Today I’m going to show you a two-part dividend-growth strategy that actually made money for one group of investors in the disastrous year that was 2008. It’s an appropriate investing strategy for us to follow now, with the Federal Reserve likely to raise rates until we end up in a recession (assuming, of course, that we’re not in one already!)

Before we get into the specifics on this technique and an example stock, I want to level with you. I do believe that stocks are heading lower still before they ultimately head higher.

That said, if we look one year out from today, I like our chances. And if you’ve been following my work—and cautionary warnings!—through 2022, you know that I don’t say this lightly. And I would not have said this in January.

Fortunately it is now July, and we can responsibly begin to nibble on the highest-quality dividend growers. In doing so, we are going to demand these two traits:

- Strong—and better yet accelerating—dividend growth, because as we’ve been saying over and over (and over!) in our recent series on my Dividend Magnet investing strategy, it’s the No. 1 driver of share prices. And …

- A low beta: Beta is a volatility measure, and you can spot it on most screeners. Simply put, a stock with a beta of 1 trades more or less alongside the market. Betas below 1 are less volatile than the market, while those above are more volatile.

Combine a low beta and an accelerating dividend and the result can be a truly powerful—and stable—income-and-growth machine, with the rising payout pulling up the price while the low beta rating throws a floor under the shares when storms like this one hit.

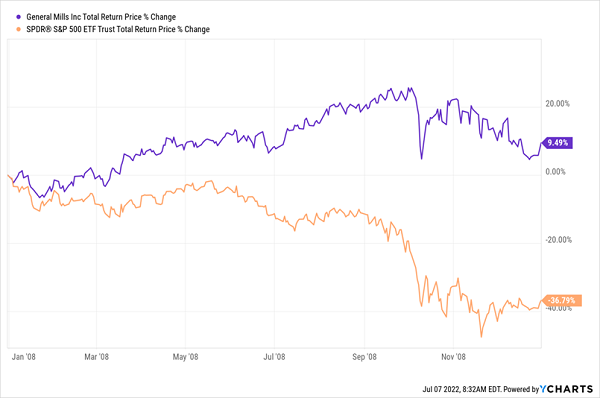

The classic example of a low-beta dividend grower defying a crash came the last time a financial crisis (as opposed to a health crisis) walloped the market. That was 2008, a year that, as most of us painfully remember, wiped 37% off the S&P 500. But General Mills (GIS), which has a history of being a lot less volatile than the market, sailed through.

During 2008, its five-year beta averaged just 0.23, meaning it was only 23% as volatile as the S&P 500. The reality turned out even better for GIS shareholders: the stock was one of a tiny handful to come through that disastrous year with a gain—and a decent one at that:

General Mills: The Classic Low-Beta Survival Story

Heck, even when General Mills’ stock bottomed that year, in December, it was still up nearly 2% from its January 2008 level. The only problem with General Mills today is that its dividend growth is not only meager but decelerating.

General Mills’ Underfed Dividend

Sure, the payout is up 151% since the end of ’08. That’s okay—and its Dividend Magnet has pulled up the share price in lockstep. But as you can see on the right side of the chart, the dividend has barely budged in six years—and the share price has gone nowhere, too. That seems unlikely to change as inflation drives up the company’s ingredient costs.

To be sure, GIS remains a decent stock to hold—thanks to its low beta, it’s unlikely to fall as far as the market on the next leg down. But there are far better examples of a Dividend Magnet and a low beta rating combining for superior returns.

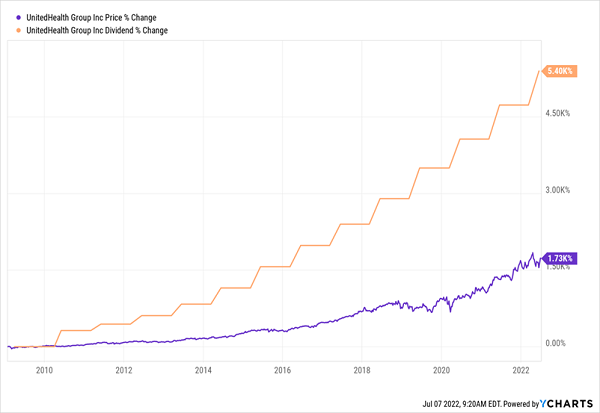

UNH’s Shocking 5,400% Dividend-Growth Story

Case in point: health insurer UnitedHealth Group (UNH), a name Hidden Yields members will know well: we’ve bagged a 76% total return on the stock since we bought it in January 2020.

Check out the difference in dividend growth since ’08, compared to General Mills: it’s not even close! UNH’s explosive payout growth has driven a price gain more than 10X bigger:

UNH Shows What a Real Dividend Magnet Can Do

Also note the stock’s accelerating payout growth in recent years (UNH just announced a healthy 14% dividend hike in June).

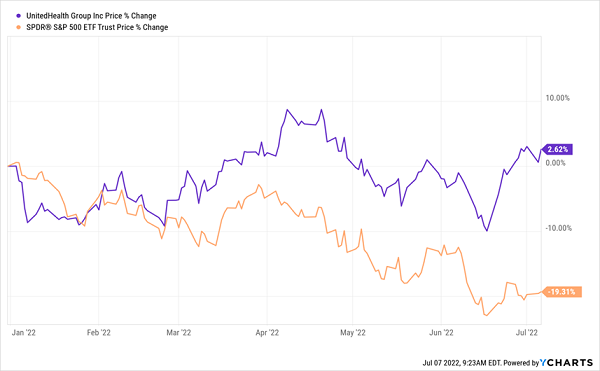

Thanks to its five-year beta of just 0.77, this one should be 23% less volatile than the S&P 500. But this year, like GIS in ’08, it’s done a lot better: as the market sunk 19%, UNH gained ground:

“Low Beta” UNH Defies Gravity

This is also the best way to build a safe, high dividend over time. Because if you hold a stock like UNH over the long haul, your yield on cost—or the stock’s current yield at the time of your original buy—will likely soar, thanks to its strong dividend growth.

Consider this: if you’d bought UNH in early ’09, your dividend would have barely registered, due to the stock’s near-invisible 0.1% yield at the time. But fast-forward to today and you’d be yielding an incredible 24.8% on your original buy, thanks to the stock’s stunning 5,400% dividend growth in that span.

UNH’s strong growth came in large part because it had the foresight in 2011 to start Optum, its own technology-driven unit. Optum provides pharmacy benefits, runs clinics and supplies data analytics and other cutting-edge tech to streamline healthcare. These days, Optum’s earnings continue to grow faster than UNH’s legacy business, and its profits account for more than half of the firm’s total bottom line.

Imagine getting a quarter of your original buy back in cash dividends every year! That’s the power of the Dividend Magnet.

New Report Reveals 7 MORE Low-Beta “Dividend Accelerators”

I’ve uncovered 7 MORE stocks with this proven combo of dividend growth and low beta that are perfect for the market we’re facing today. If you’re buying now, these 7 names should absolutely be at the top of your list.

I’ve prepared a Special Investor Report that gives you my research on these 7 stocks, including their names, tickers and my in-depth analysis of their operations. Click here and I’ll tell you more about my “pullback-resistant” dividend-growth strategy and show you how to get your copy of this exclusive report today.