Small companies are sneaky AI-friendly plays because they are implementing these tools faster than their larger competitors.

Expect to see these smaller firms become more efficient in the quarters ahead. Sales will continue to increase while headcounts will remain relatively flat as robots take up the slack—a boon to future profits.

Ironically, small caps are currently the cheapest sector on the board:

Broad-Market Forward P/Es:

- S&P 500: 22.2

- S&P MidCap 400: 16.2

- S&P SmallCap 600: 15.6

So, we turn our attention to a six pack of small but mighty dividend payers. Let’s start with a lender that yields “only” 15.7% per year and work our way up from there.

We discussed BlackRock TCP Capital (TCPC, 15.7% yield) recently as part of our “unloved stocks” focus. This business development company (BDC) invests in more than 150 companies across 20 industries, with a penchant for first-lien debt. It really began underperforming with gusto in 2023; it’s currently restructuring deals amid portfolio credit issues, so things don’t look much better now.

But TCPC’s woes have opened up a wide 18% discount to its net asset value (NAV)—that and a 14% regular yield (with an additional 1.7% from specials) might tempt some distressed-asset buyers.

That said, the vast majority of BDCs trade for less than their NAV right now, and most of them sit in the small-cap space, so perhaps there’s more fertile ground elsewhere.

For instance, New Mountain Finance (NMFC, 12.1% yield) offers a double-digit yield and a double-digit discount to NAV (14%).

NMFC deals in U.S. upper-middle-market businesses backed by private equity sponsors. First-lien debt is its most common deal type, at 65% of the portfolio currently, but it has positions in second lien and subordinated debt, preferred stock, common stock and net lease deals.

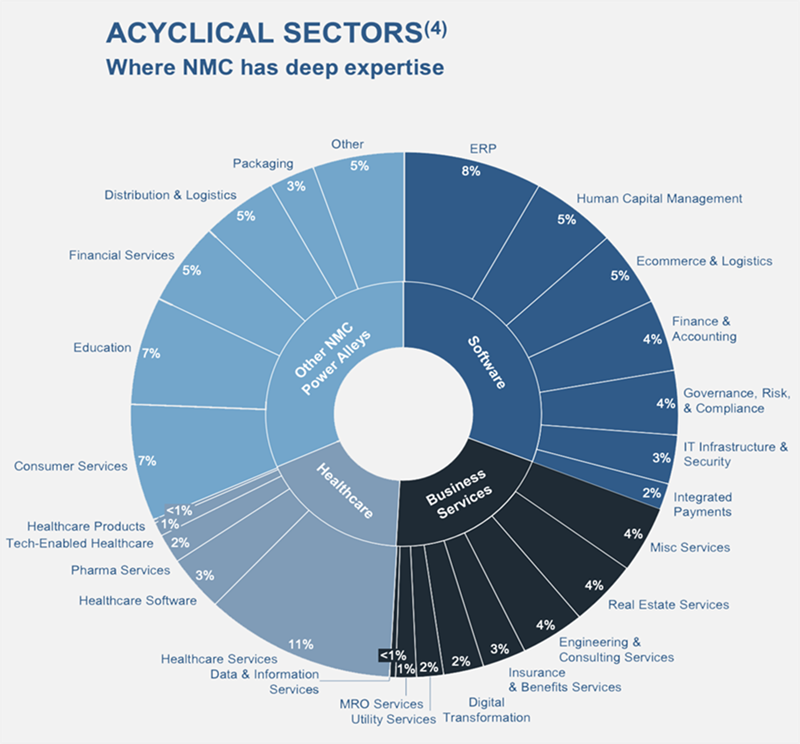

Its portfolio is 124 companies wide right now, and it uses a “defensive growth” strategy, with a focus on investing in strong businesses in acyclical sectors.

NMFC Spreads Out the Risk Across a Few Business Clusters

Source: New Mountain Finance Q2 2025 Earnings Presentation

New Mountain bounced off the COVID bear-market bottom much like other BDCs. But when the industry caught a second wind in 2024, NMFC was largely left behind. Shares are down about 3% even after accounting for its massive yield, which helps to explain its wide discount to NAV.

The problem is that NAV is declining too, including a big quarter-over-quarter dip of nearly 2% between the first and second quarters. NMFC suffered from markdowns on healthcare, consumer products, and ed-tech firm Edmentum.

On the bright side, non-accruals (loans that are delinquent for a prolonged period, usually 90 days) were stable, and its credit quality remains in decent shape. Moreover, the company has fee waivers and a dividend protection program to keep the high payout in place. But for that discount to NAV to be a bona fide deal, we’ll need to see better business performance.

