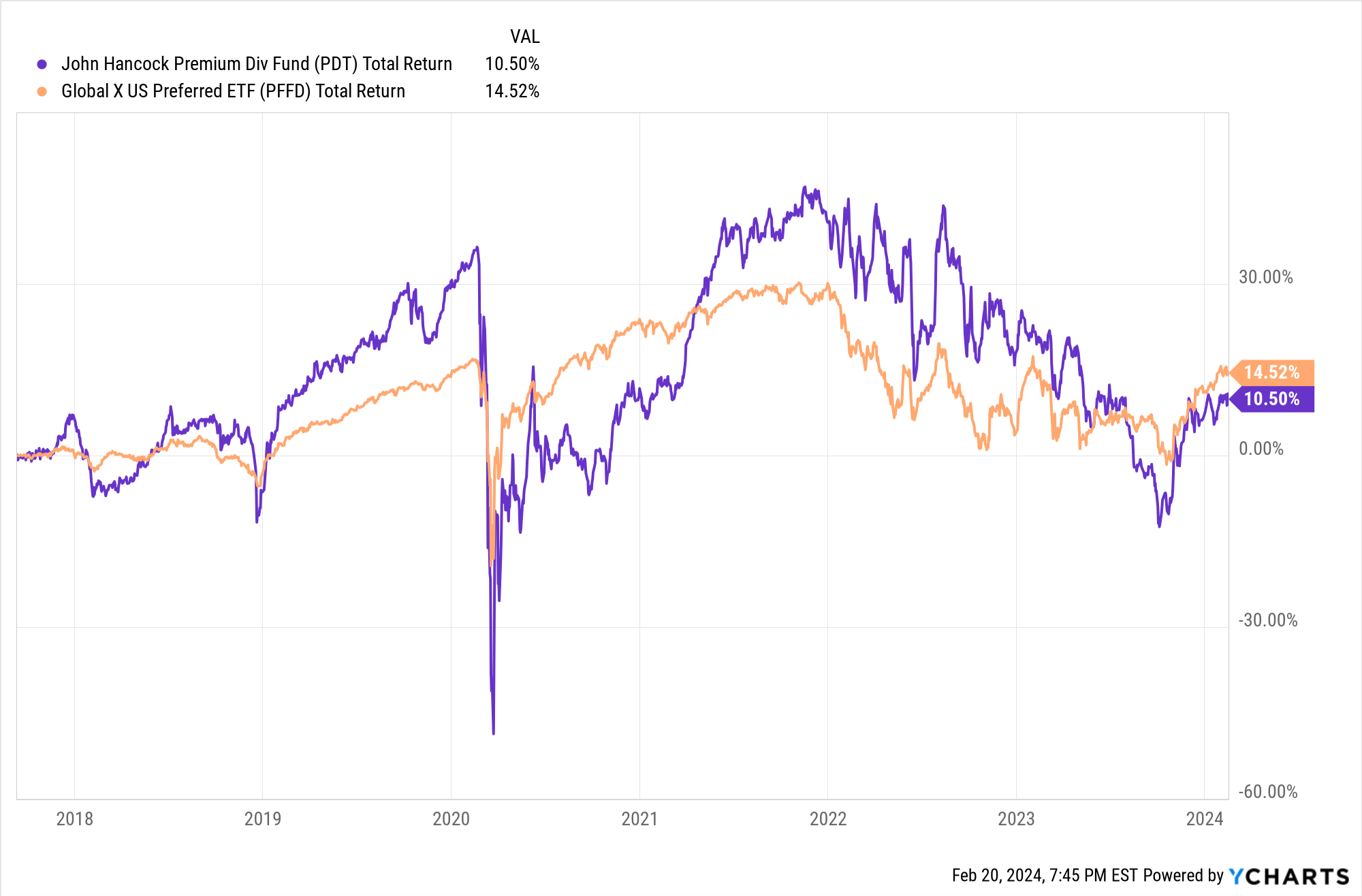

The JH Premium Dividend Fund (PDT) is an example of how CEFs and human managers can deliver something different.

Consider PDT a broader income portfolio of sorts. That’s because it invests not just in preferreds, but dividend-yielding common stocks as well, currently at a roughly 60/40 split. That gives us the opportunity to enjoy both high yield and the potential for outsized gains should the stock market pick up speed.

