Worried about a serious pullback in the S&P 500?

That something is going to go a bit haywire here in America, or overseas, and send stocks swooning?

If so, this 5-stock portfolio is for you. It yields up to 7.3% and it is built to withstand Armageddon.

No, really. These “low beta” payers can really lower our blood pressure. (Hold my beetroot juice!)

We blunt the bears with big dividends and small betas. Beta is a measure of an investment’s volatility against a benchmark.

If a stock has a beta of 1, it means it’s every bit as volatile as “the market.” But if a stock has a beta of 0.5, it means it’s only half as volatile as the S&P 500. Which means if the market dropped 10%, we’d only be out 5%.

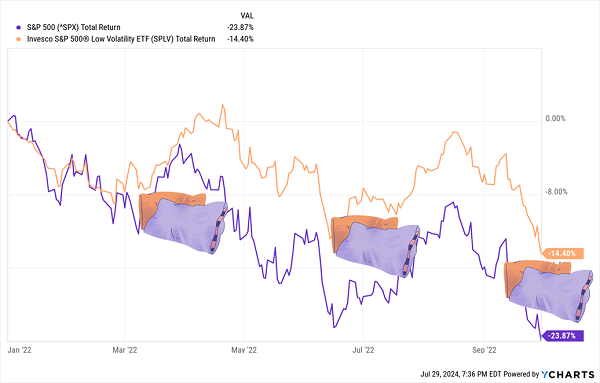

The effect is most pronounced (and most appreciated) in bear markets. Just look at how low beta did compared to the index as stocks spiraled in 2022:

Low-Beta Stocks Provide Downside Cushion

Just remember: The other side of low volatility’s double-edged sword is that the potential for upside can sometimes be capped, too. That’s why we need to identify the best of the best—companies that can reduce downside drama, pay out a substantial income, and can keep up when the bulls start charging again.

Let’s see what we can find amid these five low-beta dividend stocks delivering 3x and 5x the market’s yield right now.

Amcor (AMCR, 4.8%) isn’t at all what we’d think of when we think about low-beta stocks. It’s in the highly cyclical materials sector, which is joined at the hip with the ebb and flow of the economy.

But Amcor is a special case. It makes a variety of packaging—including shrink bags for food, blister packaging for pharmaceutical pills, and sachets for cosmetic samples—for consumer and healthcare companies.

So consumer demand still matters here, but perhaps not as acutely as consumer cyclical companies that specialize in just one or a few product categories.

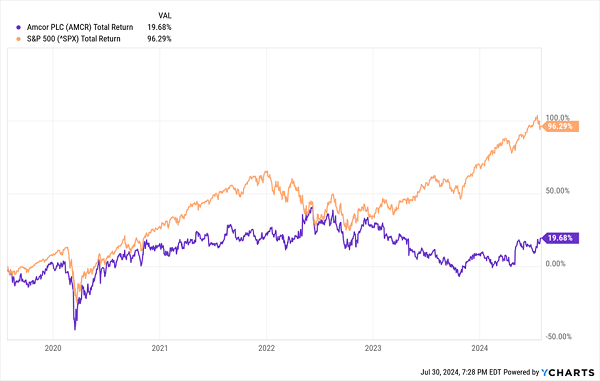

After more than a year’s worth of weakness thanks to lackluster consumer demand, AMCR shares are finally picking up, buoyed by both aggressive cost cuts that are starting to bear fruit, as well as improvement in volumes.

Amcor Is Trying to Claw Back Its 2022-23 Losses

Amcor has a few defensive characteristics. It’s a Dividend Aristocrat with more than four decades of uninterrupted payout growth and a yield near 5%. And its five-year (0.87) and one-year (0.43) betas are plenty low.

But I would stop just shy of calling AMCR a defensive stock. It’s not a reliable source of protection in down markets—instead, think of Amcor as marching to the beat of its own drum.

Northwest Bancshares (NWBI, 5.7% yield) enjoys its own unique rhythm, too, but in this case, you have a cyclical stock that truly feels more defensive in nature.

NWBI is the holding company behind regional financial Northwest Bank, which operates 131 full-service community centers in Ohio, Pennsylvania, Indiana and New York. Yes, it’s in another cyclical sector—financials—but it has a more even keel. It’s very well capitalized, and it has a much lower-risk loan profile compared to its regional peers.

