There’s an unusual shift unfolding in the labor market that we contrarians can tap for outsized dividends (I’m talking a near-10% yield here), plus price upside for years to come.

We’ll do it using a closed-end fund (CEF) that’s tethered itself to a trend everyone has missed—a trend that’s concealed behind a metric called the labor force participation rate, or LFPR.

It may have a boring name, but that doesn’t stop the media from reporting on the LFPR. You’ve likely heard it pop up in the mainstream press from time to time.

It simply refers to the percentage of the population that’s actively working or looking for work. The bigger the number, in theory, the more productive a country is because it has more people to work and grow its economy.

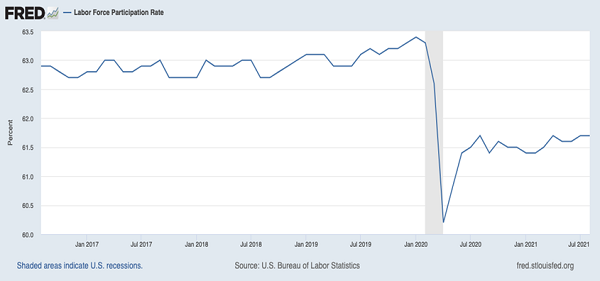

With an LFPR of just 61.7% in the US, it sounds like we’re far from our productive peak. After all, today’s rate is down from just over 63% before the pandemic and behind the LFPRs of both China (around 68%) and the European Union (72.6%).

The US: A Productivity Laggard?

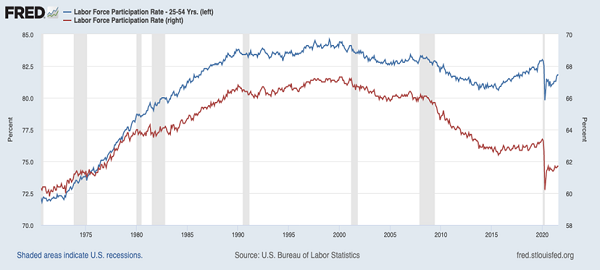

That, of course, would lead you to believe that our lower LFPR is a drag on corporate profits (and share prices). But jumping to that conclusion would be a mistake. To get at what’s really going on here, we need to look at the LFPR for people aged 25 to 54, the group that’s in their prime working years.

And their LFPR (shown in blue below) tells a much different story than the headline number.

Younger Workers Are Busy—and Getting Busier

With an 81.8% participation rate, these prime working-age Americans are very likely to be working or looking for work, and that number has recovered to its mid-2010s level after aggressively improving in recent months.

Economists expect it to go higher still, even if the broader LFPR is set to stay lower, as baby boomers retire. And that’s okay, because these highly productive people are still hard at work, and they’re pocketing fatter paychecks, too.

A CEF That Turns Rising Wages (for Workers) Into a 9.8% Dividend (for Us)

Of course, we all know that ongoing labor shortages are pushing workers to demand higher pay and better working conditions.

On the one hand, this is bad for corporate earnings—companies will have to share more of their profits with employees. On the other hand, it’s good for corporate revenue because more workers will make more money they can then spend on goods and services.

To play this trend, we want to buy companies that are valued more for their revenue than their earnings and do not rely on a lot of manual labor to produce their products.

There just happens to be a CEF that has a lot of those companies in its portfolio: the Liberty All-Star Fund (USA), payer of a 9.8% dividend today.

With a lot of tech companies that rely on computers and robots to do their work, such as PayPal (PYPL), Amazon (AMZN), Facebook (FB), and Adobe (ADBE), USA is nicely positioned to profit from our current labor market situation.

These companies, most notably Amazon, have been paying workers above-market rates for a while now and are increasing pay—and that’s okay, because investors care much more about Amazon’s revenue than its earnings.

And the management team running USA is proven, too: they’ve defied the conventional “wisdom” that actively managed funds can’t beat the S&P 500 over the past decade:

Human Managers: 1, S&P 500 Index Fund: 0

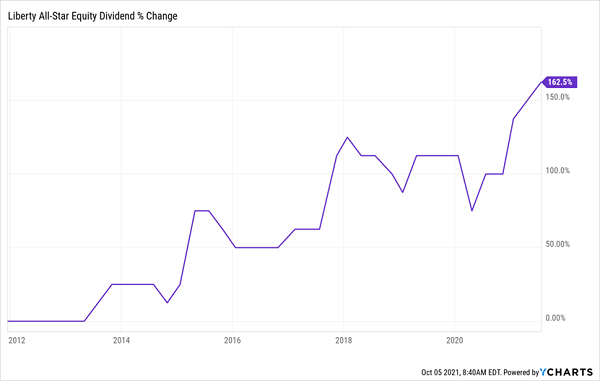

Note also that the chart above shows both funds’ total returns, including dividends—and due to USA’s high yield, most of its return was in cash, rather than ephemeral price gains. And about that 9.8% dividend: it’s not only sky-high today, but it’s nearly tripled over that period, as well.

A 9.8% Dividend That Soars

As you can see above, USA’s dividend rises in a two-step-forward, one-step-back fashion. That’s actually a benefit for investors because USA tends to reduce its dividend slightly during periods of market weakness, so management can free up cash to grab stocks at a discount. That’s a smart strategy because the bargain stocks the fund buys boost its upside and our future income stream, letting USA raise its payout when the market gets back on its feet.

The result is an overall long-term rise in the dividend, as you can see from the chart above.

The only catch here is that USA trades at a 7.5% premium to net asset value (NAV, or the value of the stocks in its portfolio) as I write this. But the fund has seen premiums in the double digits as recently as June 25, when its premium broke over 13%, and a return to double-digits is certainly on the table as the fund continues to benefit from long-term shifts in the labor market.

But bear in mind also that USA’s premium dropped as low as 2% in August, so you can afford to wait with this one (as we’re currently doing in my CEF Insider service), put it on your watch list and pick it up when the next pullback drops its valuation to par (or below).

Whenever you buy, you’ll be nicely aligned with ongoing trends in the labor market while getting a huge dividend—maybe big enough to get you out of the labor market, too!

Urgent Buy Alert: These 4 CEFs Yield 7.3% (and They’re Set for 20%+ Gains)

If you want to hold off on USA for now, I get it. But I’m not letting you walk away empty-handed! I have 4 other CEFs for you that are ridiculously discounted and ripe for buying now.

Taken together, these 4 powerhouse funds pay you a strong 7.3% payout. And thanks to their totally unusual discounts, my latest analysis calls for 20%+ price upside from each of them in the next 12 months!

Put it all together and you could easily be looking at a solid 27% in price gains and dividends by this time next year.

Don’t miss your chance to buy these 4 stout income plays now, while they’re still cheap. Click here and I’ll give you everything you need to know about all 4 of these high-yielding CEFs—names, tickers, current yields, and my complete analysis of management—in a special investor report.