This John Hancock product boasts a fairly tight portfolio of just 117 holdings, which it leans into extra-hard with a high 39% in debt leverage. Like PFFD, the vast majority of its holdings are U.S.-based. But unlike PFFD—and most other preferred ETFs, for that matter—financials don’t make up a majority of the fund. They still loom large, at 40% of assets, but utilities make up another 40%, with the rest sprinkled among a few other sectors. Top holdings currently include the likes of Verizon (VZ) and BP (BP) common shares, as well as 8.594% preferreds from Citizens Financial Group (CFG).

Over the long haul, PDT has been a much more productive fund than plain-vanilla preferred ETFs, though quite more volatile thanks to both the leverage and common-stock holdings. Performance in recent years, however, has been a bit choppier.

Active Management Hasn’t Shown Its Value-Add of Late

One thing going in PDT’s favor, however? The CEF currently trades at a 7%-plus discount to net asset value (NAV). That’s good on its own, but great when we consider that over the past five years, it has traded at a 5% premium on average.

VANILLA ETF: First Trust Preferred Securities and Income ETF (FPE)

Yield: 5.9%

The $5 billion-plus First Trust Preferred Securities & Income ETF (FPE) holds a robust portfolio of more than 230 preferreds. Like with PFFD, this is a high-quality group; nearly two-thirds hold investment-grade ratings. Sector weightings are par for the course, too, with financials at 75% and everything else at single-digit levels.

Source: First Trust

Where this First Trust ETF deviates is geography. Only a little more than half its assets are invested in U.S. preferreds—the rest is scattered across nine other predominantly developed economies, including Canada (11%), the United Kingdom (10%), and France.

FPE also stands out in that it’s an actively managed ETF. Whereas fees are usually one of the few stark advantages ETFs have over CEFs, they’re not much of an edge for FPE, which at 0.85% has a pretty high expense ratio compared to its peers.