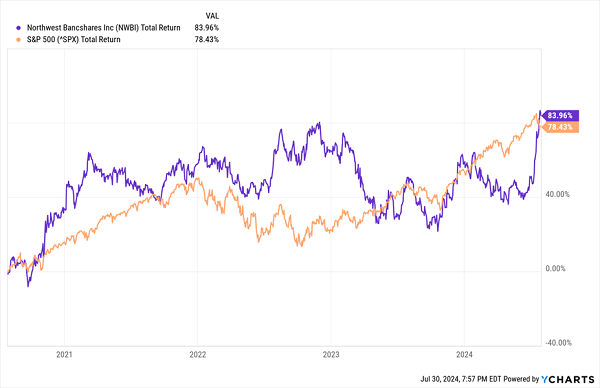

Here, we’re getting much more of what we bargain for with low-vol stocks: an ability to fade downturns while also capturing some upside during bull runs.

But It Really Seems to Move, Doesn’t It?

Yes, NWBI is capable of moving in big bursts. But remember: Beta is a comparison to the market over time. In both the short term (one-year beta of 0.38) and medium term (five-year beta of 0.62), NWBI isn’t moving nearly so much.

Perhaps my only complaint about NWBI is its dividend. It offers up a nice yield approaching 6%, but the payout hasn’t budged since 2021.

Getty Realty (GTY, 6.0%) frequently pops up on my research radar. And while its growth potential is just slightly less than what I’d want to see, it is the very definition of “boring is beautiful.”

Getty Realty is a real estate investment trust (REIT) that owns more than 1,100 single-tenant retail properties in 42 states and the District of Columbia. That brick-and-mortar retail specialization would normally be a red flag. But Getty’s tenant mix (by annualized base rent) is nearly two-thirds convenience stores, 20% express tunnel car washes, and the rest is a mix of legacy gas stations, repair hubs, auto service centers, and a dash of drive-through quick-service restaurants.

At the end of the day, Getty is a REIT, which means it’s at the behest of interest rates. And I’ve previously mentioned that an EV-centric world is a potential threat to some of its gas-station properties.

Still, Getty is a rock. It did cut its dividend back in 2012—fallout from Getty Petroleum Marketing, then its largest tenant, filing for bankruptcy. But GTY repossessed 788 properties in the wake, and it has grown its dividend annually without interruption ever since. In the past decade, GTY shares have underperformed the market, sure, but they’ve delivered a solid (and growing) income stream. The five-year beta of 0.92 implies that Getty hasn’t been exceedingly less volatile than the market, but it has been relatively calmer over the past year, with a one-year beta of just 0.40.

I want to like Universal Corp. (UVV, 6.1%). It’s a high-yielder. It’s in one of the stickiest consumer-staples industries (tobacco). And it has a pick-and-shovel kicker.

When you think of tobacco stocks, you think of companies like Philip Morris (PM) and Altria (MO) that produce cigarettes and other tobacco products. However Universal Corp. is brand-agnostic—because it doesn’t produce finished products, but instead merely supplies the tobacco.

Universal has diversified over the years, too, with an ingredients division (Universal Ingredients) and a “value-added agricultural business” (Universal Enterprises) that includes liquid nicotine production, a lifecycle data solution and even a 12,800-square-foot compost facility in North Carolina.

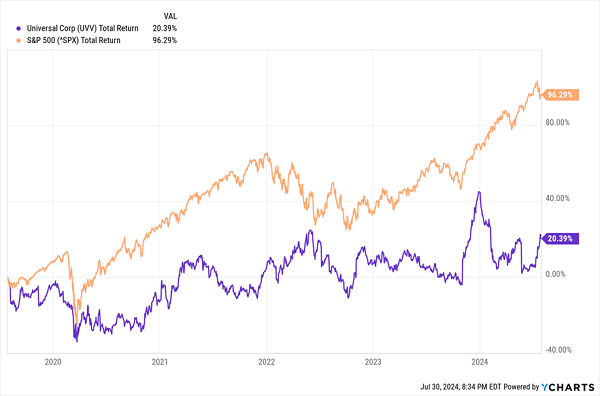

We’d expect low volatility out of a company like this, and we get it. UVV’s five-year beta is 0.79; over the past year, it’s been less than half as volatile as the market, with a beta of 0.47.