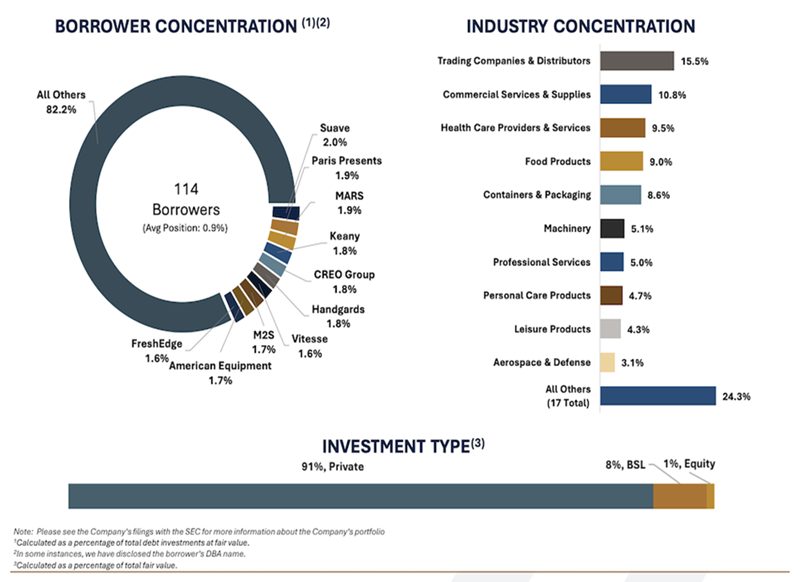

Kayne Anderson BDC (KBDC, 12.6% yield) is another BDC operating in the middle-market with a penchant for private equity-backed, first-lien loans. KBDC targets companies with between $10 million and $75 million in EBITDA (earnings before interest, taxes, depreciation and amortization), and its 114 portfolio companies are largely concentrated in defensive, stable industries.

As BDC Portfolios Go, Kayne Anderson’s Is Heavy on Safety

Source: Kayne Anderson BDC Q2 2025 Earnings Presentation

This is an extremely fresh-faced BDC: It began operations in 2021 and went public in 2024. And while it has hardly come roaring out of the gate—its lifetime total return is 1 percentage point removed from the VanEck BDC Income ETF (BIZD)—there are signs of a decent business here.

Are there weaknesses? Yes. One small loan was added to the non-accrual list during Q2, bringing non-accruals to 2.2% of the total portfolio on a cost basis (up from 1.9% in Q1). And NAV declined by just less than 1%.

But the company’s investments have been picking up in Q3, including a strategic $80 million investment into lower-middle-market credit manager SG Credit at an 11% cash fixed yield. It’s running a $100 million buyback program through May 2026. And part of the aforementioned NAV decline was a 10-cent special dividend—its third in as many quarters. (KBDC yields 10% based on its 40-cent-per-share regular quarterly dividend; specials bring that up to 12.6%.)

Mach Natural Resources LP (MNR, 16.0% distribution) is in another big-income niche: master limited partnerships (MLPs). While they can be a pain come tax time because of their additional K-1 form, double-digit distributions can make them worth our time.

MNR is a young MLP that formed in November 2017 and went public in late 2023. Its primary operations are in the Anadarko Basin, and it has additional assets in the Green River basin. More recently, it has expanded its reach to the San Juan and Permian basins. While many of its peers are oil-heavy, it has a higher natural-gas mix that in the most recent quarter represented just over half its production. It’s also an efficient operator and has a good track record of buying assets at low valuations.

MLP valuations get far into the weeds, but a common-enough one is EV (enterprise value)/EBITDAX (earnings before interest, taxes, depreciation, amortization and exploration expense). On that front, MNR trades at roughly 3.5 times this year’s EBITDAX estimates, which is a little more than half of the average among comparable MLPs.

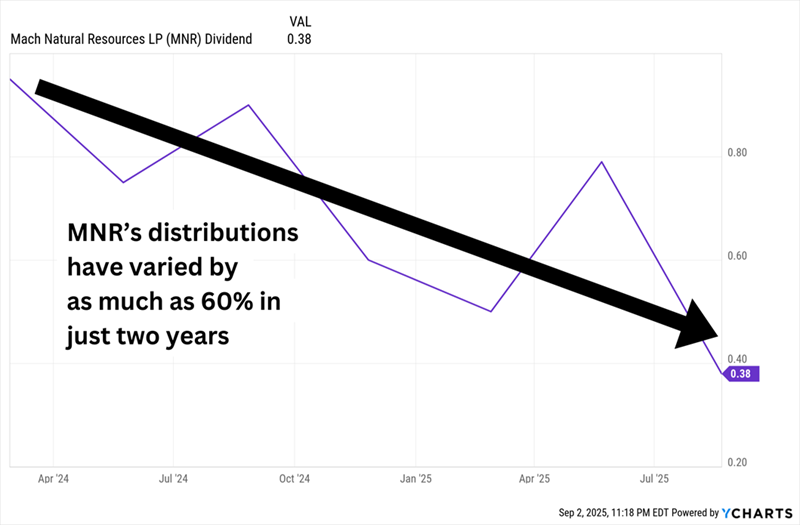

Just understand that while the distribution is sky-high, it’s also all over the place. That’s because MNR pays out variable distributions, which are based on cash available after its 50% reinvestment rate.