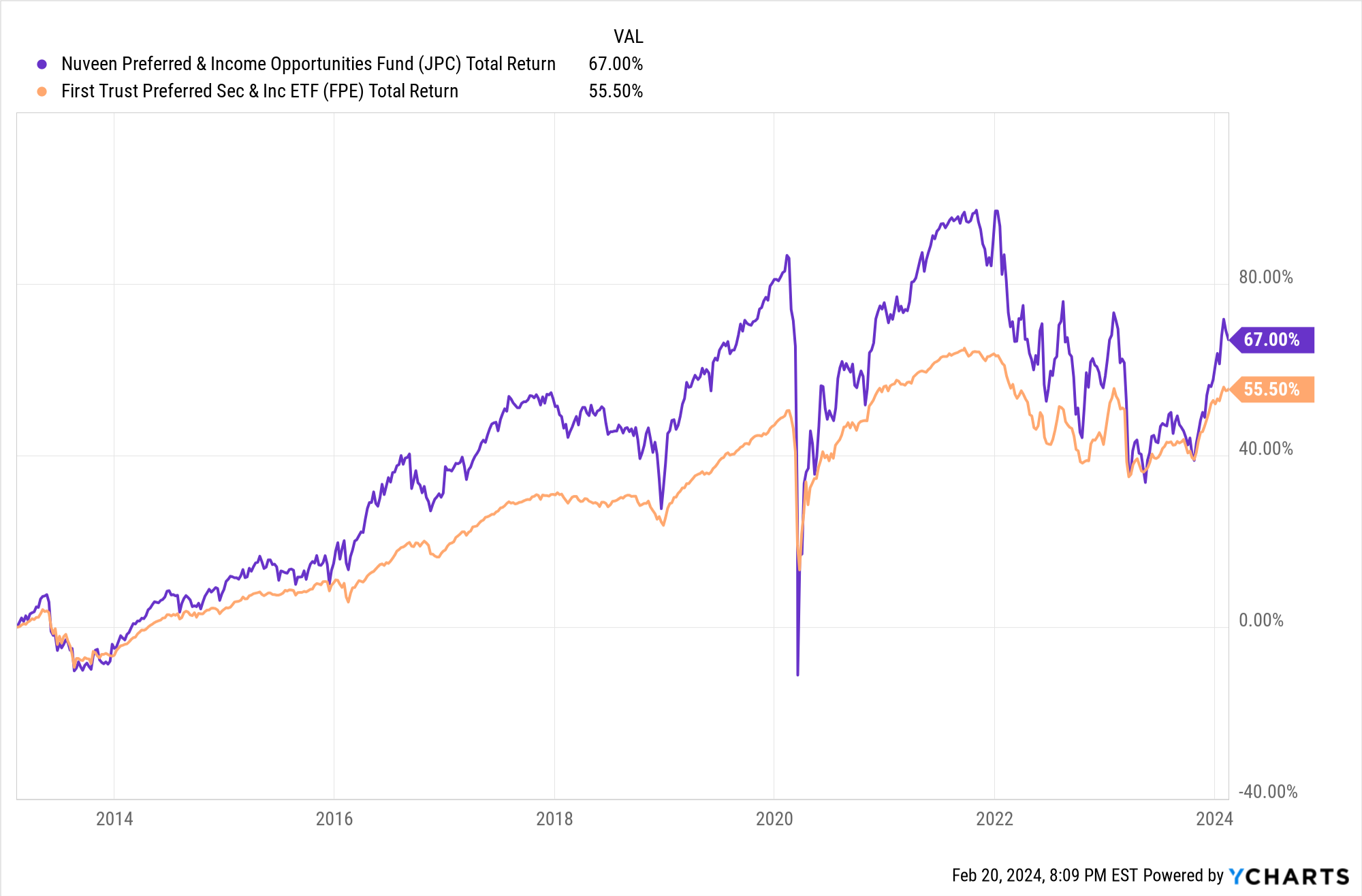

CONTRARIAN PLAY: Nuveen Preferred & Income Opportunities Fund (JPC)

Distribution Rate: 8.0%

FPE might have a high-quality portfolio, but the Nuveen Preferred & Income Opportunities (JPC) is downright sterling.