Unfortunately, there are just no signs of meaningful growth. The dividend has been climbing at a low-single-digit rate for seemingly ages now, and compared to the broader market, shares are practically in park.

Is Safety Worth This Much Underperformance?

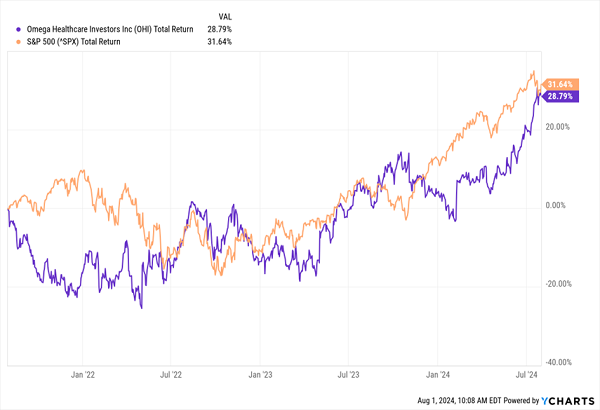

The highest yields on this list belong to a REIT that focuses on elderly Americans.

Omega Healthcare Investors (OHI, 7.3% yield) is a triple-net REIT that provides financing and capital solutions to skilled nursing facility and assisted living facility partners. It has a five-year beta of 0.96 that implies only slightly less wiggle than the market, but a much calmer one-year beta of 0.58.

Stocks like OHI were among the COVID bear market’s most high-profile implosions. At one point, roughly a third of COVID-related fatalities were coming from senior-related properties. Would-be tenants found any alternative they could to living in senior housing. And priming the pump: Even before the pandemic, senior housing faced a significant glut of supply.

Fortunately, the worst of the pandemic is well in the rear-view mirror. But while OHI’s shares have bounced back above pre-COVID levels, it would be a stretch to say things have calmed down.

For instance, in April, the Centers for Medicare and Medicaid Service (CMS) issued its final minimum staffing ruling for skilled nursing facilities (SNFs) in the U.S.; at the time of passage, it was estimated that three-quarters of American SNFs were staffed below these new thresholds. However, senior housing has largely enjoyed increases in both occupancy and rates, while SNFs have enjoyed improving reimbursement rates.

The net effect, it would seem, is still largely positive for OHI and its peers.

But There’s a Bigger Factor at Play in This Chart

OHI is operationally on the mend, but you’ll notice that it’s only in recent months that shares have really started to take off. That’s because ultimately, this REIT (and several others!) is largely an interest-rate play. As expectations for the Federal Reserve’s first rate cut of the cycle have grown, so too has enthusiasm for rate-sensitive stocks.

Earn a Reliable 8%+ in Retirement—Paid Each and Every Month!

In fairness to OHI, very few companies will be completely unmoved by Powell & Co.

But if you’re hunting down cornerstone investments that can really stabilize our portfolios, you want to hold stocks and funds that are a little less “headline-reliant.”

And if you want to retire on dividends alone, you’ll probably need a little more yield.

My “magic number” for retiring on dividends alone is 8%.

At that level, a million-dollar portfolio will allow you to collect $6,600 in dividends each and every month. Even if you’re behind on your retirement savings, a half-million-dollar portfolio would still pay you $3,300 every month.

That’s the simple math behind my “8%+ Monthly Payer Portfolio”, which is made up of some of Wall Street’s most mouth-watering yields.

And these portfolio picks offer oh-so much more than income alone:

- They’re beautifully boring, “steady Eddie” stocks that don’t make us slap the panic button in bear markets.

- They have significant projected price upside, which means we can keep growing our nest eggs well after we’ve quit our jobs.

- They pay us monthly—not annually, not quarterly, but monthly!—which aligns our income with all of life’s expenses.

Put simply: This is how you win retirement.

No drama. No nonsense. Just substantial income, month in and month out, allowing you to think less about how you’ll manage your finances and think more about your golden years.

Can your current portfolio generate a $40,000-$80,000 annual “salary”? If not, it’s time for a change. Click here to learn everything you need about these generous monthly dividend payers right now!