Don’t Mind the Distribution’s Short-Term Direction So Much as the Volatility

MFA Financial (MFA, 14.4% yield) invests in residential mortgage loans, residential mortgage-backed securities (MBSs), and other real estate assets. It also originates and services business purpose loans (BPLs) through its Lima One Capital subsidiary.

MFA has massively outperformed the mREIT industry throughout its publicly traded life, though shareholders are best advised to wear their seatbelts—it speed-runs peaks and valleys alike.

MFA Financial Has Rewarded Investors Who Could Stomach It

Lima One, which MFA acquired in 2021, is heading in the right direction; Q2 origination, servicing and other fees were up 13% QoQ, and the subsidiary added 15 loan officers during the quarter. Delinquency trends aren’t nearly so clean-cut: In Q2, they declined on the residential whole loan portfolio and single-family rental loans, but increased in the single-family BPL portfolio.

Distributable earnings (DE, a non-GAAP measure of profitability that MFA favors) are expected to drop significantly this year before rebounding in 2026. Until then, the dividend is expected to outpace DE—that’s hardly a comfortable position. On the flip side? The market doesn’t appear to be pricing in a cut, and in fact, MFA actually raised its dividend by about 3% earlier this year—its first hike since a 20% cut in 2022.

But MFA is value-priced, at about 7 times 2026 earnings estimates and 73% of book.

We can get a downright jaw-dropping dividend from Armour Residential REIT (ARR, 19.0% yield), which primarily invests in fixed-rate “agency” residential MBSs, which are those issued or guaranteed by government-sponsored entities such as Fannie Mae, Freddie Mac, or Ginnie Mae.

The value picture is a bit different from MFA, but it’s still cheap—ARR trades at about 90% of book, but also at just more than 4 times 2026 core EPS estimates.

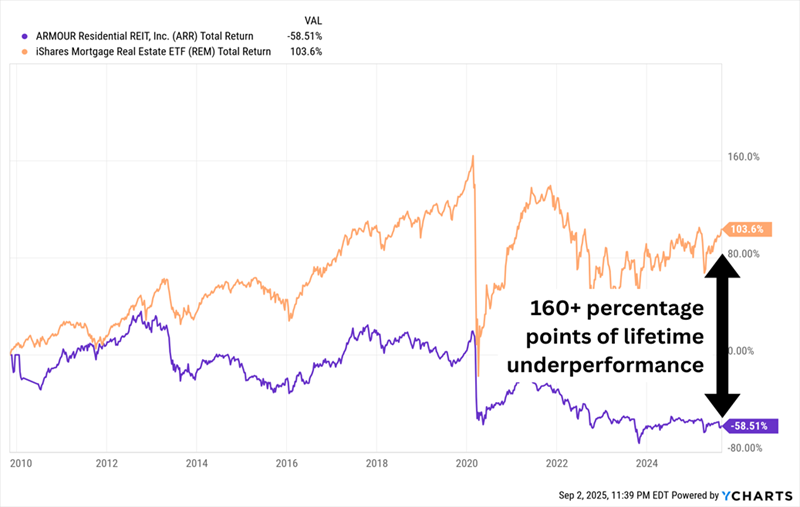

The question is: How deep must the discount be to ignore Armour’s past?

Consider this: In December 2024, I wrote that “any prospective investors will have to overcome a significant mental hurdle: namely, Armour’s horrific dividend track record.” Armour has cut its payout seven times since 2015, and that reflects serious underperformance compared to the mREIT industry.

Not Pictured Here: 2 Reverse Stock Splits and More Than a Dozen Dividend Cuts!

It has continued to underperform since then, but it really detached from the mREIT group in August following a second-quarter miss on distributable EPS and net interest income. Book value per share dropped by 9%.

If there’s any solace, it’s that the nearly 20% dividend remains well-covered. But even with that mammoth dividend, ARR has been historically incapable of delivering consistent positive total returns.

You Saved and Saved—And Think You Still Can’t Retire? Think Again.

Most of these BDCs and mREITs have the home-run dividend yields we need to retire on dividends alone. But they don’t necessarily have the other vital part of the retirement equation: a predictable income stream.

That’s OK. Because you can find both in my Contrarian Income Report research service.

Stack up a few of our favorite high-yield, low-drama payers, and you’ll be on the path to a retirement funded by dividends alone—on a far smaller nest egg than you think you need.

Heck, you might have enough saved up to clock out right now.

Don’t let your retirement strategy be governed by inflation fears, recession fears, geopolitical fears, and plain old fear fears. Instead, invest in the kinds of stocks and funds that march to the beat of their own drum—and pay us well for marching right alongside them.