Source: Nuveen

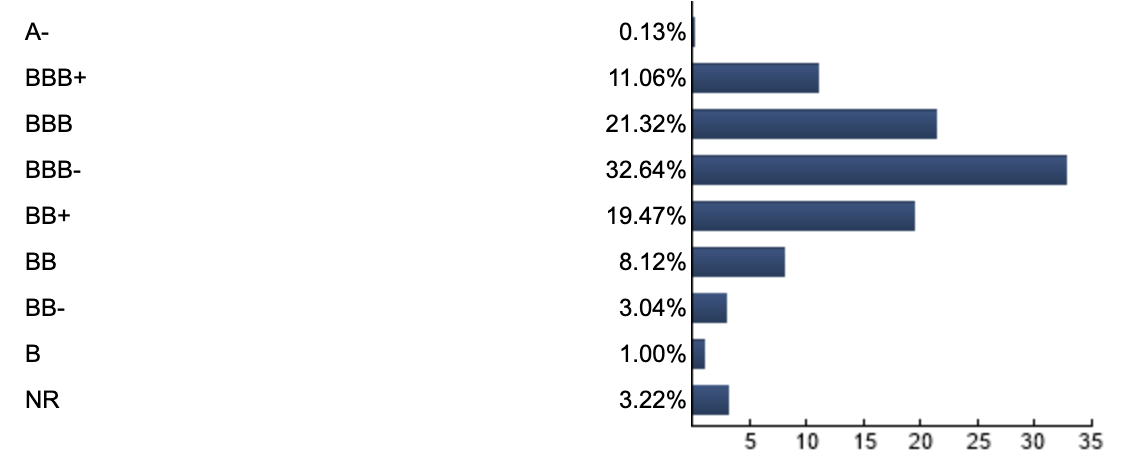

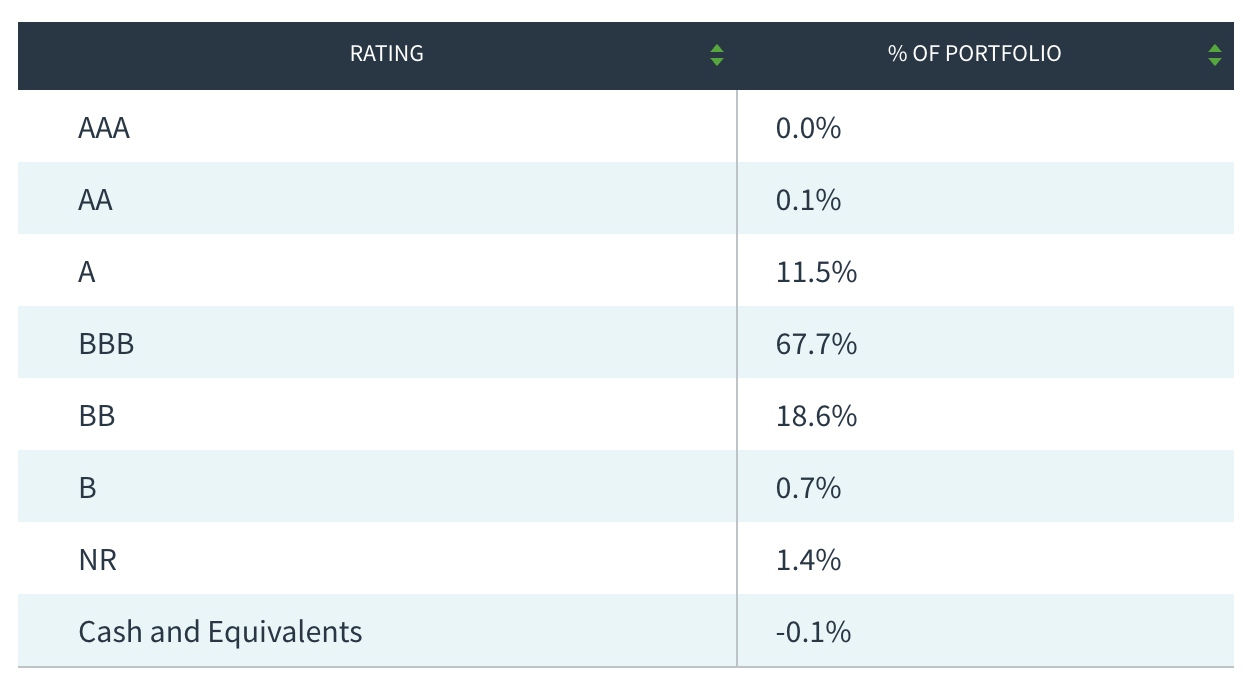

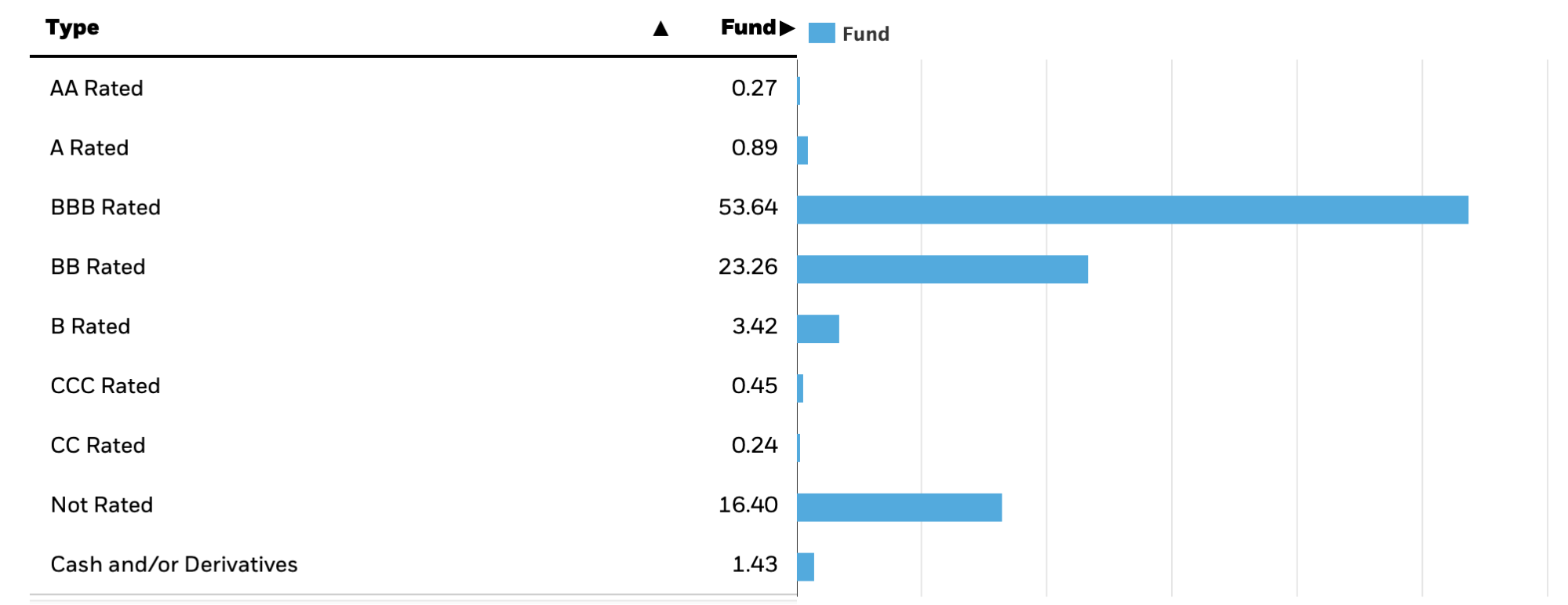

Almost 80% of this 345-stock Nuveen portfolio are investment grade, including a whopping 11%-plus exposure to A-rated preferreds. Even its “junk” debt isn’t very junky, with the lion’s share of the remainder in BB-rated issues.

