Hedge funds have a big problem: They can’t beat the market anymore.

If you read the press, you’ll see a lot of concern over this. If hedge funds aren’t cutting staff, they’re struggling to find talent to try to boost their returns. Moreover, the industry mostly keeps shuffling people within its ranks, undercutting the stability needed to make outperformance last.

So it’s kind of strange that hedge funds are managing more money than ever. The industry was managing $1 trillion in the mid-2000s, a milestone at the time. But now hedge funds are managing more than $4 trillion globally. And they’re still growing.

Therein lies the issue: Hedge funds are struggling because they’ve gotten too big. Bloomberg recently published an article titled “Hedge Funds Are Just Too Big to Beat the Market.” This quote sums up the problem nicely: “The industry is now a multitrillion-dollar business, and that kind of size inevitably leads to disappointing results.”

Hedge funds, it seems, are victims of their own success. Many of the people I’ve spoken to in the industry have said the same: Beating the market is harder because they’re managing too much money, which means smaller opportunities get ignored.

Fortunately, there’s another, lesser-known group of funds that doesn’t have this problem: closed-end funds (CEFs).

CEFs are typically small, with the largest having around $4 billion in assets and the smaller ones managing less than $100 million (the majority are around the $500-million mark). Their small size means they can often outperform bigger hedge funds, since small moves in the market matter much more for them.

For example, consider the Columbia Seligman Premium Technology Growth Fund (STK), which has around $500 million in assets. The fund mostly holds large cap tech stocks like Broadcom (AVGO), Microsoft (MSFT), NVIDIA (NVDA) and Apple (AAPL)—all of which are top holdings.

It also sells call options on the NASDAQ 100 (or its benchmark ETF) to generate extra income and reduce volatility, which is a very hedge fund–like strategy. (That’s no surprise, as STK’s parent company, Columbia Threadneedle, employs a number of professionals with hedge-fund experience.)

That’s a savvy approach because the fees STK collects from option buyers give it extra income. It then uses these funds to help support its 5.5% income stream—not an easy yield to find in tech—which the fund pays out quarterly.

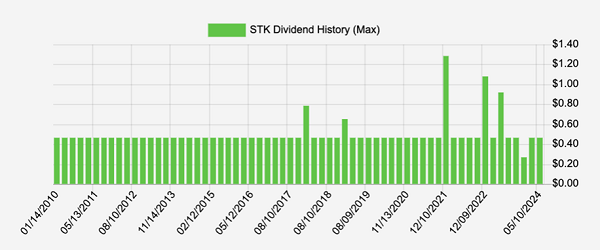

STK also occasionally pays special dividends, and since these aren’t picked up by most fund screeners, its real yield is typically higher:

Special Divs Mean STK’s “Real” Yield Tops 5.5%

Source: Income Calendar

(That dip you see on the right-hand side of the chart, by the way, is a special dividend paid out in December—not a cut.)

The strategy also reduces volatility, as STK gets more of its return in cash. And as we’ll see when we talk about our next CEF, that 5.5% yield on its regular dividend is actually low for CEFs.

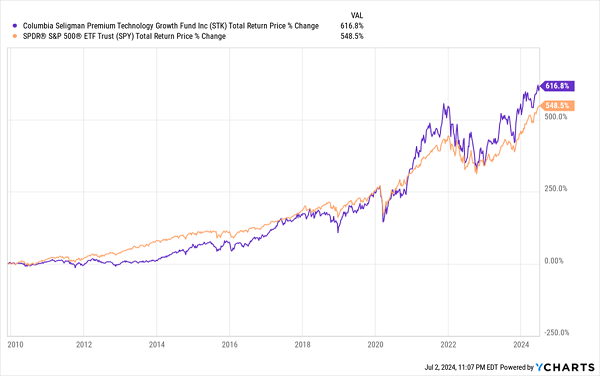

Management’s lower-volatility, higher-dividend approach has been enough to propel STK past the S&P 500 since the fund’s inception in November 2009:

STK’s Conservative Tech Strategy Beats the Market

STK’s use of complex investment strategies and deep-market analysis (tools used throughout the hedge-fund world) have helped it generate that return. And consider, too, that much of that return has come in just the last decade:

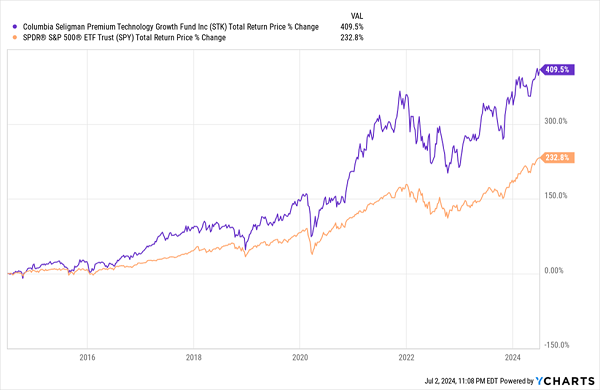

STK (Conservatively) Rides the Tech Wave Past the S&P 500

In the last decade the stock market got you an annualized 12.8% return, while STK returned an annualized 17.8%.

STK isn’t the only fund that does this—there are lots of CEFs out there that use hedge fund–like strategies to identify underpriced market opportunities, then, thanks in part to their small size, leverages them for strong gains.

This is even more impressive when we consider that CEFs don’t have “lock-ups.” What’s a lock-up? Most hedge funds have rules for investors: If you invest in the fund, your money is “locked up” and can’t be withdrawn for a certain period. These are typically a year in length, but they can be longer.

CEFs, meanwhile, are publicly traded: You can buy and sell them with any broker, including online brokers, during regular trading hours, just like any stock.

But let’s swing back to dividends for a second: These funds regularly distribute the profits they earn in the form of regular payouts; as mentioned, STK pays those quarterly, while many other CEFs pay monthly.

And while STK yields just 5.5%, as mentioned, other top-quality CEFs yield more, like the BlackRock Science and Technology Term Trust (BSTZ), an STK rival that recently increased its dividend to an all-time high of $0.213 a share monthly (not including a big special dividend paid in late 2021).

This payout hike means that BSTZ now yields an outsized 12.5%. That’s much higher than the 8.3% average yield that CEFs currently offer. But it goes to show how much income CEFs can provide, while also giving investors exposure to top fund managers.

Why aren’t more people buying CEFs? A lack of awareness is the real issue now, but that’s changing. More people are learning what these high-yielding funds can do, and they are getting into the CEF market. That means anyone who is early to the game is going to profit more than the latecomers; it just depends on when you decide to buy in.

5 MORE CEFs That Crush Hedge Funds (and Yield 8.5%)

My top 4 CEFs to buy now yield an outsized 8.5% and are cheap now—so much so that I’m calling for 20%+ price gains from them in the next 12 months. That’s in addition to their 8.5% payouts.

And they’re all smaller CEFs, which gives them an added edge over the huge, lumbering hedge funds that hog the media spotlight.

Click here and I’ll share more details on each of them with you and explain more about why CEFs are (for now) so far off the radar. You’ll also get to download a FREE Special Report naming all 5 of these funds, including their tickers, current yields, discounts and everything else you need to get in on them now, while they’re still cheap.