Past that, JPC has thrown the kitchen sink at financials, which make up more than 80% of assets. It also has a significant international bent, with non-U.S. preferreds at 43% of the portfolio—hence, top holdings not only include the likes of JPMorgan Chase (JPM) and Wells Fargo (WFC), but also Société Générale (SCGLY) and Lloyds Banking Group (LYG).

JPC has a great deal of international exposure, with ex-U.S. preferreds making up nearly 40% of the fund. Indeed, JPC is a very global CEF, with positions including the likes of HSBC (HSBC), Lloyds Banking Group (LYG) and Barclays (BCS). And like the other preferred CEFs on this list, it uses a high amount of debt leverage (37%).

This Nuveen CEF is emblematic of what you we can expect with preferred CEFs that use a lot of leverage—similar direction as vanilla ETFs, but much more volatility. The good news? This has largely worked in JPC’s favor, and it should be able to do more with a positive environment for preferreds.

JPC: In the Midst of One of Its Violent Upswings?

Despite its recent rally, JPC’s portfolio still trades at 90 cents on the dollar, which is twice as nice as its long-term average discount of 5%.

VANILLA ETF: iShares Preferred & Income Securities ETF (PFF)

Yield: 6.5%

Had Keith Jackson been a financial pundit, he surely would have called the iShares Preferred & Income Securities ETF (PFF) “the granddaddy of them all.” It’s the largest preferred ETF, and by a wide margin—its $14.2 billion-plus in assets is nearly triple FPE’s haul.

It helps that PFF is old. This fund came out in 2007, so it has had nearly 17 years to vacuum up investor funds. A competitive expense ratio of 0.46% helps.

There’s nothing remarkable about PFF. It invests in nearly 450 U.S. preferreds, three-quarters of which are from financial-sector firms such as Wells and Citigroup (C). It is worth noting that PFF has lower credit quality than most of the funds I’ve talked about here; only a little more than half its preferred stocks are investment-grade. And that translates into a higher yield than its ETF peers.

Source: iShares

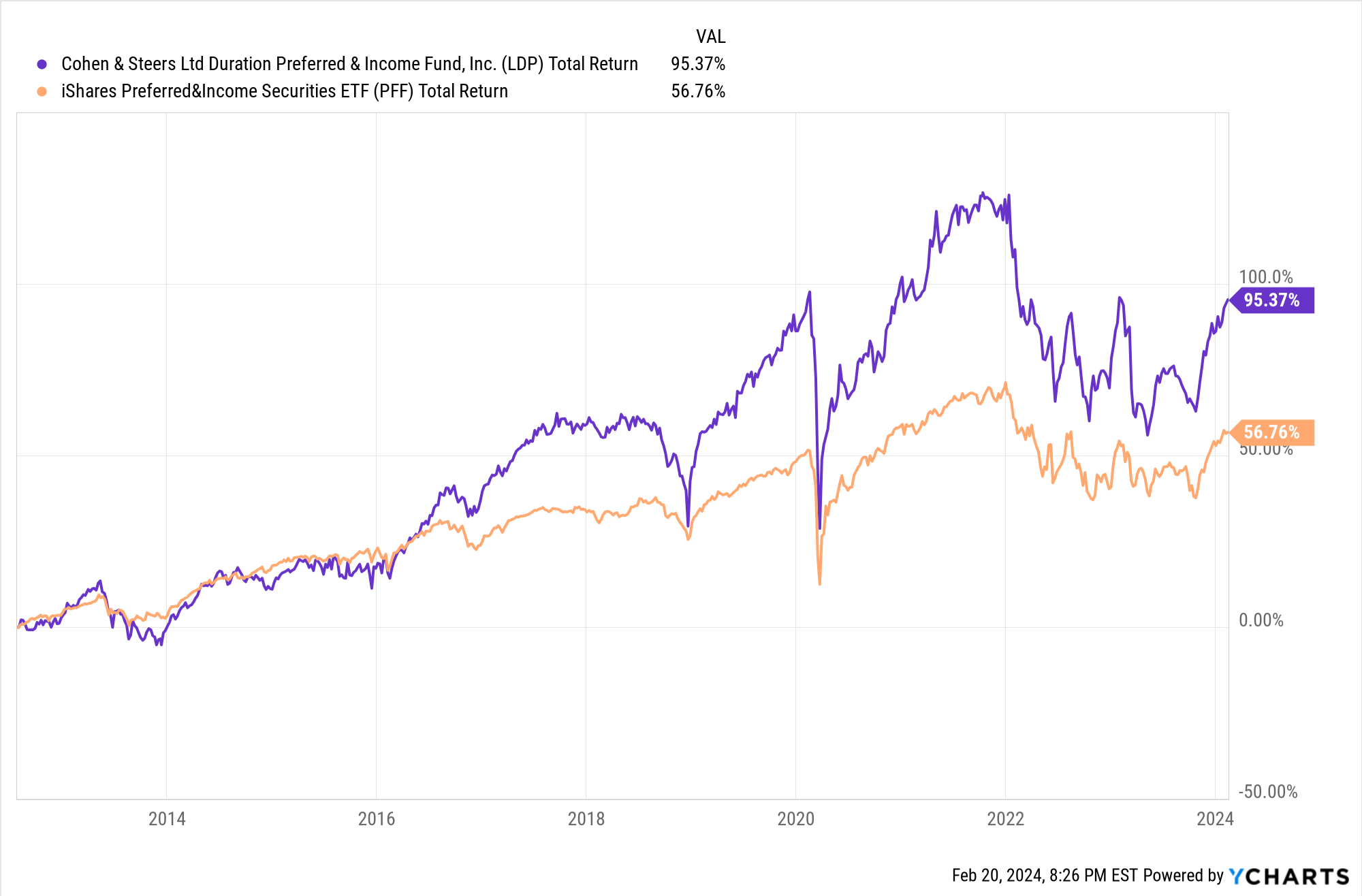

CONTRARIAN PLAY: Cohen & Steers Limited Duration Preferred and Income Fund (LDP)

Yield: 8.1%

The Cohen & Steers Limited Duration Preferred and Income Fund (LDP) doesn’t have as much of a yield advantage as these other ETF-CEF matchups, but given historical performance, I don’t think shareholders are complaining.

LDP Offers a Bumpier Ride, But It Delivers the Goods, Too

LDP is, for lack of a better word, weird.

Most preferred stocks are perpetual in nature. In other words, most of them don’t have a duration to speak of because they don’t have an expiration date. But LDP specifically targets preferreds that do—and it focuses on the particularly ephemeral ones. Namely,

LDP is a bit of an oddball in that, like the name says, it’s a “limited-duration” fund. Most preferreds are perpetual in nature, meaning they have no real duration—but limited-duration funds buy preferreds that do have expiration dates, which in theory should help us reduce interest-rate risk. Morningstar shows that the category average modified duration is around 8 years; LDP’s is currently around 3.5.

We get credit quality that’s similar to PFF, but a shorter duration, higher income (thanks to high leverage of 34%), and better historical performance. We also get a decent deal—its current 7% discount to NAV is roughly twice its five-year average.

The Bond Bull: 3 Funds Yielding Up to 12% With Massive Upside Potential

The bond market has been pulverized in recent years, with many bonds getting slashed by 50% or more—on par with the Dot-Com Bubble bust and Great Financial Crisis!

But fixed income has recently shown flickers of life—a quick reversal that could signal the start of a new “bond bull.”

And I’m getting ready by positioning myself into three funds that not only deliver fat yields of up to 12%, but have massive upside potential, too.

Bonds are throwing off their highest yields in more than a decade! The “Agg” index, with a yield of around 5%, is paying nearly 5x what it did just three years ago.

The Fed has signaled multiple rate cuts—and as you know, when rates head lower, bond prices head higher.

So right now, we have a rare chance to lock in uber-high rates before they disappear, and set ourselves up for price upside when bonds pick up steam. It’s a powerful 1-2 punch most investors don’t think about when it comes to the bond market!

I’m not the only one who has noticed, either. Capital Group, Pimco, BlackRock … all of Wall Street’s big names, collectively managing trillions of dollars, are starting to notice the potential for a sea change in the coming months.

If things go the way the Fed, the biggest investment firms and I think—well, astute investors can make a boatload of money in the bond market.